(Bloomberg Opinion) -- Modern finance requires a lot of trust, and its digital future will demand still more. If, for example, electronic payments are to replace cash, people must be willing to believe that the bits of data traveling among phones, cards, terminals and blockchains actually represent something of value.

So will they be? Judging from their growing predilection for physical currency, maybe not.

At first glance, cash would appear to be on its way out. Sweden has almost eliminated its use for payments. In America, home of the almighty dollar, almost a third of the population gets through a typical week without using a single banknote. Businesses are experimenting with going cashless, hoping to speed up transactions, combat theft and create a safer environment for their employees.

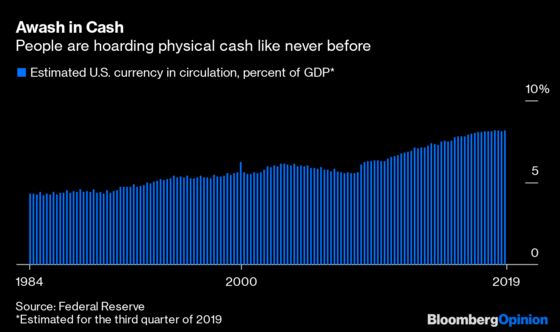

Actually, though, physical currency is experiencing a resurgence. People in many of the world’s most advanced nations – including the euro area, Japan and the U.S. – are holding more of it than ever. In the U.S., for example, currency in circulation stood at an estimated $1.76 trillion as of late September. That’s about 8.2% of gross domestic product, up from just 5.6% before the 2008 financial crisis and close to the highest level in at least 36 years.

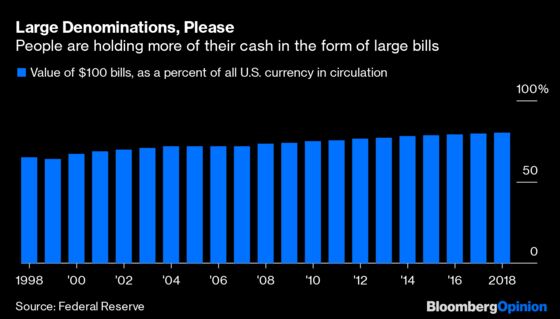

If people need less cash to pay for stuff, why do they want to hold so much of it? The answer, it seems, is that they’re turning to currency as a store of value. Consider the kind of cash they favor: Increasingly, it’s large denominations such as $100 bills, which are the most convenient for stashing away big sums. Benjamin Franklin’s share of total U.S. currency in circulation reached 80% in 2018, up from 73% a decade earlier.

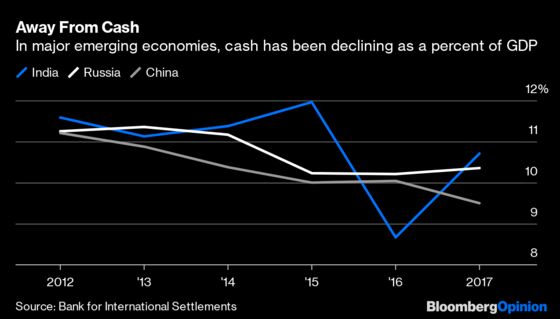

The trend in the developed world contrasts sharply with emerging economies such as China, Russia and India, where currency in circulation has been declining as a percent of GDP:

Why are people in rich nations hoarding cash? No doubt, it has a lot to do with central banks’ efforts to keep interest rates low. When safe investments such as deposits or government bonds yield little or less than nothing, people aren’t missing out by holding paper money. This illustrates why central banks can’t push rates too far below zero: Instead of spending the money or watching their savings shrink while sitting in the bank, people will just withdraw their cash and put it in the mattress.

That said, the surge in demand for currency has been too large for interest rates alone to explain. This presents something of a mystery. Criminals, of course, are avid users of cash, but there’s no particular reason to think that their demand for it would have increased so much in the past decade. On the contrary, the advent of cryptocurrencies has provided them with a viable alternative.

One recent study, by a pair of economists in Asia, found a link to aging populations. It seems that older folks — perhaps because they’re less inclined to trust numbers on a screen — have a greater affinity for cash. So when they make up a larger share of the population, overall currency holdings also go up. This might also help explain the contrast with emerging economies, where population aging is less of an issue (and where interest rates haven’t been as low as in the developed world).

The most troubling possibility is that people are losing faith in financial institutions more broadly. The surge in cash began immediately after one of the worst financial crises ever — and has been concentrated in the affected countries. Granted, one wouldn’t expect the effect to keep growing over time. But perhaps persistent scandals — such as those involving fake accounts, manipulative fees and the theft of personal data — have compounded the problem.

Trust might also have something to do with the opposite trend in emerging economies. To be willing to hoard cash, people must have a certain amount of confidence in a government’s ability to manage its legal tender. In developing countries, this confidence is often lacking. Consider India’s 2016 “demonetization,” in which the government pulled large-denomination banknotes out of circulation and replaced them with new bills. The move didn’t disrupt the shadow economy as intended, but it did undermine the currency: Cash holdings have yet to recover to their pre-reform level.

Cash accumulation can go only so far as a sign of trust in government. After all, governments in the developed world would typically like to see more electronic payments. Getting rid of cash can have a lot of benefits: It can help deter crime, reduce tax evasion and give central banks more power to stimulate the economy. But people have to believe that electronic money will be safe from mismanagement, man-made disasters, hackers and even confiscation. So far, neither the denizens nor the overseers of the financial system have done a great job of earning that trust.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Leonid Bershidsky is Bloomberg Opinion's Europe columnist. He was the founding editor of the Russian business daily Vedomosti and founded the opinion website Slon.ru.

Mark Whitehouse writes editorials on global economics and finance for Bloomberg Opinion. He covered economics for the Wall Street Journal and served as deputy bureau chief in London. He was founding managing editor of Vedomosti, a Russian-language business daily.

©2019 Bloomberg L.P.