(Bloomberg Opinion) -- JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon made no secret that he wanted to buy back some of the bank’s stock before the roaring equity market rally took it too far. “I hope we can do it before it goes way up,” he said in July.

Five months later, right in the heart of the holiday season, the Federal Reserve made his wish come true. And he and JPMorgan could hardly wait to share the good news.

After running a second round of stress tests, the central bank concluded that the biggest lenders could handle a severe economic shock, given their current capital levels, according to results released late Friday. As a result, the Fed loosened its restrictions on cash distributions, which were put in place in the wake of the coronavirus pandemic. While the banks still can’t increase their dividends beyond what they paid out in the second quarter of 2020, they can now resume buybacks, provided the combined amount doesn’t “exceed an amount equal to the average of the firm’s net income for the four preceding calendar quarters.”

Just 10 minutes after the Fed’s stress tests were made public, JPMorgan announced a new $30 billion share buyback program starting in the first quarter; it also maintained its dividend of 90 cents a share. Shares climbed 5% in after-market trading.

“Our highest and best use of capital continues to be supporting our clients and driving an inclusive economic recovery,” Dimon said in a statement. “We will continue to maintain a fortress balance sheet that allows us to safely deploy capital by investing in and growing our businesses, supporting consumers and businesses, paying a sustainable dividend, and returning any remaining excess capital to shareholders.”

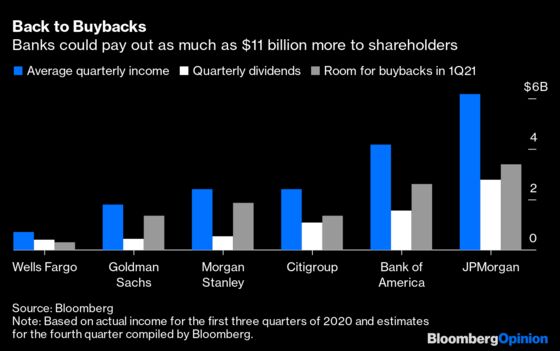

JPMorgan was first out of the gate but hardly the last. Waiting a half hour until after the stress-test results, Goldman Sachs Group Inc. said it would also start buying back shares in the first quarter. Before the announcement, Wells Fargo analyst Mike Mayo suggested Bank of America Corp. and Citigroup Inc. would most likely be the greatest beneficiaries if the Fed allowed new buybacks, given that they trade close to or below book value.

All told, Bloomberg News’s Jesse Hamilton and Yalman Onaran crafted the following chart that shows the potential distributions in the coming quarter from the six largest U.S. banks:

Interestingly, leading up to the stress-test results, Mayo and his fellow analysts weren’t at all confident that the Fed would ease up on lenders, expecting that the optics around Wall Street stock buybacks in the midst of a resurgent Covid-19 pandemic would be too much for the central bank to withstand.

Instead, only Fed Governor Lael Brainard, who could be in line to succeed current Fed Chair Jerome Powell after his term is up, voted against the decision. “Prudence would call for more modest payouts to preserve lending to households and borrowers during an exceptionally challenging winter,” she said.

Fed Vice Chairman for Supervision Randal Quarles struck a different tone in the central bank’s statement. “The banking system has been a source of strength during the past year, and today’s stress test results confirm that large banks could continue to lend to households and businesses even during a sharply adverse future turn in the economy,” he said.

They’re both right, in a way. Purely looking at the Fed’s preferred figures, there’s little doubt that the banks are well capitalized. The central bank said that under two hypothetical scenarios with severe global recessions, large banks would have more than $600 billion in combined total losses, but their capital ratios would fall from 12.2% on average to 9.6% in the more severe scenario, still more than double the 4.5% minimum. All of the banks’ risk-based capital ratios would stay above the minimum threshold.

Yet from a public perception standpoint, it doesn’t feel quite right to declare the good old days of bank buybacks are here again just as President-elect Joe Biden warns of a “dark winter” ahead and many families across the U.S. are experiencing a challenging holiday season. I wrote early in the pandemic that banks quickly pivoted to play the “good guy” role in this crisis. Lately, however, they’ve turned back to their old ways of seeking out ways to cut expenses — and, in some cases, jobs — to boost profitability.

Here’s one way to spin it: Everyone is eager for a return to normal in 2021. It wouldn’t be that way without Wall Street buybacks.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.