Wall Street's Big Moneymaker Isn't Sexy

Cash management may not have the lure of fintech. But there’s plenty of disruption in this staid corner of the financial sector.

(Bloomberg Opinion) -- Few dispute that Chinese tech giants have shaken up retail banking, changing how millions of customers do everything from paying their bills to choosing insurance. But the real disruption may be occurring in a more staid corner of finance – and it’s being led by Wall Street.

As investment-banking revenues slumped in the wake of the global financial crisis, traditional broker-dealers found that trading and dealmaking weren’t cutting it. Steadier money could be made in cash management, the humdrum business of assisting multinational companies with daily liquidity, and getting the most out of idle deposits by deploying them in global markets.

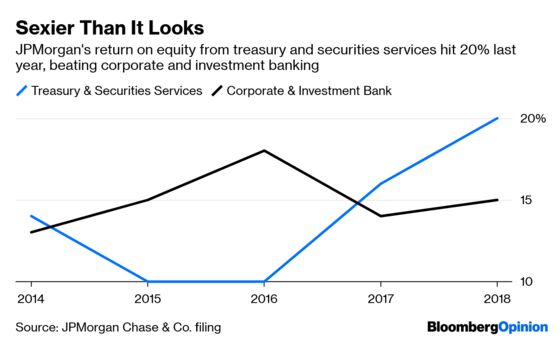

JPMorgan Chase & Co.’s treasury-services business, its lingo for cash management, hit a 20% return on equity last year, compared with 15% for its corporate and investment bank. Citigroup Inc., a global leader in this area, posted a return on equity from transaction banking (which is dominated by cash management) in the mid-20% range, according to a 2017 investor presentation.

These sort of results underpin Goldman Sachs Group Inc.’s recent decision to use technology to make a splash in cash-management – in Japan, among other countries – as part of a global push later this year. The country’s appeal is two-fold. Corporate treasuries everywhere seek yen assets when they want to hide from global turmoil. Meanwhile, Japan could also support Goldman’s fledgling ambitions in online retail banking, which requires reliable access to liquidity. Taking a digital platform to cash-rich, yield-hungry Japanese companies – and snagging even a sliver of their deposits – would mean cheaper funding than the wholesale market.

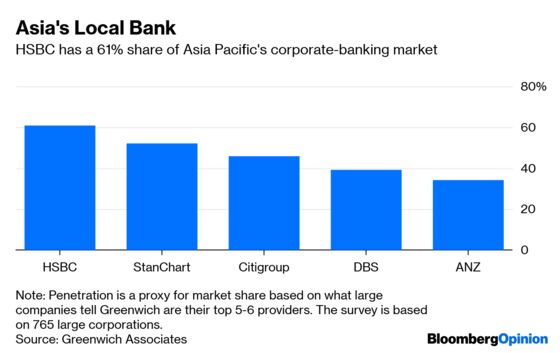

It should also help Goldman that Japan's megabanks don't even crack the top 15 among Asia-Pacific cash-management leaders, according to Gaurav Arora, head of Asia Pacific at Greenwich Associates. While Mitsubishi UFJ Financial Group Inc., Mizuho Financial Group Inc. and Sumitomo Mitsui Financial Group Inc. are upgrading their technology and expanding their digital reach, they remain well behind global players. Out of Mizuho’s surprise 680 billion yen ($6.2 billion) writedown in March, about 460 billion yen was related to a long-delayed move to integrate its computer systems. For their part, the megabanks must be worried about Goldman’s arrival. The likes of Citigroup Inc. and HSBC Holdings Plc were already beginning to challenge Japanese banks’ long-standing domestic client relationships by winning over their overseas units.

While the initial costs involved in building out a platform are high – think of all the banking licenses and regulatory approvals required in a vast region like Asia – cash management is sticky. Once a finance department adopts and integrates a bank’s system, it doesn’t flip for a competitor easily. This is also a low-margin business albeit with high operating leverage; it doesn’t require capital set aside to manage the risk of credit losses. And unlike investment banking, growth doesn’t depend on million-dollar bankers.

Japan could become a testing ground to move this business fully online. Goldman inevitably will need brick-and-mortar partners to manage the physical cash collected by domestic distributors for multinational clients such as Procter & Gamble Co. In that vein, the bank’s entry could be a model for other Wall Street firms that lack a physical footprint. But global banks already big in cash management have a major advantage: They can simply protect their turf by beefing up digital offerings.

The idea that banks’ software should seamlessly connect with clients’ online applications is gathering interest. Three-quarters of large companies in Asia Pacific said they sought so-called open banking arrangements, with treasury-management among their top three priorities, according to an Accenture Plc survey last year. Half of the bankers in the region expect 5% to 10% of their divisions' revenue growth in the next three to five years to come from open banking for commercial customers. Another 43% gave even more optimistic forecasts to the the consulting firm.

Managing corporate cash online isn’t as sexy as a consumer super app. But it’s not yet clear that retail customers can transition from keeping small sums on deposit for movie tickets and pizza delivery to forking over substantial shares of their income and wealth to web-only banks, as we wrote previously. Without steady retail deposits, the fintech dream of lending to small businesses will remain just that.

Eking out a digital win for a bank like Goldman, which can lean on its investment-banking relationships to sign up cash-rich multinationals, is perhaps a more modest leap of faith – and the landing may be more sure-footed.

This is the last time the bank disclosed the figure publicly.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.