(Bloomberg Opinion) -- It’s pretty much never a good idea to call out someone else’s incorrect forecast in hindsight, especially if you’re also in the business of prognosticating (or writing opinion columns). The reason: You’ll almost surely be on the receiving end of ridicule yourself in the not-too-distant future.

This past year in fixed income, though, defies that rule of thumb. Since nearly everyone got at least something wrong, the entire bond-market community can look back and laugh at just how little they thought they knew about the stage of the credit cycle and the willingness of global central banks to abruptly change course and ease policy aggressively.

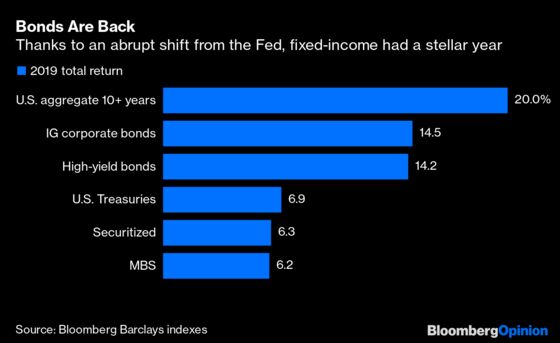

In 2019, every key U.S. bond market posted positive returns, according to Bloomberg Barclays index data. A sample: High-grade corporate debt, 14.5%; high yield, 14.3%; Treasuries, 6.9%; securitized products, 6.3%; mortgage-backed securities, 6.2%. Buying long-dated bonds in the aggregate index netted a profit of 20%. The benchmark 10-year Treasury yield fell to as low as 1.43%, from 2.68%, as the Federal Reserve embarked on back-to-back-to-back quarter-point interest-rate cuts in the second half of the year. Credit spreads are near the tightest they’ve been this economic cycle and the cost to protect against default is the lowest of the post-crisis era.

- Bank of America Corp.: “We forecast the Fed will hike rates four times in 2019, reaching a terminal funds rate of 3.25-3.50% by year-end.”

- Morgan Stanley: “We believe the credit bear market, which likely began when IG spreads hit cycle tights in Feb. 2018, will continue in 2019, with HY and then eventually loans underperforming.”

- Deutsche Bank AG: “Increasingly tight policy will push bond yields higher and lead to wider credit spreads after a near-term relief rally.”

- Nomura: “We expect 2019 to conclude the hiking cycle with up to two more hikes. … IG is still in focus (especially the BBB story) but it’s HY that could come under pressure as growth slows.”

- Citigroup Inc.: “Both equities and bonds have the potential to see positive returns in 2019. However overall return levels are likely to remain subdued.”

- BlackRock Inc.: “We see equities and bonds eking out positive returns in 2019. ... We take an up-in-quality stance in credit, and overall see limited upside and asymmetric downside as the economy enters into a late-cycle phase.”

- Pacific Investment Management Co.: “Cautious on generic corporate credit, but see relative value in financials and mortgages, modestly underweight duration.”

- Fidelity Investments: “These are fertile conditions for complacency, and there is a real risk of inflation spiraling if central banks pull back from further monetary tightening.”

Bloomberg News’s Mark Cudmore also admitted that he and the Markets Live team missed the great year for bonds: “We never saw it coming.” He chalked up the miss to underappreciating what an intensified U.S.-China trade war would mean for the global economic outlook and being caught caught off guard by the Fed’s quick and nimble shift from raising interest rates to lowering them.

I agree with both of those culprits. Looking back, I was too convinced that Fed Chair Jerome Powell would hold policy steady through trade tensions to avoid the appearance of backstopping President Donald Trump’s standoff with China. In late April, I wrote that bond traders went overboard on their rate-cut bets. In May, I still thought the Fed was committing to an aggressive pause, and in June I wrote that the market was seeing dovish signs that weren’t necessarily there. Of course, the Fed dropped its lending benchmark by a quarter point in July and did so again in September and October.

But aside from parsing Fedspeak, it’s the following takeaway from Cudmore’s retrospective that might be the most important of all, and why 2020 could most likely be another year of ever-shifting expectations:

“Perhaps the broader lesson from all our asset forecasts was a lack of ambition. We fell into the common trap of anchoring our predictions in today’s ranges, and not realizing how far things could run once a move started.”

Across Wall Street, strategists are doing the exact same thing for 2020. Consider the 10-year Treasury yield for example, which is set to end 2019 around 1.9%. Aside from outliers at Citigroup and Societe Generale, analysts at other primary dealers see the yield in a tight window of 1.5% to 2.25% in 12 months’ time.

As for high-yield debt, analysts are forecasting a total return between 1% and 7.5%, which equates to fairly benign price swings given the securities’ large interest payments. The median annual return on the Bloomberg Barclays high-yield index since 1984 is 7.5%.

I wrote earlier this month about the bold call for 10-year yields from John Dunham. He sees inflation rapidly picking up in the first half of 2020, freaking out the Fed and forcing policy makers to raise interest rates again. Then, toward the end of the year, he sees the U.S. tumbling into a recession. That’s how the benchmark Treasury yield rises past 3% come September and drops to a record low 1.3% by mid-2021.

Is that precise sequence of events — and ensuing wide price swings — likely to play out? I’m not so sure. It certainly stands in stark contrast to BlackRock’s three overarching ideas for 2020: “modestly positive on risk assets,” “neutral on global duration and cash” and “cautious cyclical rotation.” Don’t get me wrong: Strategists at the world’s biggest money manager have sound reasoning for those views. But they risk falling into the same trap that snared Wall Street in 2019.

One idea BlackRock and Dunham agree on: The risk of accelerating inflation is underappreciated in markets. That might be the one thing that could most quickly reverse 2019’s bond boom. The median forecast of 61 analysts surveyed by Bloomberg calls for the 10-year U.S. yield to end 2020 at 1.94%, just about where it is today. If longer-term yields were forced to move higher in a hurry, that would cause a lot of pain across fixed-income assets.

The future, it turns out, is often quite difficult to predict. As the 2020s begin, perhaps it’s best to borrow a page from the Fed’s 2019 playbook: Take your best shot at forecasting the road ahead, but don’t hesitate to react to important new information.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.