Bond Traders’ Hot Tip for Next Year? Buy Stocks.

(Bloomberg Opinion) -- There’s always been something of a rivalry between traders in stocks and bonds. Equities grab most of the headlines — they are shorthand for “the market,” after all — and captivate individual investors. Fixed income, on the other hand, is for pessimists and hedgers and is often praised as the “smarter” asset class.

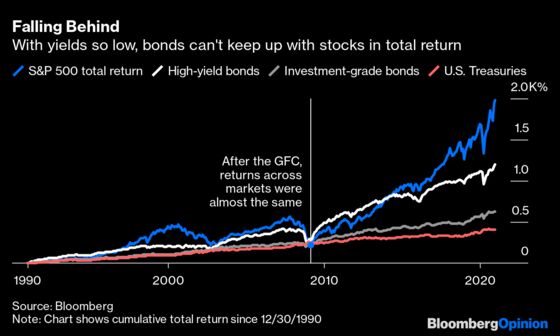

No one truly disputes the notion that stocks tend to deliver superior returns to bonds over a long period. But during the past three decades, it’s been a relatively tight race. The Dow Jones Industrial Average has gained an average of 11.1% a year since 1990. The S&P 500 has earned 10.7%. High-yield bonds have returned 8.9%, investment-grade corporate debt has gained 6.9%, and even U.S. Treasuries have delivered 5.5% on an annual equivalent basis, according to Bloomberg Barclays index data. During this stretch, with a handful of smart decisions, a fixed-income fund manager could at least hope to match the overall performance of U.S. equities, if not beat the indexes altogether.

Heading into 2021, however, bond investors are just about ready to throw in the towel.

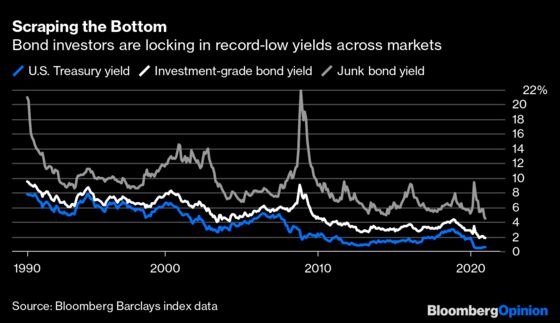

A quick glance at prevailing yield levels tells the story. Benchmark 10-year Treasuries are still below 1%. Top-rated 10-year municipal debt yields even less: 0.67%. The average investment-grade corporate bond, with a 12-year maturity and a rating six or seven steps below triple-A, yields 1.82%, just two basis points away from its record low. The average U.S. junk bond yields 4.49%, also within range of an all-time low.

Yields, of course, are an expression of the total return an investor can expect from holding a bond to maturity, provided it doesn’t default. While fixed-income assets of all stripes have had the wind at their backs for the past three decades as Treasury rates declined, which boosts bond prices, the “income” part of the equation has been what has reliably driven returns over the long run. That’s especially true for patient investors who could step in during periods of turmoil — buying the right high-yield bond in late 2011 or early 2016 could lock in a 10% return for years.

After an unprecedented year in which the Federal Reserve expanded its balance sheet by more than $3 trillion and waded into the corporate-debt and municipal-bond markets like never before, however, bond traders are left to wonder whether such patience will be rewarded ever again. Betting on a sharp increase in yields looks like a fool’s errand, even if U.S. growth rebounds next year, given the central bank’s ability to bend the Treasury market to its will. Meanwhile, the S&P 500 is up 16.9% in 2020, and a stunning 67.3% since March 23, when the central bank unveiled its corporate credit facilities.

“Let’s be honest: We try to generate cash plus 2% to 3% in our fixed-income portfolios. You can get that in equities in two to three days,” said Nick Maroutsos, head of global bonds at Janus Henderson Investors. “Why own lower-rated debt, why own illiquids, bank loans, when you can just buy equities and you’re probably going to be better off?”

Maroutsos runs the $2.9 billion Janus Short Duration Income ETF, which is up about 3% this year. That may seem meager in absolute terms, but it has one-tenth of the volatility of the SPDR S&P 500 ETF Trust, as measured by standard deviation, giving it a better overall Sharpe ratio, which measures return per unit of risk.

“What we’re telling our investors is that central banks aren’t going to be raising interest rates, so there’s not going to be a lot of volatility in the front end,” Maroutsos said. “You’re not going to make a ton of return, but you’ll get some income that won’t be subject to a lot of volatility. You set yourself up for an OK return for the next 12 months, and if you want to be more aggressive, you do it in the equity space.”

Rick Rieder, BlackRock Inc.’s chief investment officer of global fixed income and head of the global allocation team, sees individual investors who allocate 60% to stocks and 40% to bonds coming to the same conclusion. “For a traditional 60-40, if a lot of the 40 is getting you zero to negative return, holding more cash and moving more to equities or private, less-liquid alternatives, that’s going to keep going,” he said in an interview. “The yields we’re financing companies at today is not a normalized condition. Part of why I think equities will continue to run higher is it’s allowing companies to spend on capex, M&A, R&D — it’s just a direct injection of enterprise value for these companies with where they can borrow.”

If that weren’t enough, none other than Fed Chair Jerome Powell appeared to make the case that stocks aren’t as inflated as they seem by employing the so-called Fed model, which looks at the S&P 500’s earnings yield relative to bonds. He also made it clear that investors shouldn’t expect meaningfully higher long-term interest rates anytime soon. “Admittedly P/Es are high, but that’s maybe not as relevant in a world where we think the 10-year Treasury is going to be lower than it’s been historically from a return perspective,” he said during his Dec. 16 press conference.

He might as well have said TINA (there is no alternative). “As much as the Fed says they don’t focus on the stock market, we know that they do,” and the comment on equity valuations proved it, said Patrick Leary, senior trader and chief market strategist at Incapital.

At some point, once the cloud hanging over the U.S. economy from the pandemic is lifted, the Fed will most likely pay closer attention to financial conditions, which are as easy as they’ve ever been. “By lowering the discounting rate for every asset class, you’ve inflated the terminal value of those asset classes,” Bob Michele, global head of fixed income at J.P. Morgan Asset Management, told me. “That’s something that longer term is not sustainable, and you need a response.”

That doesn’t help bond investors heading into 2021, however. A slow and steady increase in 10-year Treasury yields from 0.9% to 1.25% — as predicted by Goldman Sachs Group Inc. — would mean a loss of about 1.6%. For General Electric Co. debt that matures in 2035, the largest component of the Bloomberg Barclays triple-B corporate bond index, it would only take a 30-basis-point move higher in yields by this time next year to produce a negative return. If yields are unchanged, it would return 2.9%. But to Maroutsos’s point, that compares with the 13.3% gain for the S&P 500 since the end of October.

Stocks don’t “always go up” and certainly shouldn’t be seen as providing risk-free returns. But, as some market observers like hedge-fund billionaire Leon Cooperman have taken to saying, bonds at these yields offer something closer to “return-free risk.” When faced with those two options, it’s hardly surprising that investors are leaning toward riding the equity rally into the New Year. Even the “smart money” in fixed income.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.