(Bloomberg Opinion) -- Barnes & Noble Inc. is finally closing the books on its nearly 26 years as a publicly traded company.

Leonard Riggio, its 78-year-older founder and chairman, and the rest of the Barnes & Noble board agreed on Friday to sell the bookstore chain for $683 million (including debt) to funds affiliated with Elliott Management Corp., the investment firm led by billionaire Paul Singer. Elliott acquired Waterstones, a U.K. book retailer, a year ago, and it plans to have the Waterstones CEO manage Barnes & Noble’s operations as well once the transaction closes.

When Barnes & Noble listed on the New York Stock Exchange in 1993, it had a market capitalization of around $800 million. It’s now exiting the market for far less in an anticlimactic chapter in the company’s storied history. The Barnes & Noble name traces its roots to a Fifth Avenue New York store opened during the Great Depression, which later became its flagship location but eventually shut down in 2014. That’s now a Banana Republic.

Barnes & Noble remains the country’s largest operator of bookstores, but it’s a title that means little today. From a 1993 New York Times article about the stock’s debut:

Currently with 168 superstores, Barnes & Noble has become the Home Depot of the book superstore business. Its largest competitor among superstore operators, Borders, a unit of Kmart, has 35 superstores.

Only one of the companies named there — Home Depot Inc. — is still truly relevant. And Borders, formerly one of Barnes & Noble’s biggest competitors (and one of my employers during college), went out of business eight years ago. Barnes & Noble’s decline has been much more graceful. But just like other retailers that don’t fulfill as a big of a need in the age of Amazon.com Inc., Barnes & Noble will continue to fade from shoppers’ memories.

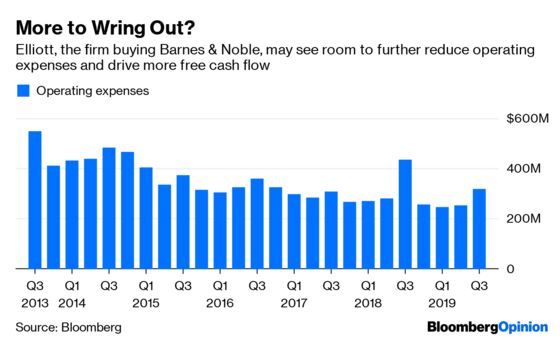

In the meantime, Elliott sees money to be made.

Elliott is paying $6.50 a share in cash, a 33% premium to Barnes & Noble’s average closing price over the last 20 trading sessions. However, the stock traded above that level as recently as December, and it’s been falling steadily for more than four years as the chain failed to secure an acquirer sooner.

The takeover offer values Barnes & Noble at a mere 4.7 times estimated Ebitda for fiscal 2020, which began in May. U.S. specialty retailers are valued on average at just less than 9 times forward Ebitda. And on a revenue basis, Elliott is paying only about 20 cents on the dollar for Barnes & Noble, a large discount to the median sales multiple in other U.S. retailer acquisitions of the last five years. Staples Inc., the office-supply chain, sold for about 35 cents on the dollar to private equity firm Sycamore Partners in 2017.

Barnes & Noble still has more than 600 stores across the U.S., which threw off nearly $200 million of cash last quarter, hence the interest from a financial buyer like Elliott. Its $113 million of net debt, with a maturity date of 2023, is also manageable. As for Waterstones, its new sister company, the press release announcing the deal said that the chain “has successfully restored itself to sales growth and sustainable profitability” under CEO James Daunt by investing in the stores and through “empowerment” of local staff. Daunt will now try to adopt similar strategies at the U.S. business.

As for Barnes & Noble, there are probably benefits to managing its challenges away from the public eye. But the deal also signals that a relatively cheap bid was more attractive than trying to regain the confidence of public market investors. It’s a bittersweet ending for Riggio, no doubt, but turning a page on what is still America’s largest bookstore chain is better than the alternative.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.