(Bloomberg Opinion) -- Consumer prices paid by city dwellers in the U.S. rose more than 7% last month and more than 9% in April on an annualized basis. If this keeps up the rest of the year, it will be the highest inflation rate the U.S. has experienced since the 1980s. But fear not, say some investors and the Federal Reserve, the bond market isn’t worried. Yields fell over the last week and remain low by historical levels, even after rising on the back of Jay Powell's speech Wednesday. And if markets aren’t worried, maybe we shouldn’t be either.

But there are reasons to worry about rising prices, and the bond market shouldn’t offer any comfort.

In theory, bonds are a barometer of future inflation. If inflation is high for the next 10 years, that would lower the return on a 10-year note. So investors want to be compensated for what they think inflation will be or for the risk involved when the outlook is uncertain. If either expectations or inflation risk increase, so should bond yields, but the opposite has happened in the last few weeks . That means one of two things: Inflation will moderate, or bond prices aren’t accurately reflecting inflation risks.

Historically, bond yields have not been very good at predicting inflation.

In the last 70 years, bond yields rarely rose ahead of inflation, going up only after inflation takes hold. One study indicated that past inflation trends were a better predictor of bond rates than what future inflation turned out to be.

Does this mean bond traders are wrong? Not necessarily. It may just reflect that inflation is unpredictable and bond traders don’t know any more about the future than the rest of us. All they have is the past data and current prices to make their predictions, too. So when inflation suddenly spikes — as it has in the past — bond traders are as surprised as everyone else.

Bond markets are even less predictive now.

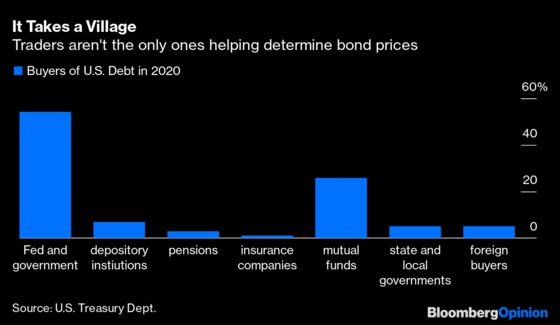

Even if bond traders did have a magic ability to predict the future, they don’t entirely determine bond prices. In the first quarter of 2021, the Fed’s expanding balance sheet accounted for more than 70% of the growth in outstanding government debt. Many financial institutions also buy lots of bonds; depository institutions and insurance companies accounted for about 8% of new Treasury bonds purchased last year, in part because government bonds are considered low-risk assets and must be held for regulatory reasons.

In 2020, the Fed, the government, banks and insurance companies accounted for more than 64% of new government debt. Pension funds also buy bonds, no matter their inflation outlook, to hedge their liabilities. Not only that, fewer bonds were issued in the first quarter of 2021 compared with the last quarter of 2020. In short, U.S. treasuries have a large captive market because of government policy — and then supply was cut. This alone could lower bond yields and swamp whatever inflation fears bond speculators have.

Meanwhile, falling yields should be a source of concern. The current pickup in inflation may indeed be temporary, related to the inevitable hiccups from turning back on a dormant economy that has thrown supply and demand out of alignment. But it's possible that the effects will be long-lasting and that inflation has returned after nearly 40 years in retreat. Even temporary inflation can become permanent if it changes long-term expectations. Or perhaps the world is entering an era of less trade, which will mean higher-priced goods.

And the fact the government is such a large buyer of bonds is a source of risk. Policy could change. The Fed may decide to clamp down on inflation if it takes hold. And if so, it will stop buying bonds and start selling them instead. This not only risks cutting short an economic recovery, it also risks causing huge dislocations in the bond market when it loses a massive buyer of debt.

The U.S. government has historically relied on selling the world’s risk-free asset, which has meant no matter what it did (even monetizing debt), yields fell as foreign buyers kept purchasing U.S. bonds. In the last few years, their appetite has waned, though they remain a source of vulnerability, too. Even while purchasing fewer bonds now, foreign buyers still hold about 25% of outstanding debt. If they get nervous, they could sell, too, and add more turmoil to the bond market.

No one can predict the future, even bond buyers. All we have is data from the past and current market prices to make sense of things. Both of these suggest interest rates and yields will stay low. But there are some significant sources of risk ahead and reasons to think this time could be different. Current data should not convince investors to let their guard down.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Allison Schrager is a Bloomberg Opinion columnist. She is a senior fellow at the Manhattan Institute and author of "An Economist Walks Into a Brothel: And Other Unexpected Places to Understand Risk."

©2021 Bloomberg L.P.