(Bloomberg Opinion) -- After several dismal years, hedge funds are back in favor with investors. Improved performance is luring cash back into the industry. So much so that one of the most storied firms in the industry is making a smart decision to limit the size of its assets to preserve its ability to generate alpha.

Brevan Howard Asset Management LLP has closed its two biggest funds to new money, my Bloomberg News colleague Nishant Kumar reported last week. One, the Brevan Howard Master Fund, more than doubled since the start of 2020 to top $7 billion. With a total of $16 billion of assets, the firm remains one of the biggest players in the global macro space.

Having more money banging on the doors than you’re comfortable managing is a nice problem to have. Research abounds arguing that funds that grow too large struggle to replicate the returns that made them popular in the first place.

A study by the CFA Institute, for example, found that as assets under management grow, decisions are more likely to be made by teams rather than individual managers, resulting in “more expensive and less timely decisions.” Research by Rutgers University argued that capacity constraints arise both because more money chases fewer opportunities, and because of the difficulties of trying to scale up the abilities of individual managers. So the Brevan Howard decision to resist gathering additional assets is probably wise, even as the investing environment is improving.

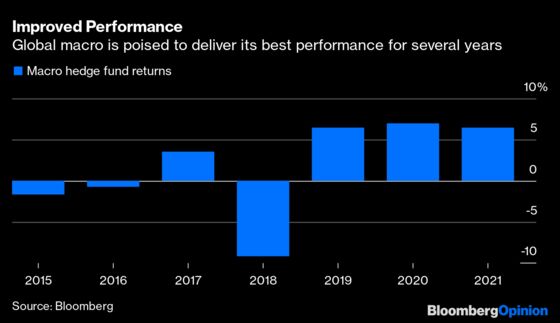

Global macro, which makes investment decisions based on the economic relationship between asset classes and markets, is where Brevan Howard’s billionaire founder Alan Howard made his money. It struggled in the wake of the global financial crisis, with central banks relentlessly pumping money into the markets. A shift toward more normal monetary conditions, albeit one that was blown off course by the pandemic, allowed the strategy to start making money again.

Those better returns are finally winning back customer cash. In the first five months of the year, macro strategies have attracted net inflows of more than $5.6 billion, after clients withdrew $14 billion last year and more than $20 billion in 2019, according to data compiled by research firm eVestment. In April, 70% of macro funds drew in fresh cash, compared with about 57% for the industry as a whole, the data show.

Those return figures just reflect the average performance. Some macro portfolio managers will have outstripped their peers, while others will have lagged. Brevan Howard’s flagship fund, for example, posted a 27.4% gain last year for its best outcome since it opened for business in 2003. Chris Rokos’s macro fund climbed by 44% in 2020. Soros Fund Management, founded by legendary investor George Soros, returned almost 30% in the 12 months through February under the stewardship of Chief Investment Officer Dawn Fitzpatrick.

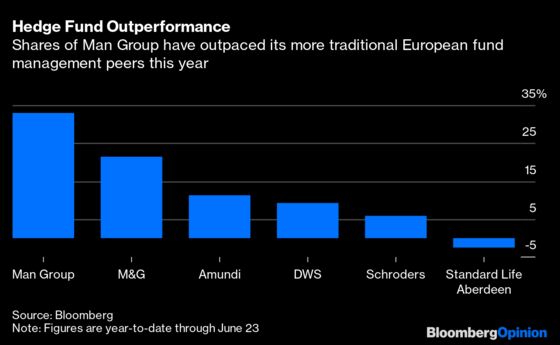

Stock pickers have also noticed the improved outlook for the most speculative fund managers. Man Group Plc, the world’s biggest publicly traded hedge fund, has seen its shares climb by a third this year, handily outpacing its more traditional European money management rivals. While the more vanilla fund firms are occupied eyeing each other up in anticipation of a wave of consolidation, the hedge fund gang can get on with making money.

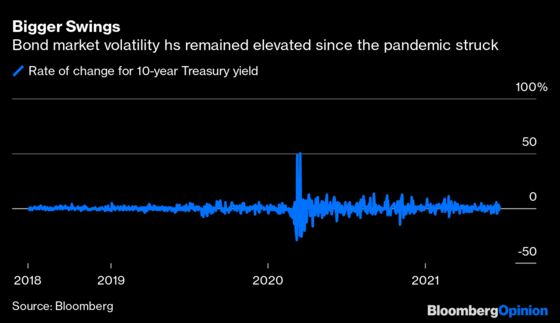

The onset of the pandemic last year produced a spike in volatility in bond and currency markets that provided a profit opportunity for nimble traders. Swings in the 10-year Treasury, the global benchmark for government debt, have remained elevated.

As market watchers debate the likely central bank response to rising consumer prices, those opportunities look likely to persist. Hedge fund traders, less constrained than their long-only counterparts in both the size and scope of the bets they can make, should be able to capitalize on conflicting views about whether inflation will prove transitory. With monetary policies poised to diverge among the biggest economic regions in the coming months, global macro has an opportunity to regain the swashbuckling status that made the names — and the fortunes — of some of the hedge fund industry’s most well-known players.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2021 Bloomberg L.P.