For Central Banks, Omicron Is Another Word for ‘Reset’

(Bloomberg Opinion) -- Since the summer, it's not been a fun time to be a central banker: What with not-so-transitory inflation playing havoc with official targets and leading to some pretty terrible attempts at forward guidance. Yes, I'm looking directly at you, Bank of England.

But the Old Lady of Threadneedle Street has not been the only major institution struggling to chart a clear course in the Covid era. Everyone’s been unsettled since the global economy shut down suddenly only to reopen with a jolt. It's a tough balancing act for central bank policymakers to appear competent.

The omicron variant of the coronavirus is a get-out-of-jail-free card to play for more time by blaming acts-of-god. It is a Christmas present come early to be given a chance to buy some time or just to point the finger elsewhere. It will be interesting to see which central bankers this week will say their interest rate stances have to be softened from the hawkishness forced on them by the surging inflation of recent months.

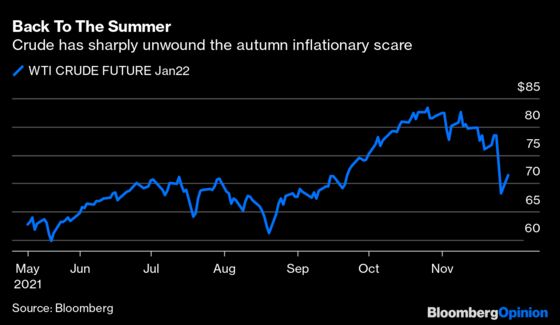

There is just as much fear from the economic recovery hollowing out as there is from runaway inflation. The sharp drop in crude oil is the simplest guide to how much froth has been taken off economic hopes for 2022. We have moved on from the huge collective effort to throw everything possible at the Covid economic recovery to bickering about when the largesse is removed.

The BOE’s Monetary Policy Committee is wrestling with external members — who tend toward dovishness — refusing to be browbeaten again by the full-time internal members pushing for an imminent rate hike. Governor Andrew Bailey and Chief Economist Huw Pill have put themselves through contortions to account for their inability to bend the MPC to their will. It does not make for edifying viewing.

The BOE will certainly not be getting any holiday cards from market participants after its interest rate head fake. Unfortunately, omicron or not, there is no way to divine what the MPC does next at its Dec. 16 meeting. But if it demurs from hiking rates again, be assured omicron will be the star guest.

The Federal Reserve had its own kerfuffle recently over whether Jerome Powell was to be allowed a second term. It was much more about keeping stimulus than personalities — seeing as it was nigh-on impossible to draw any distinction between him and the new vice-chair Lael Brainard. The debate is over when to accelerate the pace of tapering. If omicron does take hold meaningfully in the U.S., then this may well get put on the backburner.

The German Bundesbank President Jens Weidmann threw in the towel last month trying to advocate for a more hawkish stance within the European Central Bank. Though as ever, when a major player capitulates, it leads to a round of soul-searching. That’s what the ECB Governing Council is currently going through as it tries to figure out what replaces the Pandemic QE program and how much of a wider safety net remains.

With the recent weakness in the euro, it would be a very brave ECB that decided — by its Dec. 16 quarterly review — that the EU economy no longer needed all-encompassing monetary protection. This Covid scare will strengthen President Christine Lagarde’s hand in securing a more flexible and powerful replacement.

What was that tinny sound? It'll be the can kicked down the road.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2021 Bloomberg L.P.