Breaking Up Amazon Won't Get the U.S. Its Next Tesla

(Bloomberg Opinion) -- Antitrust is again becoming a hot issue in the U.S., with a new bill advancing through Congress taking aim at top technology companies. There are the usual concerns about monopoly power, and also reason to worry about big-company dominance of key industries. Becoming over-reliant on just one or two national champions in each industry creates a lack of diversification, which puts the U.S. in danger of falling behind in key areas if those companies stumble. Government-forced breakups are one solution, but a wiser, longer-term approach is to encourage the formation of new superstars.

The U.S. has seen its national champions fall behind before. In the 1970s, General Motors Co. and Ford Motor Co. lost significant ground to Japanese competitors when they had difficulty managing the shift to reliable, fuel-efficient cars. International Business Machines Corp., which was utterly dominant in the technology industry as recently as the mid-1980s, is now a largely irrelevant also-ran.

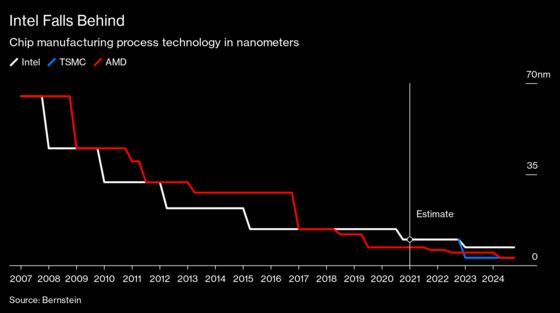

In some high-tech industries, U.S. giants persisted or even prospered. Boeing Co. retained its dominant position as part of a global duopoly in wide-body aircraft, while Intel Corp. was the king of the microprocessor. But in recent years, these, too, have begun to look shaky. After a period of uncertainty, it’s now clear that Intel has fallen behind Taiwan Semiconductor Manufacturing Co. in terms of the actual fabrication of computer chips:

Meanwhile, the company has never been able to do well in the mobile chip market. And in laptops, it's recently lost substantial ground to its old rival, Advanced Micro Devices Inc. There are many reasons for this, such as strategic decisions, management turmoil and technical difficulties. But the upshot is clear: The U.S. can no longer rely on Intel to dominate the strategically important semiconductor industry.

As for Boeing, its woes began with the grounding of the 737 Max in the wake of two deadly crashes. A defect in the flight control system was identified and corrected, but now the plane is facing a new set of manufacturing defects. With other factory problems weighing on the company, Boeing was hurt much more by the Covid pandemic than its main rival Airbus SE.

Sales are rebounding now that the pandemic is drawing to a close, but if the company has allowed the quality of its manufacturing to degrade, its future is cloudy. Meanwhile, competition from China in the wide-body aircraft space is about to arrive.

What should we conclude from this pattern? The wrong answer would be that U.S. companies are inherently weak. Other countries’ superstars, from the UK’s Rolls-Royce Holdings Plc to Japan’s Sony Group Corp. and many others, also tend to decline over time. Part of this might be simple statistics — if you stay around for long enough, eventually someone comes along and beats you. But it might also be due to what business guru Clayton M. Christensen called the “innovator’s dilemma” — the tendency of large, established companies to focus exclusively on their existing high-value customers and ignore new technologies that serve new markets. Intel’s failure in mobile chips certainly fits this pattern.

There’s one important difference between the U.S. and other countries when it comes to its flagship companies: the U.S. keeps minting new ones. Apple Inc., Amazon.com Inc., Microsoft Corp., Alphabet Inc.'s Google and other U.S. technology champions are all relative newcomers. The average age of companies in the S&P 500 stock index has gone from more than 60 years in the mid-20th century to less than 20 years today. Meanwhile, the most valuable car company in the world is now Tesla Inc., which was founded in 2003. This gives the U.S. an advantage over Europe and Japan, which create relatively few new giants — and it should eventually be an advantage over China, when that country’s companies age.

There’s an important lesson here. As the U.S. turns back toward industrial policy, there will be a natural urge to throw money at large stalwarts such as Boeing and Intel. As an example, a large component of the recently passed U.S. Innovation and Competition Act includes more than $50 billion to support semiconductor fabrication; it’s possible that Intel will end up pocketing a significant portion of that. Preferentially supporting nameplate companies is, unfortunately, a staple of U.S. industrial policy — the Export-Import Bank, which lends money to U.S. businesses that sell goods abroad, traditionally lends most of its money to major companies.

That’s a wrongheaded approach. Yes, sometimes rivals like China subsidize their own national champions and the U.S. has to follow suit in order to stay competitive. But a great many times, U.S. giants fail all on their own — by firing a top CEO, making the wrong bets or by letting quality control slip. Placing the country’s resources behind the largest players risks propping up companies that don’t deserve to be propped up.

It’s not clear how much antitrust action helps either. Smacking down the platform business models of Google or Amazon might increase competition domestically, but the effect on U.S. competitiveness vis-à-vis countries like China is unclear. And given the historical pattern of companies like IBM losing their dominance naturally, antitrust enforcement might simply be speeding up a natural process.

Thus, the U.S. has to focus more on creating new national champions to exist alongside the old ones. Industrial policy funding should be directed to young upstarts, in order to help them scale up quickly. Andy Grove, himself a former Intel CEO, recommended this approach. This funding should be available for a limited time — if a promising new enterprise fails to become the next Tesla, it's fine to let it settle for a smaller market position, or get scooped up by another up-and-comer.

But the key here is novelty. America has always been the country of novelty. To shift toward backing old dominant companies will be to retreat into a defensive crouch. Instead, move on to the next big thing.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2021 Bloomberg L.P.