(Bloomberg Opinion) -- Two likely events have just complicated the global economic outlook for Fed Chair Jerome Powell as he prepares for his speech on Friday at the Jackson Hole virtual central banking symposium.

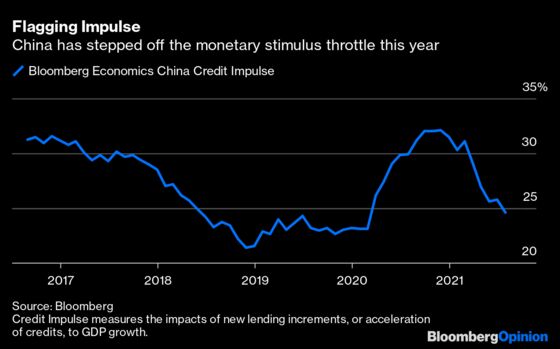

First, the U.S. House of Representatives backed President Joe Biden’s $3.5 trillion budget resolution, moving it an important step toward passage. It includes $550 billion to spend on infrastructure. Secondly, the Peoples Bank of China just signaled it is going to pump credit into the world's second largest economy.

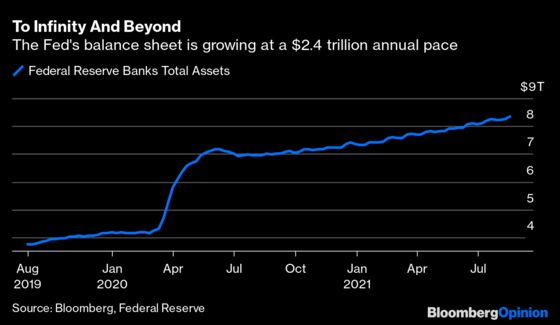

A trillion here, a trillion there and pretty soon you are talking serious money funneled into the world economy.

Money is akin to water: It seeps through cracks and across borders. The monetary stimulus from the quantitative easing programs of the major central banks acts to lift all boats globally. Big Chinese stimulus will surely have an effect on the U.S. economy, just as how America spends has an effect on the People’s Republic. The Fed’s economists now have to figure if these potential factors compel the U.S. central bank to ease up on its own stimulus.

For the first time in living history, governments and central banks have acted in concert to combat the sharp pandemic recession. (For some, perhaps too close a collaboration.) But more may be required: Recession has been stopped in its tracks and reversed, but big spending — and the potential for runaway inflation — is just getting going.

Apart from the U.S. Congress’s and Xi Jinping’ prospective influence, there are two known knowns for central bank chiefs to consider. On Monday, the International Monetary Fund is unleashing the largest ever allocation of its special drawing rights ($650 billion). This will be targeted primarily towards emerging markets where it will have a seismic effect on vaccination programs in the poorer countries. Also, the European Union will finally put to work the first grants released from the 800 billion-euro ($938.7 billion) NextGeneration EU recovery fund.

This might be coming too late to lend support to U.S. growth which is appearing to be more transitory than high levels of inflation, if recent economic data is any guide. So if Powell comes off as too hawkish in his speech, he risks tipping the world's markets in to a taper tantrum tailspin akin to 2013 and 2018. But if he dithers and delays too much, the window to curtail monetary stimulus — the Fed’s $120 billion monthly QE splurges — will slam shut.

And then there’s the fiscal stimulus effect: The Federal Open Market Committee has to guesstimate how much more money is going to be pumped into the U.S. economy by the Biden administration. Not an easy task. All that money will eventually have an inflationary effect.

The PBOC statement has already had a dynamic turnaround effect on crude oil, iron ore and Chinese tech stocks, showing raised hopes of a sea change in China stimulus. It could be a major turning point after the Chinese credit impulse fell dramatically this year.

All this global monetary and fiscal stimulus may convince Powell to chew things over and decide he needs more time to assess their quantitative and qualitative effects. Unconventional monetary measures — such as QE — have had a waning effect over time but they do grease the wheels for government spending to work more smoothly. Until he knows how much more is coming down the pipe, he will be deeply reluctant to turn off the taps. The life of a modern central banker is not an easy one. There are no prizes for a misstep.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.