Big Job Gains Are Coming, But Not Yet and Not Enough

(Bloomberg Opinion) -- The economic disruption caused by the coronavirus has led to huge questions about what the employment situation in the U.S. will look like in a few months, let alone in the next year or so. Forecasts of annualized real gross domestic product growth in the second quarter of -40% and an unemployment rate peak of 25% are well within reason. If there's a bright spot for workers, it's that the historic relationship between real GDP and employment suggest that, millions of workers will need to be hired back fairly soon just to keep the economy running at its current low level. Short-term pandemic disruptions are unpredictable, but we should expect a return to the historic relationship between output and employment before too long.

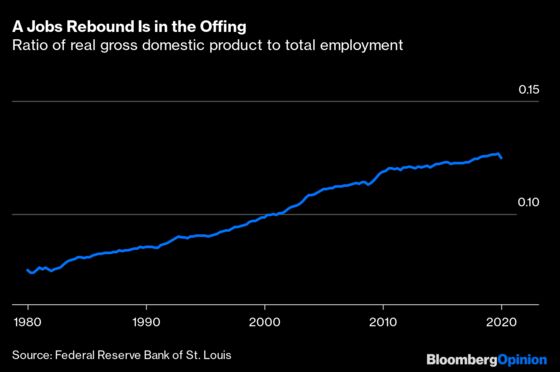

We can see how tight the relationship is between real, or inflation-adjusted, GDP and employment by looking at a long-term chart. Over the decades we've had big and small booms and busts, but dividing real GDP by employment shows a relatively stable relationship. The gentle rise accounts for productivity growth, as the economy becomes more efficient. There's nothing magical here; real GDP can be thought of as a function of hours worked and productivity. But it's useful to keep in mind when we're experiencing historic levels of economic disruption.

As we await another jobs report that probably will show millions of jobs lost in May, this framework can help us think about how many jobs that have been lost over the past few months will be added back. Through April, total employment had already declined by 21 million since the end of 2019, the starting point we'll use to be consistent with the real GDP data. Estimates for May are a loss of another 8 million jobs. That would be a total decline in employment of 29 million, or 19.1%.

That decline would be disproportionate relative to the decline in real GDP. Normally, when we talk about GDP growth we use annualized numbers, but since these declines have been so big it's more useful to look at the raw decline. On Friday, in part due to slight improvements in real-time economic data as state economies reopen, Goldman Sachs "raised" its estimate for second-quarter real GDP growth to -36% annualized, or 9% for the year. That would follow the first-quarter decline of 5% annualized, or 1.3% overall. Combine these figure and the U.S. will have a suffered a cumulative real GDP decline of 10.2% since the end of 2019.

A 19.1% decline in employment is inconsistent with a 10.2% decline in real GDP. Assuming there's any kind of economic recovery from here, companies will run out of things to sell or find themselves understaffed at even these lower levels of demand. We don't need a coronavirus vaccine to close some of the gap between the decline in employment and real GDP.

To think about what kind of partial employment recovery we should expect, we need to know how much economic output will recover in the short-term. Various real-time indicators have shown economic activity increasing since about the second week of April, and those can give us at least a little bit of an idea for what to expect. Housing has recovered robustly, with mortgage-purchase applications now back to pre-coronavirus levels and up from a year earlier. Mobility data from Apple Maps shows a steady increase in Americans on the move. Applications to form new businesses have largely recovered, a sign that would-be entrepreneurs have confidence in the future.

Harder-hit industries such as lodging and air travel still have a long way to go, but even they are showing steady improvement. Hotel occupancy has recovered about 30% of its peak-to-trough decline and passenger data from the Transportation Security Administration shows that air traffic, which at its April lows was about 4% of last year's levels, is now up to about 13% year-earlier levels. Both hotel occupancy and TSA data have shown gains every single week since early April. Those trends should continue for at least a little while as Las Vegas casinos, Disney theme parks and New York City slowly reopen in coming weeks.

What sort of near-term employment recovery is possible? Recovering 30% of lost output by the end of the third quarter would mean real GDP would still be 7% below its end-of-2019 level. That would still be much more severe than the 4% peak-to-trough decline of the Great Recession. And if the real GDP-to-employment relationship recovers to its late-2019 level, that would lift overall employment to 141 million -- meaning 10 million more jobs than in April. A less-efficient economy with more safety protocols and lower utilization of factories and facilities could even require more workers to produce the same amount of output for a while.

Returning to full employment will require a full economic recovery. But keep in mind that even in this subdued environment, the level of employment is unsustainably low. That means a significant, though still insufficient, rebound in employment should come during the next several months. It can't happen soon enough.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Conor Sen is a Bloomberg Opinion columnist. He is a portfolio manager for New River Investments in Atlanta and has been a contributor to the Atlantic and Business Insider.

©2020 Bloomberg L.P.