Can Moderna Buy Its Way Into the $200 Billion Club?

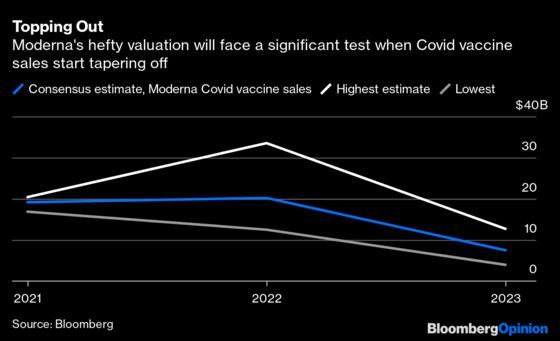

(Bloomberg Opinion) -- Moderna Inc.'s highly effective Covid vaccine, in addition to protecting millions, is officially a cash cow. The company disclosed during its earnings presentation Aug. 5 that it expects the shot to generate $20 billion in sales this year. Now it has to figure out what to do with its windfall as it tries to justify a market valuation that has surged by more than $100 billion since May. That's a nice problem to have. But it's also an urgent strategic issue.

The Cambridge, Massachusetts-based biotechnology firm’s astonishing stock surge has been driven by the success of its vaccine and excitement about its underlying messenger RNA technology, which it is also employing in other shots and treatments in early stages of development. As of now, though, the Covid jab is the company's only approved product, and its finite future sales depend on the very uncertain trajectory of the pandemic and booster shots.

Single-product companies are usually targets rather than buyers when it comes to biotech. But Moderna is in the rare position of having the firepower to go on the hunt itself. M&A makes sense; it’s certainly a better alternative to buying back $1 billion worth of its inflated shares, which the company also plans to do. But don’t expect acquisitions to solidify a valuation that has somehow surpassed that of McDonald’s Corp. and Morgan Stanley.

Moderna has plenty of deal capacity, with $12.2 billion in cash on hand and more coming in, as well as highly valuable stock and minimal debt. But it plans to be very particular about what it buys.

On its Aug. 5 earnings call, Moderna CEO Stephane Bancel said the company would only invest in new areas that are complementary to mRNA, which the body uses to give cells instructions. Bancel specifically said the company is interested in gene editing and gene therapy and that it won’t invest in small-molecule or antibody drugs — tried-and-true approaches that are used in most available and best-selling medicines. This focus on newer technology rules out many targets and means investors shouldn't expect deals to diminish the company’s risky Covid sales cliff, which will arrive well before its internal drug pipeline is ready to contribute.

Gene-editing companies such as Intellia Therapeutics Inc., Crispr Therapeutics AG, and Beam Therapeutics Inc. are substantially more affordable and quite promising. All three aim to treat and potentially cure diseases by modifying DNA, which stores instructions that RNA delivers, and use mRNA as part of their process. On top of adding valuable expertise in genetic medicine, a deal for one of these companies would boost the ratio of treatments in Moderna’s pipeline. That might be wise, because vaccines are less profitable outside of a pandemic.

But even relatively advanced companies in that field are still in very early stages of development and they wouldn’t add sales soon or do much to improve Moderna’s risk profile. The company already plans to spend heavily on new medicines; it's working on more than 20 drugs that apply mRNA in six different ways. All are likely at least a few years away from market; several face strong competitors, and its non-vaccine projects are largely unproven. Planting a stake in another still-developing area of medicine, even if it’s complementary, could increase the company’s cash drain and downside potential.

Moderna’s strategy could pay off if investors are very patient, and the company certainly seems to have lots of believers in its long-term future. But their conviction and Moderna’s valuation haven’t really been tested yet. If the Covid booster market peters out sooner than expected or Moderna has a significant pipeline hiccup, look out below.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2021 Bloomberg L.P.