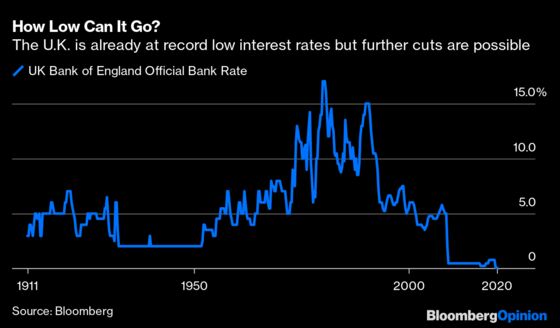

(Bloomberg Opinion) -- Should U.K. interest rates be taken negative? It would be a monumental gamble that might threaten the health of the country’s banking sector and its ability to manage its current account deficit.

Despite the risk, the Bank of England is exploring whether this option could be used if the economy fails to recover from the pandemic, or if more lockdowns are needed. You can see why it would look at this, but the messaging has caused more confusion than clarity. It would be better if BOE Governor Andrew Bailey stated his order of preferences for how the bank would respond to a sustained economic crisis. That would be proper forward guidance.

The first option would be more BOE bond buying through an expansion of its quantitative-easing program. This could be reinforced by cutting rates on its already very cheap loans to the banks. If that didn’t work, the U.K.’s 0.1% interest rate could be cut to zero. A recent study from Israeli academics and a European Central Bank working paper show that zero rates might encourage more borrowing than negative rates — in part because the latter can spur risk aversion.

If all else fails, then negative rates could be used as a last resort, but no one should be ignorant of the dangers. The most obvious concern is Britain’s sustained current account deficit. Because the U.K. imports more than it exports, it relies on foreign capital. Negative rates could put that funding source at risk.

Some fans of negative rates point to the ECB, which has long been in sub-zero territory as it props up the euro zone economy. But there are big differences with the U.K. Britain has an outsized financial sector, which would suffer from negative rates, especially its large insurance and pension industries.

The country’s fledgling “challenger bank” sector is already struggling with narrowing net interest margins and it might not be able to come up for air with sub-zero rates. Likewise, such a change could ruin the building societies that provide many U.K. mortgages. More concentration in the hands of big banks and a devastated savings sector is hardly a recipe for economic recovery.

Besides, the benefits of the ECB’s negative rates are far from clear. The euro area has struggled for growth despite continuous multi-trillion euro injections of liquidity and QE.

The chief benefit to the ECB has been keeping a lid on euro currency strength, which helps exporters. But that too has created problems for European countries outside of the euro zone. Denmark’s and Switzerland’s experiments with negative rates are almost solely down to stopping their currencies from appreciating versus the euro. Sweden has given up on negative rates and raised its benchmark back up to zero.

The pound is weak anyway because of the Brexit process but removing any positive interest-rate prop would leave it vulnerable to collapse.

The BOE is right to assess what negative rates might achieve if Britain’s huge fiscal and monetary splurges fail to deliver a recovery. But it should make its road map clear and only adopt negative rates if the economy is demonstrably failing. That is the sensible thing to do.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.