Brexit and High Wages Are a Poisonous Mix for the Bank of England

(Bloomberg Opinion) -- Three years on from the U.K.’s vote to quit the European Union, its failure to come up with a realistic plan for how to withdraw is pretty farcical. Officials at the Bank of England aren’t laughing, though.

Mark Carney, the bank’s governor, has gone slowly on raising interest rates as he waits for the fog of Brexit to clear. It’s been a protracted and fruitless delay. The longer the unhappy process drags on, the harder it is to ignore what’s happening in the country’s economy.

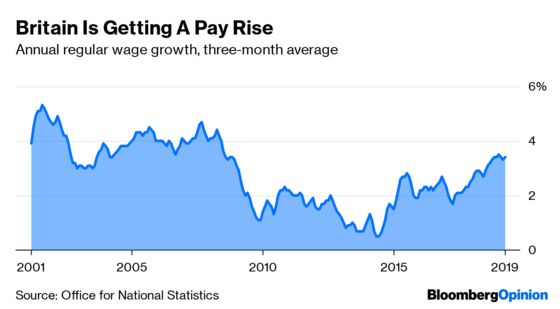

This week, official statistics showed that annual growth in basic pay climbed to 3.4% in the three months to April. The labor market, which has stayed resilient since the 2016 referendum even as investment in the U.K. has fallen, shows no sign of weakening. Unemployment stands at 3.8%, while the employment rate is 76.1% — the highest level on record.

As the labor market tightens, workers demand higher wages. But Britain’s dismal productivity performance means there’s little room for this to happen without stoking inflation. (That’s because unless an employee starts producing more output per hour, any salary hike would have to be paid for by raising prices for customers.)

Under normal circumstances, the BoE would be thinking seriously about raising interest rates from their existing level of 0.75% to counteract the effect of rising pay. Its mandate is to keep inflation at 2% over the medium term, and accelerating wages suggest an economy that might be overheating.

These are hardly normal times, however. The other EU member states have granted Britain an extension to the Brexit deadline as the U.K. Parliament seeks to build a consensus around a withdrawal plan. All options — including crashing out of the EU without a deal — remain firmly on the table. It would be risky to tighten monetary policy right now, given the uncertainty about the possible impact on the British economy.

Yet the case for holding fire as Brexit is resolved is becoming flimsier by the day. Ideally, the U.K. government would set out a clear departure path for its citizens (and the BoE’s rate-setters), whether this meant an orderly exit with a negotiated transition or a sudden break. The bank would at least then be able to assess the economic outlook, weigh the different risks, and set monetary policy accordingly. But it’s impossible to read which way the politicians are headed, and it’s not getting any clearer. Maybe they’ll return to voters for a new referendum or general election. This would just prolong the wait for the policy makers.

Some members of the bank’s Monetary Policy Committee are getting twitchy about the delay. “I want to stress that the MPC does not necessarily have to keep rates on hold until all Brexit uncertainties are resolved,” Michael Saunders said on Monday, adding that interest rates may need to rise faster than the market expects. Ben Broadbent, deputy governor, and Andy Haldane, the BoE’s chief economist, have also struck a hawkish note.

They should tread carefully. There are signs that the recent wage spike may be down to one-off factors, especially in the public sector. Inflation stood at 2.1% in April, which is only just above the bank’s target. The global outlook is gloomy because of the trade standoff between America and China. From the U.S. Federal Reserve to the European Central Bank, some of the world’s leading monetary authorities are getting ready to inject more stimulus. That should make the BoE think hard about hiking rates.

Still, as the Brexit process drags on endlessly, it will become more and more difficult to simply wait for its resolution. Central bankers can’t do the job of politicians. Nor can they wait forever while members of Parliament make up their minds.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2019 Bloomberg L.P.