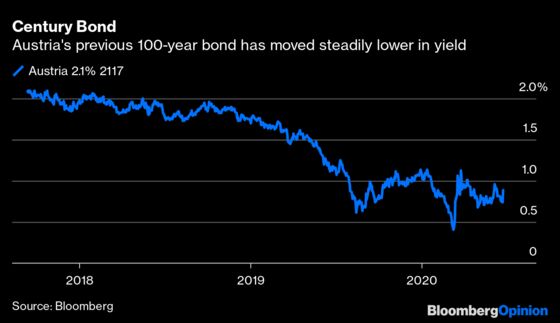

(Bloomberg Opinion) -- Nothing says it’s cheap to borrow quite like a 100-year bond with a yield of 0.88%. Austria returned to the century-bond club on Wednesday with a new 2 billion-euro ($2.3 billion) debt issue on its most favorable terms yet.

It’s the clearest example of how the European Central Bank’s 1.35 trillion-euro pandemic bond-buying — alongside a similarly sized injection of liquidity into the banking system — is encouraging greater risk taking. That’s what it was designed to do, for issuers and investors alike. The risk for Austria was that the sale was well-received, because the market for these ultra-long issues is thin (although such is the appetite for any safe yield that this auction was more than 10 times oversubscribed). The risk for investors is that the bond doesn’t pay out for 100 years and they’re hardly getting a handsome coupon.

The sale may just be the start of a wave of European sovereign issues as governments raise a lot more debt to finance their pandemic economic responses. What would have seemed like crazily low yields three years ago are just run-of-the-mill now as rates are driven lower by the gush of money flooding Europe’s finance system. While Italy has suffered the most from Covid-19 in the euro zone, its 10-year bond yields have still fallen by nearly 100 basis points over the past two months.

For its part, Austria’s new issue is a vivid example of how desperate investors are to snap up highly rated securities that yield something (anything).

Other European nations such as Ireland and Belgium have also issued 100-year debt but only in private placements. France has sold 50-year maturities, as has Italy. They might be tempted now to follow Vienna’s lead. With Germany also recently raising its largest amount of 30-year debt, at a negative yield, might Europe’s most powerful country finally be tempted to follow its southern neighbor and elongate its bond-maturity profile?

Fixed-income investors looking to boost returns in this yield-starved environment can either take greater credit risk (by buying junk bonds, for example) or reach for ever longer duration. The sensible ones will do a bit of both. Austria has the second-highest investment grade credit rating of AA+, hence the strong demand, especially from pension funds and insurance companies looking for ultra-long assets to match their future liabilities.

With long-maturity debt, investors get an additional benefit called “positive convexity,” a bit of bond-market math magic that can improve returns. The attraction of ultra-long bonds with very low coupons is that their prices rise more sharply when yields fall than they decline when yields rise. This means the price outperforms when interest rates drop (as they’re doing now), which is overall good news for investors.

Austria’s positive experience with longer debt means more European countries are likely to follow. At this rate, 30-year debt will soon just be viewed as medium-term maturity.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.