(Bloomberg Opinion) -- President Joe Biden shouldn’t expect an invitation to Saudi Arabia to place his hands on a glowing orb anytime soon.

Tuesday’s announcement that the U.S. will release 50 million barrels from the Strategic Petroleum Reserve, as part of a wider draw coordinated with other countries, is a direct rebuke to OPEC+, the group that Saudi Arabia leads alongside Russia. It also implies a potentially important shift in the role of strategic reserves in the oil market.

Rising energy prices hurt presidents at the best of times, but because of higher inflation Biden looks especially vulnerable. This not only hurts consumers but also provides Senator Joe Manchin a ready excuse to delay or derail the president’s green-tinged spending package.

So Biden wants to show that he hears the collective wailing from America’s gas stations. Initial reports suggest the total draw, including from other countries, could be almost 80 million barrels. Sold across December and January, this would provide roughly 1.3 million extra barrels a day. The Energy Information Administration’s most recent projections showed a deficit in the global oil market of about 1.5 million barrels a day in December and a surplus of 1.3 million a day in January.

Already, all the jawboning about the SPR seems to have helped cool prices (although Europe’s renewed Covid-19 lockdowns also loom large). Indeed, oil rallied Tuesday morning, presumably reflecting the earlier rumors having been digested. Still, this confirmed release upends the equation on supply and demand for the immediate future and, crucially, it derailed the rally that had gathered steam through September and October.

That is probably all Biden cares about, given that the oil market is expected to loosen in 2022. Even so, OPEC+ is threatening to offset the release by scaling back its planned production increases. It would appear to hold all the cards: The group produced almost 43 million barrels a day in October — of which almost 37 million is subject to production targets.

But it doesn’t. OPEC+ continues to underproduce even against its own modest target increases. In October, the core OPEC group delivered only half of its planned extra supply. That partly reflects the weakness of some members, such as Angola and Nigeria. It also reinforces its image as a tone-deaf club that touts its flexibility and “regulator”-like role even as it holds back supply from more capable members despite high oil prices.

Citigroup analysts estimate that the average monthly OPEC+ increase from August to November amounts to just 262,000 barrels a day, or 7-8 million barrels a month. As Ed Morse, Citigroup’s global head of commodity research, observes, from the perspective of the consuming countries releasing tens of millions of barrels, “why would I be worried about the risk to 7 million barrels?”

In addition, curbing production now would amount to giving up market share, a concept that has caused friction between Saudi Arabia and fellow heavyweights Russia and the United Arab Emirates in the past couple of years.

Strategic stocks are, of course, more finite than petro-state oil reserves. So even if the U.S. and others manage to cool prices, the effect would be short-lived. The stocks would need to be replenished at some point, creating more oil demand — and upward price pressure — down the road. Indeed, most of the U.S. release consists of short-term exchanges that will be replaced.

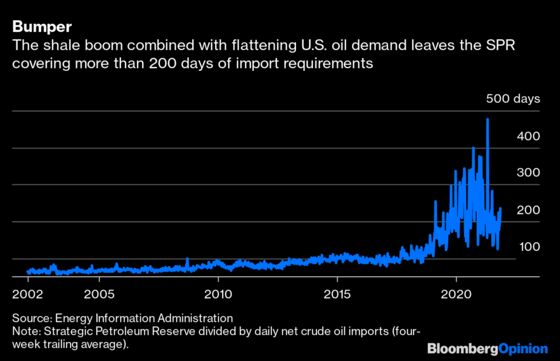

Yet the U.S. has room to be more aggressive if it wishes. It has flirted off and on with being a net exporter of oil since late 2019, including so far this month. It remains a large importer of crude oil (net exports are weighted to refined products), but even crude net imports average only around 2-4 million barrels a day. On that basis, the SPR currently covers more than six months worth of net imports, far more than needed.

Japan, one of the other countries releasing barrels, also holds more than 200 days worth of imports, although that also includes commercial inventories.

China is involved, too, which represents something of a diplomatic coup for Biden given the country’s importance as a customer for OPEC+ and its tense relations with the U.S. on nearly all other fronts. China, capitalizing on that importance, has spent the past decade or so building both strategic and commercial reserves, and it adjusts them to either take advantage of low oil prices or try to tame rallies.

Biden’s move, explicitly targeting oil prices rather than a specific emergency, hews more to Beijing’s trading model. Historically, the U.S. SPR has been “dead oil,” removed from the market and unlikely to be used except in the most extreme circumstances. If this release heralds a more interventionist approach, that would represent a important change in the oil market — and a signal that the old preoccupation with scarcity, rooted in the 1970s supply shocks, is slipping away.

For American oil producers, the release shouldn’t matter much; the longer-dated futures used for hedging purposes are less likely to be affected. Surveying 43 large exploration and production companies, Bernstein Research’s Bob Brackett calculates that, with oil averaging $71 in the third quarter, they generated almost $23 of cash flow per barrel-equivalent, of which only a third went on capital expenditure. The oil price isn’t what’s holding back shale production. It’s the deficit of trust with investors.

Biden’s move will probably have only a temporary effect of stalling momentum in oil prices. But in political terms, he is focused on the short term. The threat from OPEC+ is undermined by its own insouciance these past few months. Retaliation would only play into Biden’s hands. After all, as much as Americans blame pump prices on the sitting president, they’re no fans of OPEC either.

Bloomberg News reports five million barrels from India, "several days' worth of volume" from Japan (I assume 10 million), "at least" 7.3 million from China, "an unspecified volume" from South Korea (I assume 5 million), and 1.5 million from the U.K. Altogether, that would imply around 79 million barrels.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2021 Bloomberg L.P.