Blackstone Bid Reminds Us Why Pipelines Are Unloved

(Bloomberg Opinion) -- One could almost feel sorry for that decidedly unloved crowd known as pipeline operators. Except they keep finding ways to make it really hard.

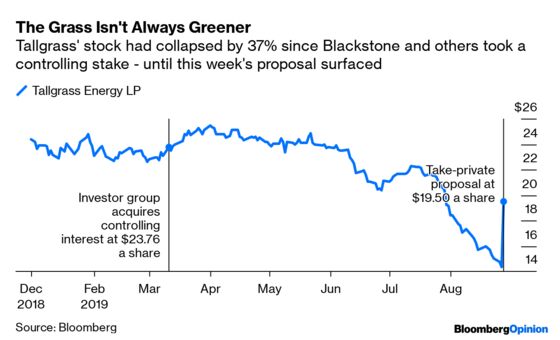

Tallgrass Energy LP has received a buyout offer from an investor group led by Blackstone Group Inc. This follows a deal in March in which the group took a controlling stake in Tallgrass. Things haven’t gone well since then.

The biggest thing weighing on the stock is fear that Tallgrass will have to drop prices in upcoming contract negotiations for two of its major pipelines amid rising competition. That and the fact that energy stocks are just pariahs in general. Plus, while Blackstone and others made a big bet on Tallgrass earlier this year and looked likely to eventually bid for the whole thing, they aren’t exactly known for being a soft touch when it comes to pricing.

The new offer is a 36% premium to where Tallgrass was trading, although that isn’t saying much given how far it had sunk. It effectively makes up just one month’s worth of lost ground.

What may really crush the already despondent souls holding the other 56% of Tallgrass, however, is the knowledge that several of the company’s executives hold something akin to a get-out-of-jail-free card.

I saw a reference on Twitter under an anonymous handle called @mr_skilling (it’s a parody, folks … I think) to “Management Side Letters” in a filing made by Tallgrass with the Securities and Exchange Commission in March. Among other things, these letters contain a provision that if the investor group took Tallgrass private within a one-year lockup period, then those executives – including the CEO, CFO and COO – could sell their stakes for a minimum price of $26.25 per share, a 35% premium to this week’s buyout proposal.

Tallgrass notes the letters were already disclosed and reflect a “general-partner control premium” as part of the deal in March. The company also characterizes the agreements as “facilitating management’s retention of equity interests,” and thereby “ensure continued alignment between management and [Tallgrass’s] equity holders.”

That last bit may prompt some narrowing of the eyes by equity holders faced with the prospect of getting paid substantially less than the executives with whom they are supposedly aligned. And while the letters were referenced in a filing that’s been out there for several months, it’s possible they could have done with a bit more airing. Stephen Ellis, an analyst at Morningstar Inc., certainly seemed taken aback, calling the letters “awful corporate governance” in a note published after the new proposal was announced. Ellis hopes the company’s conflicts committee will either reject the proposal outright or push for a higher offer (Tallgrass emphasized this independent committee would review the offer).

However this turns out, it is a reminder of the governance minefield that can greet the investor who strays into energy land. While exploration and production has its fair share of egregious examples, the pipelines business has long punched above its weight when it comes to misaligned incentives and investor-unfriendly outcomes (see this and this for two real doozies). One of the ironies of Blackstone’s offer is that it sparked speculation this week about private equity jumping on bargains in a sector that generalist investors have deserted – while simultaneously reminding us why they left in the first place.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.