(Bloomberg Opinion) -- In what’s billed by local media as the “divorce of the century,” the chairman of South Korea’s third-largest conglomerate could wind up surrendering up to $1.2 billion of his shares to his aggrieved wife. Chey Tae-won has good reason to worry that judges won’t look kindly upon him: He’s already started a second family with a glamorous American-Korean internet sensation, not to mention his wife is the daughter of former President Roh Tae-woo. But it looks like this Hollywood-caliber split could have more repercussions in the boardroom than the bedroom.

South Korea started restructuring its sprawling family-run conglomerates, or chaebol, as early as 2012. The program gained steam five years later, when it became a centerpiece of the campaign that swept President Moon Jae-in to power. Moon quickly installed a “chaebol sniper” to help unravel these overly complex corporations.

With the economy now in the doghouse, there’s a growing sense that Moon’s agenda is flagging. Chaebol are trading at a 44.8% discount to their net asset value, according to CLSA Ltd., the steepest since 2011. Last September, Kim Sang-jo, the chaebol sniper, left the helm of Korea’s antitrust watchdog. Investors have grown impatient.

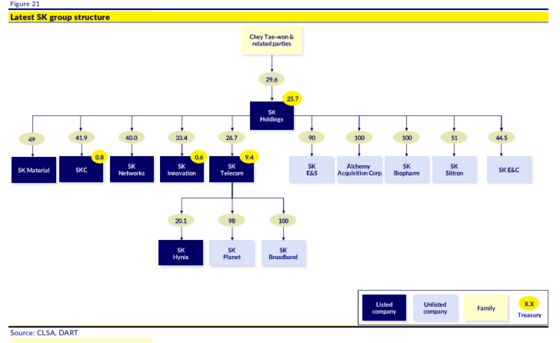

If there’s any silver lining to Chey’s divorce, it’s that his wife, Roh Soh-yeong, might be able to deliver what Moon hasn’t. In a court filing early last month, she demanded 42.3% of Chey’s stake in SK Holdings Co., which would amount to 7.8% of the company. Such a transfer of ownership would push her husband’s voting rights below 20%, a golden threshold of control in Korea. Currently, Chey and his clan hold 26.7% of the company.

To minority shareholders, a family feud would be music to their ears. The conglomerate’s holding companies are severely undervalued, so the arrival of Roh to the board may revive restructuring plans that had largely gone quiet. And even if she does nothing, Chey may want to boost his stake, just to ensure control. Such demand could lift stock prices and end up rewarding outside shareholders.

Roh has a good shot of getting what she wants. SK was founded in 1953 by Chey’s father as a textile company, but the business took off after the pair got married in 1988, the year Roh’s father was inaugurated. As part of the government’s privatization drive, the group became the largest shareholder of state-owned Korea Mobile Telecommunications Corp., which eventually became SK Telecom Co. in 1994, a year after the former president left the office. Roh’s political connections quite possibly bolstered SK’s success, a savvy divorce judge may be inclined to reason.

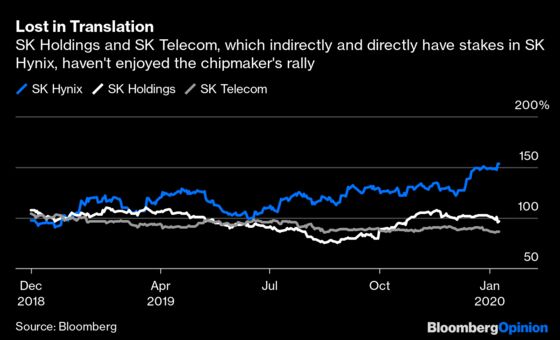

While SK’s telecom unit is no longer growing at the neck-breaking speed of the late 1990s, it holds the key that keeps Chey’s grip over his empire’s crown jewel — SK Hynix Inc. SK Holdings has a 26.7% stake in SK Telecom, which in turn owns 20.1% of the memory-chip maker, whose shares rallied 65% over the last year.

Beyond the upside of a boardroom drama, there are few reasons to hold stock of SK Holdings or SK Telecom, particularly if exposure to the chipmaker is all investors want. Shareholders of SK Holdings have to suffer a conglomerate discount, twice, just for exposure to the crown jewel, which they can just as easily get by holding the stock directly. While investors enthusiastically chased after SK Hynix, betting on a cyclical upturn of memory chips this year, they have stayed away from the other two. Meanwhile, a price war in Korea for new 5G subscribers isn’t necessarily a good thing for operators like SK Telecom.

The Chey-Roh drama isn’t the only ugly family feud that could be rewarding to outsiders. In December, shareholders enjoyed a surge in Hanjin Kal Corp. — another conglomerate whose units include flagship carrier Korea Air Lines Co. — after the founding patriarch's eldest daughter criticized her brother, who is now in charge of the family business. Heather Cho first gained global notoriety for the “nut rage” incident in 2014.

In any other part of the world, investors would breathe a sigh of relief at signs of an amicable breakup – think Jeff and MacKenzie Bezos, for one. But in Korea, a messy split might just be the best outcome: The nastier these squabbles get, the better the chances executives will pony up and buy more voting rights. Company outsiders may never get much of a voice, but at least their shares will be more valuable.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2020 Bloomberg L.P.