Buyout Firms Explore New Lows in the U.K. Bargain Bin

(Bloomberg Opinion) -- Buyout barons are regaining their appetite for U.K. assets and London-listed stocks. They’re also becoming more aggressive in their tactics. The idea that British takeover rules are a deterrent to private equity bidders faces a fresh test.

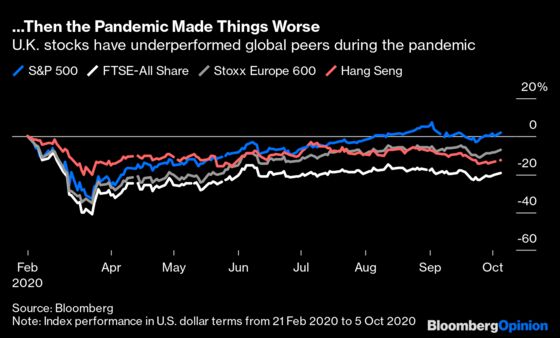

U.K. stocks have been unloved since the Brexit referendum. The pandemic has compounded investors’ wariness. A decisive election result in December provided some respite. But the FTSE All-Share Index has still starkly underperformed other major indices since late February.

A shortage of buyers in any market is a magnet for private equity. There were competing buyout bids for Walmart Inc.’s sale of a majority stake in U.K. grocer Asda. Trustbusters had already vetoed a domestic merger. One of the failed bidders, Apollo Global Management Inc., was simultaneously trying to buy listed bookmaker William Hill Plc, which has since agreed to a takeover by joint venture partner Caesars Entertainment Inc.

There’s a perception British takeover regulations hamper so-called take-private deals. Reforms were introduced in 2011 following Cadbury’s controversial purchase by what’s now Mondelez International Inc. Any leak of an approach requires the target to name the suitor, who must then formalize an offer within 28 days or walk away.

Private equity firms don’t like the idea that their tentative prospects could be made public given so many talks fail. The timetable is also tight for negotiating a price, conducting due diligence and securing financing. Meanwhile, hostile deals made over the heads of managers face due diligence snags and undermine buyout firms’ attempts to market themselves as a friendly corporate partner.

So the theory goes. In fact, deal activity held up after the rule changes, and there were several big U.K. take-private deals in defense engineering, satellites and theme parks in the year preceding the pandemic. Sterling’s weakness has helped and bidders know it may not last.

Now, if anything, private equity is getting more aggressive. GardaWorld’s hostile bid for rival security firm G4S Plc is backed by cash from 51%-owner BC Partners. True, it’s less risky for BC to support a portfolio company in a hostile takeover than to pick a fight on its own. Its Canadian partner knows the industry well, and any future problems with G4S would be shared. That’s safer than a leveraged buyout of just G4S without due diligence.

The confrontational tactics may help flush out the price at which G4S’s investors and the board will roll over. But they risk setting the tone for any future deals attempted by BC. Evidently, the firm is comfortable with that.

These are particularly fraught times for U.K. companies to be on the receiving end of a takeover. Executives’ instinct will be to argue their firm’s standalone value is much higher than its current share price implies. For the average stock, a conventional one-third takeover premium would only match the pre-Covid high — a level most boards would have thought was already depressed due to Brexit. But it may be where private and public equity investors are able to meet.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2020 Bloomberg L.P.