Brexit and Neil Woodford Are Bad News for the City of London

(Bloomberg Opinion) -- Regulators in London and Paris are mulling separately whether they need to revisit the rules governing fund managers’ investments in illiquid securities. If they reach different conclusions, it could signal a fracturing of the post-Brexit financial landscape that might cost the U.K. asset management industry dearly.

With clients of the struggling money manager Neil Woodford unable to withdraw their money from his flagship fund since June and H2O Asset Management seeing billions of euros pulled from its funds in recent months, the risks posed by firms that offer daily redemption rights to customers while buying hard-to-trade assets have been shown up starkly.

With both of those portfolios managed in the U.K., alongside the funds that Swiss firm GAM Holding AG froze a little more than a year ago, London’s Financial Conduct Authority finds itself at the sharp end of the problem. Unfortunately, at a time when a coordinated response is sorely needed, its relations with the Paris-based European Securities and Markets Authority are strained.

The debate could set the tone for how British and European markets regulators work together after Brexit. So far, the signs are far from encouraging.

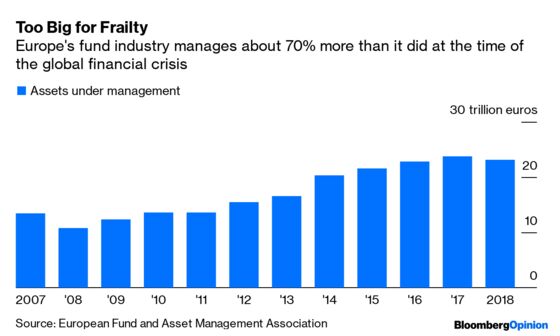

Regulators are right to be worried about what the custodians of the savings industry are doing with our nest eggs, given the explosive growth in how much money we entrust to them. In the decade or so since the global financial crisis, the amount managed in Europe by fund companies has increased by about 70% to reach 23.1 trillion euros ($25.4 trillion), according to a report published this week by the European Fund and Asset Management Association.

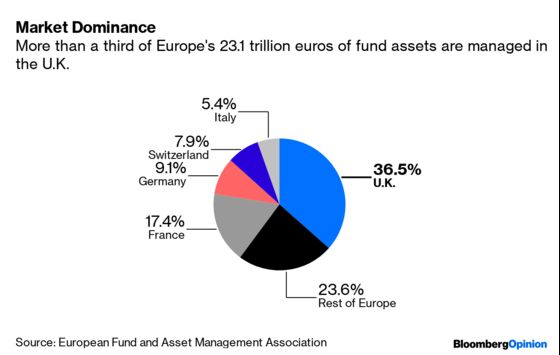

For context, the asset management industry is worth 134% of Europe’s gross domestic product, up from 102% in 2007. And when it assessed where the assets are managed, the EFAMA found more than one-third of the money is being run out of the U.K.

Of the 4,400 asset management companies registered in Europe, about 1,100 are in the U.K. compared with 630 in France and 380 in Germany. Moreover, EFAMA reckons that 40% of the 8.67 trillion euros managed in Britain comes from foreign clients — money that might otherwise be managed in Frankfurt or Paris or Milan.

That’s a prize worth fighting for. And it forms the backdrop to recent spats between ESMA and the FCA.

The European regulator’s threat to bar firms it oversees from trading shares on London exchanges after Brexit (if it doesn’t deem U.K. rules to be equivalent to its own) is evidence of the growing tetchiness between the two sides. In a speech earlier this week, the FCA chief executive Andrew Bailey said that dispute raised the risk of market liquidity being “damaged to no good end.” ESMA, though, is sticking to its guns.

The question of how to respond to funds dabbling in illiquid investments has laid bare an even bigger disagreement on how the two regulators approach fund industry oversight.

ESMA’s chairman Steve Maijoor told the Financial Times this week that “we need to be careful” about changing the existing rules on hard-to-trade investments. That framework already has “clear principles” that portfolio managers must follow, he said. Contrast that with Bailey’s comments in June, when he said Woodford had been free to indulge in “regulatory arbitrage” that could have been avoided by regulations “based more on principles” than what he called an “excessively rules-based” approach.

With Britain due to leave the EU at the end of next month, the antagonism between the regulators could hardly be worse-timed. And with several trillion euros of business at stake, neither side has much incentive for rapprochement. The U.K., though, has most to lose.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.