(Bloomberg Opinion) -- Casino Guichard-Perrachon SA announced late Tuesday that it was working on a 3.5 billion-euro ($3.9 billion) refinancing. That should be positive for the owner of France’s famous Monoprix and Franprix chains. But as usual with the sprawling retail group, there is probably more here than meets the eye.

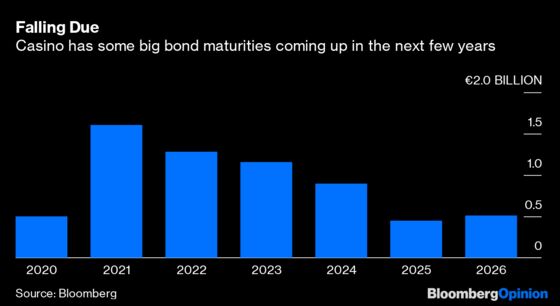

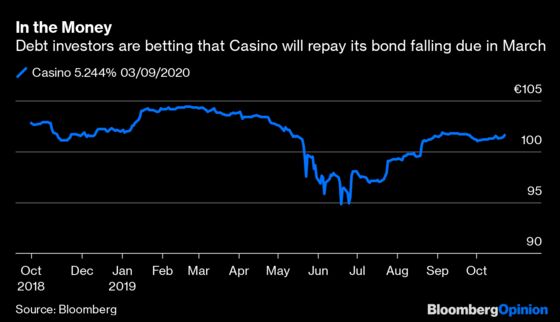

At first glance the move looks like sensible balance sheet management. The company has about 500 million euros of bonds maturing in March 2020, and more over the next few years.

But the refinancing comes at a price. First of all, it is secured over Casino’s main operating assets in France and Latin America, as well as 1 billion euros of real estate. Then, what’s grabbed the most attention, it’s conditioned on restrictions to future dividend payments to shareholders — the largest of which remains Rallye SA, the investment vehicle of Jean-Charles Naouri. (Naouri is also chairman and chief executive officer of Casino.)

The announcement was quickly followed by a long-term debt rating cut by Moody’s Investors Service. Moody’s pointed out that Casino’s overall debt level and interest payments will remain high. It also forecast that Casino’s free cash flow will stay negative despite its best efforts. All of that, plus lingering questions about an August plan to sell an additional 2 billion euros worth of assets in France, makes one wonder whether Casino is being as efficient as it can be managing its debt.

The refinancing, if finalized, will secure a new 2 billion-euro credit facility, maturing in October 2023. The company is also aiming to raise new financing of 1.5 billion euros, maturing in 2024. Part of the proceeds will be used to launch a tender offer for its bonds falling due in 2020, 2021 and 2022.

This should prevent any imminent liquidity crunch as these notes need to be repaid. Standard & Poor’s took Casino off of watch for possible downgrade, although the outlook remains negative. The company also reaffirmed its target of net debt in France of less than 1.5 billion euros by the end of next year.

But why is it still necessary to make sure Casino handles its dividend policy in a sensible manner? Casino had already said that it will not pay a dividend next year, amid fears that it might privilege payouts to Naouri over sorting out its own finances. Under the terms of covenants attached to the refinancing, any future dividend payments will be significantly reduced unless Casino can substantially cut its leverage. Analysts at Sanford C. Bernstein said this implied a 65% cut in any further distributions.

Casino has faced criticism for worrying too much about Naouri’s Rallye, which entered a creditor protection program in May. Rallye owns 52% of Casino and is dependent on income from the retailer to cut its own borrowings.

At this point, the more that Casino can retain cash to pay down debt or invest in the businesses it’s making its focus, such as e-commerce and its premium and convenience stores, the better ultimately for the company.

Naouri already has his hands full working to restructure Rallye’s debt. The prospect of lower dividends payments going forward is bad news.

As for Casino, its shares fell as much as 3% in early trading, before recovering. But it has had a good run, recovering to around 44 euros from less than 30 euros in May. The stock has been buoyed by expectations a shareholder shake-up may be in story after Czech billionaire Daniel Kretinsky and his business partner Patrik Tkac bought 4.6% of the French retailer.

Still, the refinancing is not done yet. The company has secured 1.6 billion euros of the new 2 billion-euro facility. It’s confident it will get the rest. Even when it does, this won’t be the last spin of the wheel for Casino, especially as its relationship with parent Rallye is reshaped.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.