Barclays’ Stock Traders Finally Catch Up to the Bond Desk

(Bloomberg Opinion) -- Barclays’ stock traders have found themselves on near-equal footing with the bond desks – it must be a strange feeling.

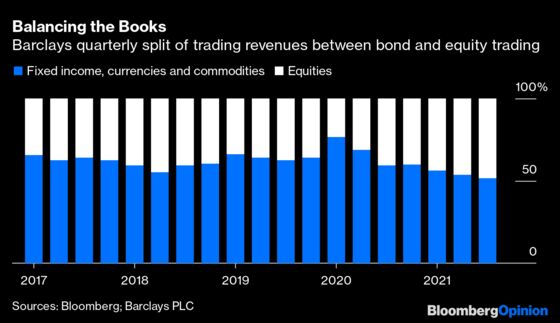

The bank has always been known as a bond house: Ever since its first forays into investment banking and trading, the business has been biased toward helping companies sell debt and trading in those markets.

Now it looks to be finally making the grade in stocks. In the third-quarter results on Thursday, Barclays trading revenue from equities and bonds was split almost 50-50. That’s a big move, since equities contributed an average of less than 40% of quarterly trading revenue in the four years before 2021.

Chief Executive Officer Jes Staley has long talked about the benefits of businesses that balance each other out. His idea is mostly about the see-saw relationship between consumer banking and investment banking, where over the long term one tends to be on the up when the other isn’t doing so well.

The approach, taken directly from his former boss at JPMorgan Chase & Co., Jamie Dimon, has worked well during the pandemic. As Covid buffeted economies, investment banking and trading boomed, while traditional lending ground to a halt.

At Barclays’ investment bank, the ebbing of 2020’s bond-market volatility was offset by this year’s gains in stock-trading activity.

Equities traders increased third-quarter revenue by more than 16% from the same period a year earlier – behind growth at even the worst-performing U.S. bank, but still much better than forecast, according to Bloomberg data. Revenue for bond traders fell 15% – better than Citigroup Inc., worse than Bank of America Corp. and JPMorgan.

Driving the equities result was Barclays’ growing business of lending to and trading with hedge funds; the bank reached a record level of exposure to hedge fund trades in the quarter, measured in terms of the balances in its prime-brokerage business.

Whether Staley can sustain the equities gains depends both on the competition and the amount Barclays will spend on technology in what has increasingly become a computer-driven arms race. Barclays, like some U.S. banks, has benefited from the retreat by Credit Suisse Group AG after it lost $5.5 billion this year on the collapse of Archegos, a New York-based family office.

Barclays is likely to have the cash to keep investing. Having spent several years bolstering its balance sheet, the bank now has more capital than it requires. It targets a 13%-14% capital ratio – which is the amount of common equity per pound or dollar of risk-weighted assets. It finished the third quarter at 15.4%.

By the end of the year, it might be sitting on almost 3 billion pounds ($4.1 billion) more capital than it needs. It’s already buying back 1.2 billion pounds of shares this year, and it could do a lot more next. Staley told investors on Thursday that it would be important to have the right “cadence” to capital returns. That suggests he won’t hand back all the cash at once, but that he wants to mimic the rhythm of steady buybacks that U.S. banks have established over the past few years. JPMorgan, for example, has bought back an average of almost $5.5 billion per quarter since 2017, excluding the three quarters last year when buybacks were barred by regulators in the U.S. and elsewhere.

For most investors, the best and simplest way to judge any large, complex financial institution is whether it can regularly put cash in your hands. If Barclays can convince investors it can do that, its stock should continue to improve its valuation.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2021 Bloomberg L.P.