(Bloomberg Opinion) -- From Donald Trump to Emmanuel Macron to Boris Johnson, world leaders have rushed to echo Mario Draghi’s words as the European Central Bank prepared to deal with the financial crisis: We will do “whatever it takes.” And yet there is no consensus on what exactly is required — not on the magnitude of relief, not on the timing of different measures, not on how to target and deliver it.

If size is mainly what matters, Britain has so far been out in front. Trump may be planning a $1.2 trillion relief package. But the one that U.K. Chancellor of the Exchequer Rishi Sunak announced Tuesday — 350 billion pounds ($424 billion) in loans, grants and tax relief — is 1.7 times larger on a per capita basis.

The biggest difference between the as-yet theoretical Trump plan — which includes direct cash payments to individuals — and the Johnson-Sunak plan is the share of loans versus grants. Small and medium-sized businesses can tap the new Business Interruption Loan Scheme (announced in the recent budget) and smaller businesses can borrow up to 5 million pounds interest-free for six months, with most of the loan amounts guaranteed by the Exchequer to encourage continued bank lending.

Larger companies will have access to the new Covid Corporate Financing Facility from the Bank of England, a temporary scheme by which the BOE buys short-term debt issued by companies with terms that the Bank says will be near those that prevailed in the market before Covid-19 hit. There’s also the question of how long a loss-making company can stay afloat under U.K. company law.

The main point of going bold is as much psychological as financial — to convince businesses and consumers that the economic fallout will be contained and support will be provided. If people aren’t panicked about losing their jobs, they are more likely to follow instructions to self-isolate. If businesses have confidence that they can ride out the crisis, they are less likely to lay off workers. And yet while the generosity of the package is clearly important, so is the targeting and the transmission mechanism. In that respect, the U.K. still has a lot to do.

There is some direct relief in Sunak’s new measures. U.K. businesses in the hospitality, leisure and retail industries will not have to pay so-called business rates, or the tax on properties used for commercial purposes, for the next 12 months. The Treasury has given companies more time to pay their tax bills and waived the usual 3.5% annual interest on deferred tax payments. For businesses in those sectors valued at less than 51,000 pounds, there will be cash grants of up to 25,000 pounds to tap.

And yet these may end up building a tent to fend off an avalanche. The targeted aid reflects the fact that the U.K. is largely a services economy, but other industries outside the three most-protected sectors will be hit. A company that is facing a long period of collapsed revenue and no immediate prospect of recovery is going to lay off workers before it will take on debt that it will eventually have to repay. None of the government’s measures are going to convince them otherwise.

The Johnson-Sunak plan, as Labour leader Jeremy Corbyn noted in Parliament Wednesday, also does little for those on low pay, the self-employed and other vulnerable workers. That includes those in the gig economy, which now employs nearly 5 million people. Many will lose their income during this period and yet have no access to sick pay or other relief.

Even for those in regular work, Britain’s mandatory sick pay is low by European standards — only 94.25 pounds per week. That is too little to support many households. And while the poorest can be helped through the welfare system, the bureaucracy is onerous. At present it takes five weeks before support is received and there are many hoops to jump through first.

Finally, while there is mortgage payment relief for homeowners (which is straightforward to administer through the banking sector), there was still a need for measures to keep those in private rental accommodation from being turfed out (trickier to implement). In the decade to 2017, the number of households in the rental sector increased by 63% to 4.5 million. And while they tend to be largely younger households, at least 16% of them have members over the age of 45. On Wednesday, Johnson announced he would introduce legislation to prevent evictions due to coronavirus consequences — one sign of how we are likely to see frequent changes, especially once new emergency powers are granted.

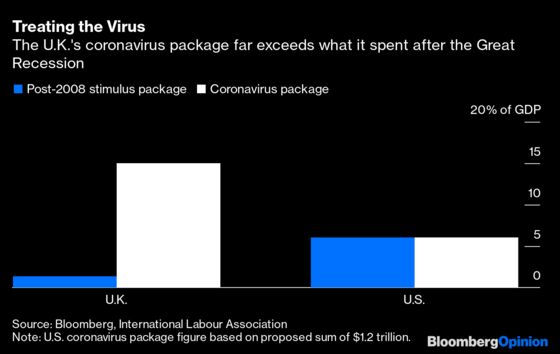

The current U.K. package amounts to an impressive 15% of GDP (compared to about 6% for Trump’s moves) and far more than the 45 billion euros ($49 billion) of measures announced in France. But even more measures to address these gaps are likely still to come along, with more from the Bank of England. Anticipation for just that has helped send yields on U.K. 10-year government debt to the highest levels they’ve seen since January.

The U.K. is not yet considering a basic-income type experiment of the kind Trump is pushing — putting cash directly in people’s hands — but such handouts have the benefit of being immediate and, well, liquid. Sunak may yet have to think again about whether a loan-based program targeting specific sectors will do enough.

Welcome to the Age of the State. As my colleague Pankaj Mishra has written, government is going to be a much more central part of economic life for some time to come and that will have all sorts of consequences. How quickly the U.K. economy recovers from this crisis depends not just on how long it takes to find a vaccine or stop the virus’s spread, but whether the measures crafted now provide a sound enough floor for consumers and businesses so they can recover once the avalanche passes.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Therese Raphael writes editorials on European politics and economics for Bloomberg Opinion. She was editorial page editor of the Wall Street Journal Europe.

©2020 Bloomberg L.P.