(Bloomberg Opinion) -- Federal Reserve Chairman Jerome Powell has done an excellent job managing the U.S. economy through both the vagaries of the Trump administration and the ongoing coronavirus pandemic. Yet the Fed under his leadership has fallen short in one crucial area: ensuring the long-term health and resilience of the country’s financial system.

President Joe Biden has an opportunity to remedy this shortcoming. He should use it.

Given how well the financial system appears to have weathered the pandemic, one could be forgiven for concluding that all is in order. It’s not. Banks avoided debilitating losses in large part because the Fed and the Treasury pledged trillions of dollars to stabilize markets and help borrowers make good on loans. This was the right response, but it also obscured some persistent fragilities.

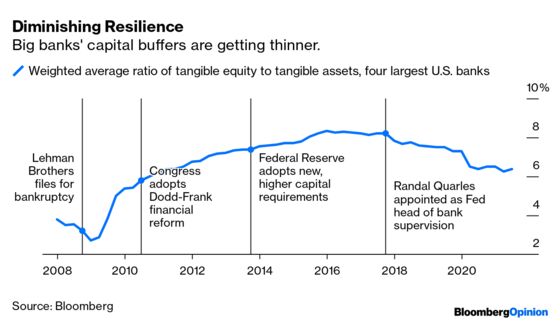

Consider one crucial indicator of financial strength: equity capital. Unlike forms of debt such as deposits, capital represents funds from investors willing to share the risk of losses. When banks have plenty, they’re better able to function in crises and contribute to the Fed’s recession-fighting efforts. But achieving this requires perseverance: Bank executives typically prefer to employ more debt, or leverage, which enjoys government subsidies and boosts certain measures of profitability in good times.

Authorities successfully pushed for more capital in the aftermath of the 2008 financial crisis, but never went far enough. At the four largest U.S. banks, tangible equity peaked at about 8% of tangible assets in late 2015 — much less than what research from the Minneapolis Fed and others suggests would be needed to make the risk of failure acceptably low. Since then, capital levels have waned along with political will: As of June 2021, that tangible equity ratio stood at around 6.4%.

The Fed has played a leading role in the unraveling. Randal Quarles, the Trump-appointed vice chairman for bank supervision, asserted in 2019 that “the capital-building phase of the post-crisis era is now complete,” citing as evidence banks’ ability to withstand hypothetical recessions and market meltdowns in annual stress tests. Yet those tests failed to capture the severity of a real crisis — and under Quarles the Fed made them even less stressful, allowing banks to return large amounts of capital to shareholders in the form of dividends and stock buybacks.

Under the rubric of achieving greater simplicity, the Fed also weakened supervision in other ways. It turned an initially sensible reform into a gutting of the Volcker Rule, intended to curb speculation at financial institutions that benefit from government backstops. It all but ended the formerly annual “living wills,” aimed at streamlining corporate structures by challenging banks to explain how, if they were failing, authorities could dismantle them quickly with minimal collateral damage. Now, for the largest institutions, the full plans are required only once every four years. Imagine trying to wind down Lehman Brothers in 2008 using instructions drafted in 2004.

The Fed is right about one thing: Supervision can and should be simpler. The way to achieve this, though, is by first insisting that banks build up sufficient equity to absorb the losses that actual crises have historically generated and still have some to spare. If banks were stronger, burdensome practices such as regular stress tests and micromanagement by examiners would be unnecessary. And if regulators placed tighter, effective limits on the activities that taxpayers support, hundreds more pages of rules could be eliminated.

This is where Biden comes in. The Fed needs a head of bank supervision who’s willing and able to pursue the dual goals of strength and simplicity. Quarles’s four-year term ends in October. With the right appointment, the president can send Powell an unmistakable signal — and set a much more promising course for financial reform.

Editorials are written by the Bloomberg Opinion editorial board.

©2021 Bloomberg L.P.