Bond Yields Are Sending a Scary Signal on Stocks

The S&P 500 could go down 30% to 40% from here as the great depth and length of the recession hits home, writes Gary Shilling.

(Bloomberg Opinion) -- There is no shortage of investors shrugging off the latest leg lower in U.S. Treasury bond yields, saying heavy central bank involvement in this part of the financial market make such moves less of a signal that the economy or that equities are headed for trouble. That interpretation would be a mistake.

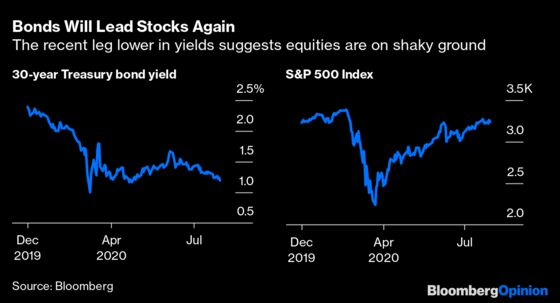

Recall that yields on 30-year government bonds started to decline on Jan. 2, anticipating the fallout from the budding coronavirus crisis that had taken hold in China. Yields fell from 2.34% on that day to 0.94% on March 9, as the price of the benchmark 30-year bond leaped 29%. Only on Feb. 19—seven weeks later—did the S&P 500 Index begin its 35% slide. Fast forward and 30-year yields have fallen from 1.66% on June 8 to a recent 1.19% as their prices climbed 9%. The question is whether stocks will follow again, and with a similar lag of about seven weeks.

The fundamental economic scene favors a repeat. The situation is ghastly, with Covid-19 infections accelerating and plans for physical classes at many schools, colleges and universities this fall risking further contagion. Staying closed or holding virtual classes, however, promotes dropouts, pressure to cut tuition and fees and financial disaster for many schools. Then there are the problems of reopening businesses, re-establishing and reorienting supply chains and encouraging many to return to work who are now paid more by federal and state unemployment benefits than when they were employed.

The recent Treasury bond rally fits with our forecast that the recession has a second, more serious leg that will extend well into 2021, despite massive monetary and fiscal stimulus. Declining business activity saps private credit demand and makes Treasuries shine as havens. A deep recession also breeds deflation to the benefit of Treasuries. The government said Thursday that its core personal consumption expenditure index, which is what the Federal Reserve uses to track inflation, fell 1.1% in the second quarter.

Over the entire post-World War II era, the correlation between Treasury bond yields and inflation as measured by the Consumer Price Index is 60%. This is remarkably strong considering all the other possible influences on long-term interest rates such as federal budget deficits, wars, consumer sentiment and spending, and government actions. My forecast of Treasury bond yields starts and ends with my projection of inflation.

The spread between 10-year Treasury Inflation-Protected Security yields and conventional 10-year Treasury yields, which is what bond traders expect inflation to average over the life of the securities, recently dropped to a miniscule 0.50% from 2.5% in 2012.

Treasury bond investors concentrate on inflation, Fed policy and not much else. In contrast, equity mavens worry about a whole host of often conflicting issues such as corporate finances, profits, price-to-earnings ratios, to name just a few.

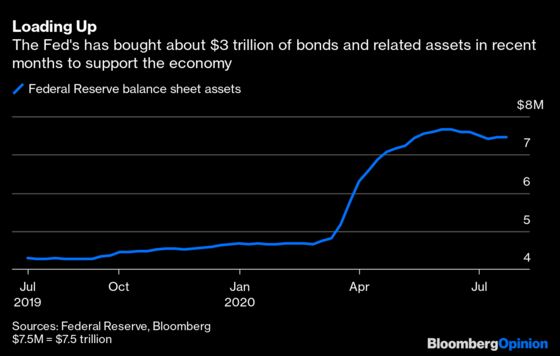

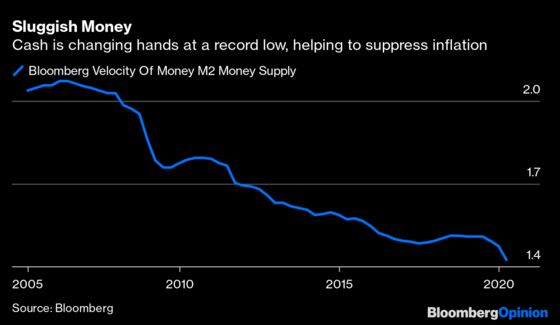

Sure, the Fed has been buying Treasuries and along with other fixed-income securities, so its assets have exploded to $7 trillion from around $4 trillion in February. Nevertheless, all this Fed-created liquidity hasn’t found its way into the real economy, as shown by the collapse in the velocity of money.

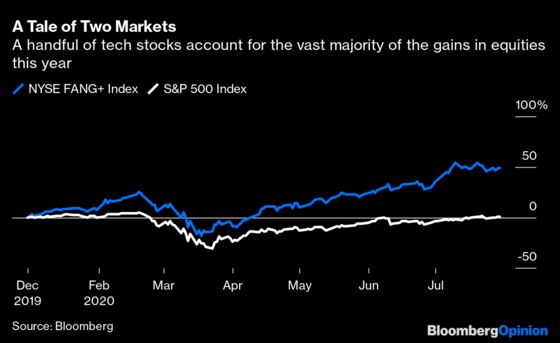

Then there is the argument that, except for a handful of technology shares such as Facebook Inc., Amazon.com Inc., Apple Inc., Microsoft Corp. and Google-parent company Alphabet Inc., the stock market continues to be weak. Goldman Sachs Group Inc. notes that these five have added more than a third to their market values this year, despite the sharpest recession since the Great Depression.

The S&P 500 is up 0.5% for the year thanks to the strength of those five companies, but the other 495 members are down about 5% on average on a market cap-weighted basis. Still, that 5% decline pales in comparison to the earlier 35% plunge in the S&P 500. Goldman Sachs calculates that if those five tech stocks were to fall 10%, the bottom 100 in the S&P 500 would need to jump 90% to offset the decline.

Tech stocks have benefited from their relative independence from the nuts-and-bolts economy. Also, they’ve gotten a boost from homebound Americans who have replaced face-to-face contact with telecommunications. But they are very expensive and under fire from Washington and Europe for anti-competitive practices. And fads end. Recall the craze for Socks the Puppet and his dot-com buddies in the late 1990s. When that bubble broke, the Nasdaq Composite Index plunged 78%.

Also recall the so-called Nifty Fifty group of stocks in the early 1970s. When the only companies of interest to investors made gimmick cameras, ran amusement parks and built motor homes, it was clear the basic economy was in trouble. What followed was the severe 1973-1975 recession and deep bear market.

I believe the bond rally signals a renewed drop in stocks, with the S&P 500 down 30% to 40% from here as the great depth and length of the recession hits home.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

A. Gary Shilling is president of A. Gary Shilling & Co., a New Jersey consultancy, and author of “The Age of Deleveraging: Investment Strategies for a Decade of Slow Growth and Deflation.” Some portfolios he manages invest in currencies and commodities.

©2020 Bloomberg L.P.