Buy-the-Dip Bond Traders Are Scared of Momentum

In a vicious reversal, 10-year U.S. Treasury yields rise the most since November 2016 on sudden optimism.

(Bloomberg Opinion) -- During one of the strongest bond market rallies in history, the mantra “buy the dip” sounded like a pretty sound trading strategy. Actually executing that plan appears to be a different story.

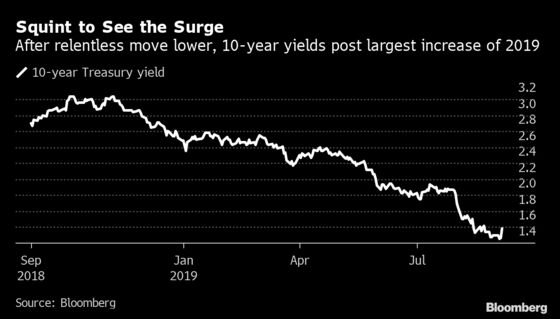

Benchmark 10-year Treasury yields rose as much as 12 basis points on Thursday, the biggest intraday increase since November 2016. A combination of factors, including news that China and the U.S. would hold trade talks in early October, better-than-expected jobs data from the ADP Research Institute (accompanied by a presidential tweet) ahead of the Labor Department report on Friday, and the sharpest monthly rebound in business activity since early 2008 all fueled optimism that the global economy might yet avert a widespread recession. Even German 30-year yields turned positive for the first time in a month.

And yet it feels like one of the most insignificant double-digit basis point yield increases in recent memory. After all, as Bloomberg News reported, central bank policy makers have cut interest rates 32 times this year by a cumulative 13.85%, according to data from the Bank of International Settlements that track 38 central banks. For the Federal Reserve, it’s less a question of whether it will lower rates again later this month but by how much. Gary Shilling, writing for Bloomberg Opinion, reiterated that Treasury yields have yet to see a bottom. Alan Greenspan said again this week that it was only a matter of time before negative interest rates reached America’s shores.

It’s possible that the bond market has it all wrong; that traders went too far and talked themselves into a recession because of the inverted yield curve, but in reality the trends in the U.S. and global economy aren’t so dire. Thomas Simons at Jefferies quipped after the ISM non-manufacturing index beat expectations that “as has been the case many times over the past decade, reports of the demise of the U.S. economy have been greatly exaggerated.”

It’s also possible, as Bloomberg News’s Cameron Crise wrote, that “bonds have hit something of an extreme” and are due for a correction. There’s certainly no shortage of investors on edge about a bond bubble.

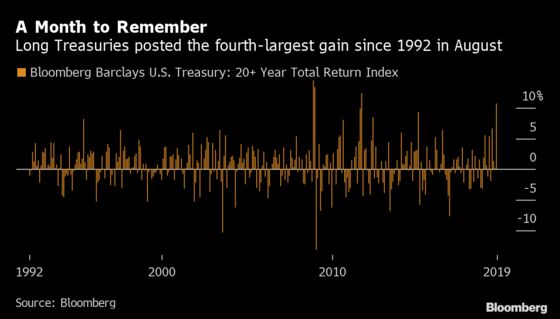

However, it’s going to take more than one bad day to convince me that the massive repricing in August will reverse itself. Those who closely track the swings of the world’s biggest bond market seem to agree. This big move feels like little more than a fleeting turn in momentum after what was the fourth-strongest monthly performance for the longest-dated Treasuries in the past 27 years (or more than 300 months).

Jim Vogel at FTN Financial Capital Markets published a note (almost at the exact same time I started writing this) that said Treasuries maturing in five to 10 years were all “in the buy zone.” He urged traders not to wait to see what happens and whether the sell-off could deepen. “The move has such a big increase in real yields and decrease in risk premiums that it allows for an easy reassessment as early as this afternoon.” At the time of his report, 10-year yields were about 1.586%. He advocated buying until they fell back to 1.555%.

So far, though, dip buyers have been reluctant. It’s admittedly hard for many investors to get excited about these yield levels. Yes, they’re at a nearly two-week high, but as recently as April they were a full 100 basis points higher. The all-time low set in 2016 is 1.318%. The U.S. long bond is comfortably above 2%, and 30-year debt in Germany briefly rose above 0%, both of which seem like small victories for those who still believe in positive interest rates.

Ask most bond traders whether Treasury yields have reached a bottom, though, and I’d wager a sizable majority would say no. And yet there are still days like this in which yields can spike higher with few buyers in sight. Buying the dip and surfing the ranges is all well and good until a massive wave of momentum knocks you over.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.