(Bloomberg Opinion) -- A new government with an ambitious fiscal plan should be bold in how it finances such a rapid increase in state spending — especially with money so cheap.

Boris Johnson has won an impressive electoral mandate for his Brexit deal, regardless of the slightly overdone jitters around sterling related to his 2020 deadline for a European Union trade deal. So with interest rates at near record lows, why not follow the lead of Austria and lock in those rates for the ultra-long haul with a 100-year government bond?

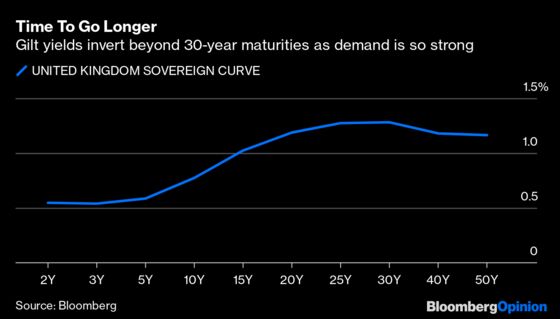

The U.K. has the luxury of a deep investor base that hoovers up long-dated, fixed-income assets to make sure it can meet its future pension and insurance liabilities. So much so that the yield on 50-year Gilts is lower than that of their 30-year counterparts, meaning there’s a so-called inversion at the long end of the U.K. yield curve:

The average duration of British government debt is much longer than that of its main counterparts; it’s about 14 years, compared to nearly nine years for German bunds and less than seven years for U.S. Treasuries. There is evidently investor demand in the U.K. for longer stuff, but it requires a genuine commitment from the government to stay the course and not leave any ultra-long issue stranded at the end of the yield curve.

Doing a 100-year deal in concert with more 30- to 50-year issuance would make sure there was plenty of interest at various maturities at the long end of Gilts. A century bond could rapidly build scale into the tens of billions of pounds with quarterly auctions, perhaps with a coupon of about 1.5% (by comparison, Austria’s 100-year issue went for 1.17% back in June). This would be a super-cheap way to really commit to some of the biggest infrastructure projects, such as connecting rail links properly in the north of England.

With countries as diverse as Argentina and Austria taking the plunge — albeit in one-off or limited deals, and with very mixed results — it’s time for a major bond market to step up. The U.S. Treasury is actively mulling the 100-year idea, and the U.K. is well positioned to take a lead by making it an active part of its regular issuance program. Having plenty of volume would allow the trading of derivatives such as futures, options and swaps to flourish too, thereby building a proper ability to hedge and widening the investor base further.

If the U.K Treasury wanted to go the whole hog and follow France's example, this could even be a green bond linked directly to sustainable infrastructure spending. How’s that for long-term virtue-signalling.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.