Biden Boosts the Euro, But the Dollar’s Still King

(Bloomberg Opinion) -- There’s nothing quite like a little bit of dollar weakness to signal traders and investors have a renewed appetite for risk. The world’s equity markets were already flashing green even before Pfizer Inc.’s Covid-19 vaccine announcement. And the euro, along with most other currencies, has been resurgent against the U.S. currency since it became clear that Joe Biden is now the President elect. But don’t confuse short-term shifts in the currency market with any diminution of the dollar's dominant position in global finance.

In fact a weaker dollar is pretty much good news for everyone, including American exporters (although an honorable exception can be made for the Japanese yen, which is getting rather too close to the 100 level with the dollar for the Bank of Japan's comfort).

While Donald Trump has yet to concede, financial markets are switching their attention back to upcoming central bank action. As the euro nears the top of its two-year range against the dollar, the foreign-exchange market matters much more for the European Central Bank, fearful of an overly strong euro choking off any nascent export-led recovery, than it does for the Federal Reserve, which has a policy of benign neglect with regards to its currency.

The most recent ECB statement highlighted “developments in the exchange rate” in its opening sentence, the first time it’s ever given such prominence to currency moves. President Christine Lagarde could not have made it clearer at the bank’s last press conference that there will be a major recalibration of its suite of monetary tools, so expect shock and awe at the Dec. 10 governing council. Economist expectations are for 500 billion euros ($600 billion) of additional quantitative easing, though it is less certain that the benchmark deposit rate of negative 50 basis points will be lowered further. The central bank’s chief economist, Philip Lane, has indicated a rate cut is something to be held in reserve should the euro’s strength start to seriously endanger the outlook for either inflation or growth.

There will also be a raft of other easing measures aimed at boosting bank lending — a point emphasized by influential executive board member, Isabel Schnabel, in a speech last week on "looking back and looking forward" on monetary responses to the Covid crisis. A second slug of bond issuance from the European Union's SURE job support program this week will underline the euro-area fiscal response to the pandemic. And there has been progress in resolving formal approval of its 750 billion-euro Recovery Fund. The key for the ECB is to keep the impression there is always more firepower if needed.

The Federal Reserve is likewise expected to be no slouch at its Dec. 16 meeting, especially if any fiscal stimulus package remains entangled in gridlock. Fed Chair Jerome Powell's speeches have been unswervingly dovish and the Fed's balance sheet has risen by nearly a quarter of a trillion dollars since July, so there is action behind the rhetoric.

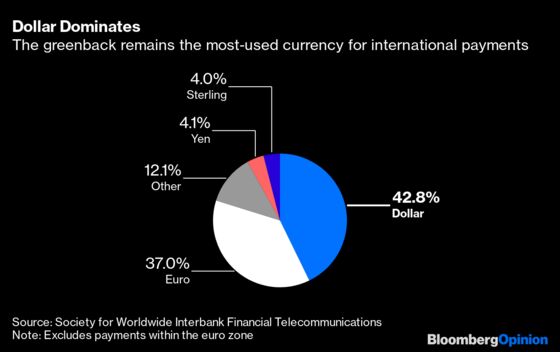

What’s clear, though, is that the current market gyrations don’t threaten to dethrone the dollar’s role as the world’s reserve currency of choice. In international payments, the U.S. currency continues to reign supreme. Excluding transactions within the euro region, the greenback has a market share of more than 42%, compared with the euro’s 37%, according to figures compiled by the Society for Worldwide Interbank Financial Telecommunications, which handles cross-border payment messages for more than 11,000 financial institutions in 200 countries.

While usage of the euro has increased modestly — that 37% share of global payments in September compares with 36.6% in the same month in 2018 — those limited gains have come at the expense of the yen and the British pound rather than the U.S. currency.

Even when including cross-border transactions between euro nations, the dollar still edges out the euro at 38.45% of worldwide international payments currently, in line with where it was two years ago and compared with 36.3% for the euro.

And in trade finance, the dollar is the undisputed king with a share of almost 87% compared with the euro’s 6.5%, little changed from where they each stood two years ago. As we argued in July, rumors of the dollar’s demise are greatly exaggerated.

Both central banks would probably prefer it if they were able to implement their respective monetary policies without tilting the exchange rate in either direction. But there are a lot of moving parts, and certainly too many factors for the ECB to relax just yet. So while Biden’s victory will be welcomed by Europe, there can be too much of a good thing if the euro rallies too far.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.