Bank of America Shows Rivals Are Leaving Money on the Table

(Bloomberg Opinion) -- Bank of America Corp. did something JPMorgan Chase & Co. didn’t in the third quarter: It beat expectations for net interest income — and handsomely, too.

This revenue line is a big focus for investors watching banks’ third-quarter earnings: Bank of America, Citigroup Inc. and Wells Fargo & Co. all reported Thursday after JPMorgan did so on Wednesday.

Bank of America is the standout among all four, mainly because it is sweating its excess cash harder. The question is whether it is risking too much for these extra rewards, and the answer for once is no. Its rivals truly do seem to be leaving money on the table.

Interest revenue at Bank of America rose to $11.2 billion on a fully taxable basis, up 9% from the third quarter last year and better than consensus forecasts of $10.7 billion, according to Bloomberg data. At the other three banks, this line was flat or lower.

Net interest income was always going to be the story of this quarter, but the plot has surprised me. It isn’t a tale of whether loans are starting to grow as the pandemic ends and the economy gets back to normal. Instead, it’s about what the banks are doing with the billions of dollars of excess cash that consumers and companies are sticking in their accounts.

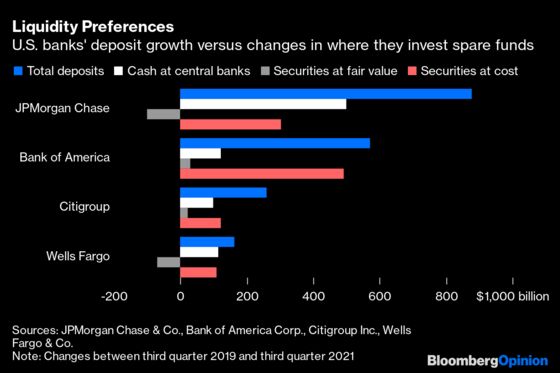

Total deposits at these four banks have grown by a combined $1.9 trillion in the two years since the third quarter of 2019. We’re getting a little blind to big numbers, but that’s a lot by any reckoning.

The banks have to pay interest on lots of those deposits. Well, not much, but they still need to put the money somewhere that will pay them something back. When the deposits are rolling in but loans are being repaid and fresh ones aren’t much in demand, the banks have two main places where they can deploy the money. They can hold central bank money as deposits at the Federal Reserve or its peers, or they can buy Treasuries, agency mortgage bonds and other super-safe debt.

Bank of America has put nearly 90% of the extra deposits it received into Treasuries and other safe debt, much more than its rivals have done. JPMorgan has put 35% of the extra deposits into such securities, the least of these four banks.

So what’s going on? JPMorgan’s chief financial officer, Jeremy Barnum, said he worried about volatility in bond markets and the possibility of losing money put into the Treasury market. He pointed to the threat of inflation and what that could do to rates. Those are all fair points.

But look a bit closer at how banks are putting money into securities. They can buy bonds and keep them on the books as “available for sale,” which means they have to update their values regularly as markets move. If yields jump higher, banks book a loss on the value of their bonds. Alternatively, they can keep their bonds as “hold to maturity.” If they have no plans to sell them, they can just clip the coupon and not worry about where the market goes.

All the banks have been avoiding market volatility by putting more of their bond holdings in the hold-to-maturity bucket. Meanwhile, the available-for-sale buckets have either grown only slightly or shrunk, as they have at JPMorgan and Wells Fargo.

There is another risk that banks miss out on more income if rates rise and they are holding lots of low-yielding bonds until they are repaid. Bank of America Chief Financial Officer Paul Donofrio wouldn’t say much about the duration of the bonds it holds, but he did say they have much shorter maturities than most people seem to suspect.

One way of judging this is to look at the average yields the banks get. Bank of America was getting about 1.39% on its debt securities in the third quarter, compared with 1.32% for JPMorgan and 1.52% for Citi. So it doesn’t look as if Bank of America is sticking its neck out there, either.

There’s another reason to prefer holding central bank reserves instead of Treasuries, which has to do with regulatory requirements around liquidity. This was part of the story of the September 2019 blowup in repo markets — where banks and investors swap safe bonds for cash.

A discussion of this would be another column in itself. But it’s sufficient to say that all of these banks have more than enough cash on deposit at central banks: Bank of America, Citi and Wells all have at least $100 billion more than they did two years ago. JPMorgan has nearly $500 billion more.

However, you cut it, Bank of America’s rivals could be getting a lot more bang for their buckets of excess bucks.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Paul J. Davies is a Bloomberg Opinion columnist covering banking and finance. He previously worked for the Wall Street Journal and the Financial Times.

©2021 Bloomberg L.P.