Boris Johnson's Biggest Battle Is the Plunging Pound

(Bloomberg Opinion) -- For much of the past two and a half years, the U.K. has had the luxury of negotiating the terms of its departure from the European Union under little pressure from the financial markets. The new prime minister Boris Johnson could soon come to pine for those calmer days.

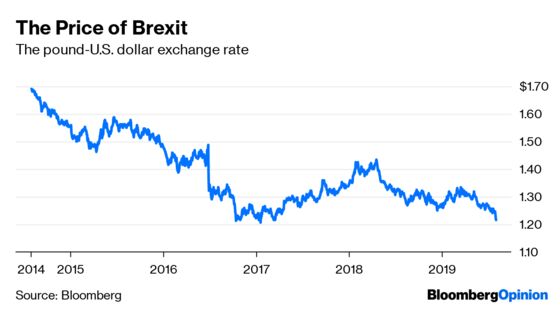

On Monday sterling fell by more than 1.3% to $1.22, hitting its lowest point against the dollar since March 2017. It resumed its slide on Tuesday and is heading for its worst slump in almost three years. Johnson has made it clear that Britain will quit the EU at the end of October even if this means leaving without a negotiated agreement. He has also stepped up preparations for a “no-deal Brexit” to try to convince Brussels that Britain is not bluffing about its willingness to accept such a fate. Investors are letting “BoJo” know what they think of his plan.

This isn’t the first time markets have moved violently because of Brexit. In the immediate aftermath of the 2016 referendum, the pound lost more than 10% against the dollar. Sterling slid again in the autumn of that year when the former prime minister, Theresa May, signaled that she wouldn’t wait long before starting the withdrawal process. But it stabilized subsequently when markets were reassured that her government and parliament were looking for an orderly withdrawal. In April of 2018, the pound briefly touched the dizzying heights of $1.434 (only 3.6% lower than before the referendum).

Investors are right to be running for cover again. A no-deal Brexit would be an unmitigated disaster for the U.K. as it would suddenly make it much harder to exchange goods and services with the EU, Britain’s main trading partner. The housing market would tumble, as would the price of other assets. The Bank of England could try to mitigate the shock by flooding the economy with money but it would need to be mindful of the impact of a steeply depreciating currency on inflation. In any case, this would do very little to address the damage to supply chains and business confidence. So dire are the consequences of a hard break that it doesn’t take much more than a whiff of it for the pound to tank.

The big question is how all of this will play into the negotiations between Johnson’s new team and Brussels. The prime minister hopes that his more muscular stance line will prompt the bloc to relax the terms of the withdrawal agreement negotiated with May, in particular the Irish backstop (a guarantee of no hard border between the Republic of Ireland and Northern Ireland). Johnson has been emboldened in his brinkmanship by the economic slowdown in the rest of the EU. The Brexiters believe that the fear of another shock (from a no-deal departure) will ultimately prove daunting enough to force Brussels to sweeten Britain’s terms of exit.

While it’s true that a no-deal Brexit would hurt the rest of the EU too, this is a pretty desperate gamble by Johnson. Should this week’s sterling storm continue, it will put the British negotiating team under enormous pressure. London risks facing its European counterparts in a condition that’s not entirely dissimilar to that of the Greek government as it sought to reopen the terms of its bailout in 2015, or the Italian government as it tried to push for a higher deficit target last autumn.

Of course, Britain is in a far stronger position economically than either Greece or Italy. But just like Athens and Rome, it’s much more exposed to an investors’ strike than the rest of the EU, only in this instance via its currency rather than its bonds. A plummeting pound is a constant reminder of what Britain has to lose from crashing out without a deal. As such, it’s difficult to see how Johnson’s aggressive negotiating stance can prevail.

Since he’s unlikely to obtain any meaningful concessions, Britain’s new prime minister would be wise to ask himself if a cataclysmic exit is really where he wants to go. In fairness, he’s been boxed in electorally by Nigel Farage’s Brexit Party, which promises a hard departure should Johnson’s Conservatives fail to deliver. But the foreign exchange markets can be an equally implacable foe.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ferdinando Giugliano writes columns on European economics for Bloomberg Opinion. He is also an economics columnist for La Repubblica and was a member of the editorial board of the Financial Times.

©2019 Bloomberg L.P.