Brazil's Oil Flop Is a Warning for Majors and Aramco

(Bloomberg Opinion) -- Royal Dutch Shell Plc made a big investment in offshore energy this week — wind energy, that is. The very next day, Brazil announced the results of a more traditional energy auction in the waters off its coast. They were not good.

The country’s biggest-ever sale of oil deposits flopped on Wednesday morning. Only two out of four blocks were sold, and only one of those involved foreign bidders, with China’s CNOOC Ltd. and China National Oil and Gas Exploration and Development Co. taking all of 10% of the Buzios field. Petroleo Brasileiro SA took the other 90% and all of the Itapu block. Western oil majors, such as Shell or Exxon Mobil Corp., were nowhere to be seen.

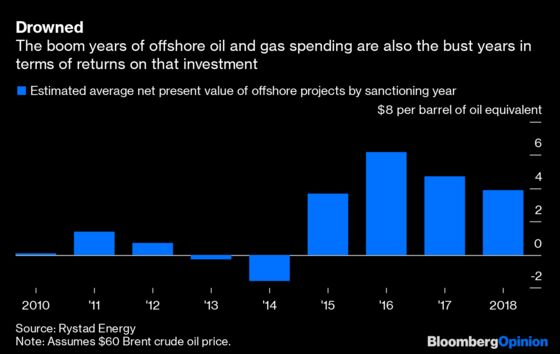

Offshore oil investment was all the rage among Big Oil during the supercycle, with capital expenditure almost quadrupling in the decade up to 2014. That is the problem. The majors poured money into large, multi-year projects prone to delays and, because of their often bespoke engineering, spiraling budgets. The result: tumbling return on capital and an inability to dial back investment quickly when the oil crash hit in 2014. Roughly 3,000 new offshore projects sanctioned between 2010 and 2014 have either barely generated any value for oil companies or are expected to generate none at all, according to a recent study published by Rystad Energy, a consultancy:

More recent investments score better, mostly because the boom tailed off, with offshore capex falling by more than half between 2014 and 2018. That took the heat out of industry inflation; and, because of the bonfire of returns in the prior decade, oil majors got smarter about such things as standardizing offshore equipment design to cut costs and shorten schedules. The pace of new projects has picked up again after the slump. Exxon, for example, has effectively opened up an entire new offshore zone with its Guyanese fields.

Still, one look at the stock prices of oilfield services firms, especially offshore-focused types such as Transocean Ltd. and Noble Corp. Plc, tells you this investment wave is nothing like the tsunami of yesteryear. Bad memories combined with unease about both near- and long-term oil demand make bold bets on big, multi-year offshore projects a tough sell with investors more interested in payouts. Even Exxon’s success in Guyana gets overshadowed by the fact that the company’s capex bill leaves it borrowing to pay its dividend. And Exxon, like Chevron Corp. and other majors, has swung more of its spending toward shorter-cycle onshore fracking in North America.

Brazil’s brush-off is an ominous sign the investment discipline demanded by energy investors is choking off one of the world’s biggest sources of oil-supply growth. In its latest World Oil Outlook published this week, OPEC cited Brazil as being second only to the U.S. in terms of medium-term growth, and number one in terms of projected long-term non-OPEC growth. Bob Brackett, an analyst at Sanford C. Bernstein, published a report a couple of weeks ago pondering if global offshore oil supply would peak next year, perhaps for good.

The implications are profound. There is a wide range of views on when global oil demand will slow or peak altogether. If it is later than sometime next decade, then the decline in offshore production that will inevitably follow a mass exodus from this part of the business could stoke another upcycle in prices. The Brazil auction suggests, however, that such possibilities play second fiddle to expectations on the part of many investors that oil has entered its twilight years.

Such results are ominous for offshore services providers, of course, and for the countries involved. Brazil’s currency slumped Wednesday morning as the market digested the lack of foreign capital targeting the country’s choicest oil resources.

Another country that should take note is Saudi Arabia. Like Brazil, it’s trying to tempt foreign buyers to pay up for a piece of its black gold. On the same morning, reports emerged that Saudi Arabian Oil Co. is seeking commitments from Chinese state-owned entities to invest in its IPO. Such strategic buyers do provide cash. But as Brazil could tell Aramco, turning to them also says a lot about the broader appetite for what you’re selling.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.