(Bloomberg Opinion) -- A bidder offers a 650 million-euro ($740 million) premium for a smaller rival and the stock market rewards it by raising its own market value by 1.3 billion euros. No prizes for guessing who got the better side of the deal in Capgemini SE’s agreement to by smaller French consulting peer Altran Technologies SA for 3.6 billion euros in cash. Altran shareholders should ask whether management got the best price.

The acquisition makes strategic sense, adding engineering and R&D services to Capgemini’s core IT consulting offer. The buyer’s growth has been less impressive than that of peers lately, and sensible M&A offers the potential for a pick-up.

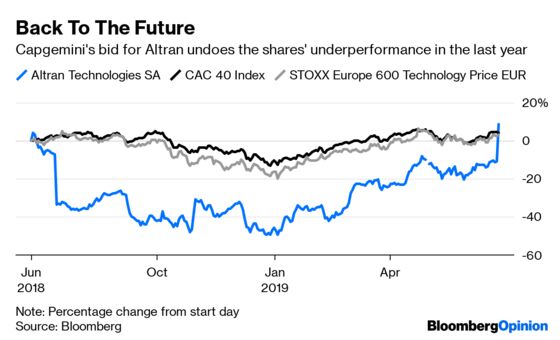

Financially, the transaction looks good value for Capgemini. Altran’s shares collapsed last year after the group revealed a forgery in the Aricent business it acquired from KKR & Co. While the stock had recovered a lot prior to Capgemini’s deal, the damage wasn’t fully repaired. The takeover premium here is a humdrum 22% over Monday’s closing price and a more conventional 30% only when measured over the last three months’ average.

A year ago, Altran implied it had the capacity to be generating nearly 600 million euros of operating profit in 2022. Add to that cost savings of around 85 million euros – the middle of the range Capgemini says is achievable – and the total 5 billion-euro investment (including assumed net debt) looks capable of earning a 9% post-tax return inside three years. That should be good enough for Capgemini shareholders. And revenue synergies would only lift this higher.

True, this is a relatively large purchase for Capgemini, capitalized at 19 billion euros, so integration could be a distraction. The company’s leverage will shoot up, given the cash paid out to Altran’s shareholders and the target’s existing high leverage following the Aricent deal. But these additional risks are tolerable given the overall logic.

As for Altran shareholders, they get an offer valuing the group roughly where Capgemini trades on forward earnings. The target doubtless feels the offer captures the value of its own strategic plan, otherwise it wouldn’t be recommending the transaction. Still, it looks like Capgemini could have afforded to pay more here.

Altran shareholders will hope for a counterbid. Accenture may be tempted to look, although the target could be too big, and Capgemini already has backing from shareholders with 11% of the stock. The shares, trading just below the bid, aren’t pricing in a gatecrasher. It would take an activist and full-blown shareholder rebellion to force Capgemini higher.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.