Bristol-Myers's $74 Billion Celgene Splurge Just Got Riskier

(Bloomberg Opinion) -- Bristol-Myers Squibb Co. really wants to get its $74 billion deal for Celgene Inc. done.

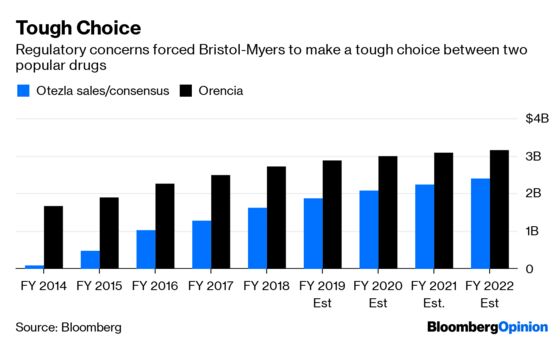

The pharma giant announced Monday that it is planning to divest Celgene’s blockbuster psoriasis medication Otezla to address concerns by the Federal Trade Commission likely related to potential market concentration. Bristol-Myers has a competing product in late-stage trials and a marketed inflammation drug of its own in Orencia. It had previously hoped to close the deal by Sept. 30. Now it is targeting the end of the year, or early 2020.

The FTC’s unexpected objection – analysts didn’t think divestitures would be required – demonstrates the hidden perils of drug megamergers and adds risk to what was already the year’s priciest pharma deal.

Regulators seemingly don’t want Bristol-Myers to retain all three assets. If one had to go, it makes some sense that it’s Otezla. Orencia generates more revenue, but Otezla has a longer runway and more growth potential. That could see it achieve a comparatively higher multiple in a sale. As for Bristol-Myers’s pipeline drug, a sale wouldn’t impact current cash flow as the medicine is still in development, but it might not bring much of a return or assuage regulators.

Even if selling Otezla is the right call, it’s a tough decision and will hurt. Otezla accounted for 10% of Celgene’s sales last year, and creating an industry-leading inflammation franchise was a big selling point for the deal with Bristol-Myers. The combined company will have significantly less scale in that area now.

Bristol-Myers also may have trouble getting the price it wants for a valuable asset through this pressured process. The FTC’s objections to this part of the deal are surprising. Orencia and Otezla work in different ways, and overlap in just one of their several indicated uses. The competitive threat from the pipeline drug is still entirely theoretical.

The high regulatory bar that Bristol-Myers has revealed could limit the pool of potential buyers. Many of the big pharma companies that are most likely to be interested in Otezla are already big players in inflammation. Add in the fact that Bristol-Myers is in a weak negotiating position, and you have a recipe for a soft price.

Biopharma companies that attempt large deals love to talk up potential synergies and increased muscle. But those transactions are always more complicated than the sales pitch indicates, and the sacrifices required to get them done have a cost.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.