Boris Johnson Is About to Meet Cold, Hard Economic Reality

(Bloomberg Opinion) -- Don’t be fooled by the slight rebound in the British economy in May.

The country’s gross domestic product rose by 0.3% from the previous month, after falling by 0.4% in April. Investors would be wrong to take this as a sign that U.K. Plc is in good health. Most indicators show signs of prolonged weakness. The likelihood that Britain might crash out of the European Union without a deal is rising as the arch-Brexiter Boris Johnson prepares to take over as prime minister. Such a rupture would spell enormous trouble for the economy.

Britain’s return to growth in May was largely a product of the vagaries of the Brexit process. Many manufacturers – including several car companies – prepared for the initial deadline of March 29 by shutting down production in April. Now that Britain’s departure has been postponed until at least the end of October, the factories roared back. Manufacturing as a whole rose 1.4% on a monthly basis, pushing up headline growth.

If you look beyond this erratic move, however, the picture is much gloomier. The services sector, which accounts for nearly four-fifths of the British economy, was flat in May. The Purchasing Managers’ Index (PMI), a widely-gauged measure of activity, points to a contraction in manufacturing and construction in June, while services still appear to be static. Economists expect GDP to have shrunk mildly in the three months to June, the first quarterly contraction since 2012.

It would be wrong to blame this slowdown entirely on Brexit. The global economy decelerated in the first half of this year, prompting the U.S. Federal Reserve and the European Central Bank to consider further monetary easing. On Wednesday the European Commission cut its euro zone growth forecasts for 2020 to 1.4% from 1.5%, saying there was a risk of further downgrades. The U.K. is an island nation but it cannot isolate itself from what happens in the wider world.

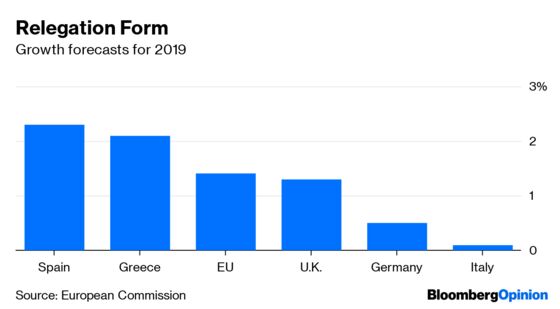

Still, Brexit is an undeniably distinguishing factor for the U.K. economy – and not in a good way – with the country slipping to near the bottom of the EU growth league. According to the Commission, the U.K. will expand by 1.3% in 2019, even assuming there’s no disruption to trading patterns (a big assumption given Johnson’s proclaimed happiness with a no-deal Brexit on Oct. 31).

In fairness, the economy is growing faster than Italy or Germany, but it’s just below the EU average and well below Portugal, Ireland, Spain, and even Greece. Investment rose slightly in the first quarter of the year but it remains weak by historic standards. Uncertainty over the Brexit process may not have been as harmful as some economists expected, but it’s taking a toll.

The trouble is that the concerns over the future relationship with the EU are bound to get worse. Johnson’s Brexit position – that the EU will allow the U.K. favorable trade terms even after a no-deal Brexit – is a mixture of fantasy and dishonesty; it’s bound to crash and burn when confronted with reality.

Investors would be wise to brace for a turbulent few months. In fact, they already are. Sterling is falling sharply even though other major central banks are taking a more accommodating stance on monetary policy, which should push down the value of their currencies. This week sterling touched its lowest level against the dollar since April 2017. A pound will now buy you 1.11 euros, down from nearly 1.18 euros in early May.

For the Bank of England such weakness poses a dilemma. It is confronting rising wage pressures, making it it more likely that inflation will exceed its target of 2% in the medium term (it stood at exactly 2% in May). At the same time, though, a more depressed outlook and the rising chance of a disorderly Brexit will create an opposite pressure to hold or cut interest rates.

Governor Mark Carney has little choice but to wait and see for a bit longer. The future of the country’s economy depends on Johnson now. Despite all of his self-declared “optimism,” this is not a reassuring prospect.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2019 Bloomberg L.P.