Bored Lockdown Traders Are a Danger to Themselves

(Bloomberg Opinion) -- The Reddit-inspired trading frenzy that lured retail investors to invest in GameStop Corp., AMC Entertainment Holdings Inc. and even precious metals in recent days seems to be abating. But bored, housebound punters are likely to continue to click away their lockdown blues by trading securities. The danger is that they’ll erode the value of their investment portfolios by overtrading.

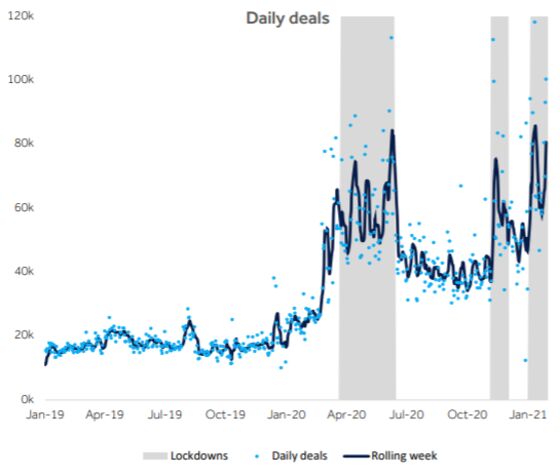

Hargreaves Lansdown Plc, which runs the U.K.’s biggest consumer investment platform serving almost 1.5 million customers, has seen the average number of daily trades it handles double in the wake of the pandemic, to about 40,000 transactions. The firm has seen days in the heart of the country’s lockdowns when more than 100,000 transactions have taken place. When mobility is restricted, trading activity increases.

In the past year, Hargreaves Lansdown, which has about 40% of the U.K. market for retail buying and selling of shares, has enjoyed a 57% increase in customers logging on to its mobile app. What’s astonishing is that they’re checking their investments 10 times a week on average.

The jump in buying and selling activity might not just be down to lockdown boredom. A shift in the demographics of Hargreaves Lansdown’s customer base is also probably playing a part.

The company reckons the average age of its new clients has fallen to 37, down from 45 in 2012. The under-55s now comprise 63% of its customer base, up from 54% nine years ago. With retirement further away for the younger crowd, there would seem to be less risk in trying to juice performance by churning the portfolio more frequently. It’s a temptation that should be avoided.

Overtrading hurts returns. Brad M. Barber at the University of California, Davis and Terrance Odean at the University of California, Berkeley analyzed 78,000 trading accounts, dividing the investors into five classes based on trading frequency. They found that the most patient investors outperformed the most active buyers-and-sellers by 7 percentage points per year.

The mathematics of compounding means that the effect of every lost percentage point of performance has an even greater impact over time. Moreover, a phenomenon known as the disposition effect prompts people to sell winning stocks in favor of holding on to investments they’ve already lost money on. We’re psychologically wired to trade badly. And in building long-term savings, patience is more than a virtue, it’s a necessity: No one should confuse investing with trading, no matter how tempting it is to chase the next hot stock touted on internet message boards.

What’s been called democratization of finance can be a good thing. Individuals are increasingly becoming responsible for building their own retirement savings, taking over from governments and companies as the custodians of the nest eggs needed to ease the financial strains of leaving the workplace. But checking your portfolio 10 times a week is likely to be bad for your long-term returns — as well as your short-term mental health.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2021 Bloomberg L.P.