Australian Banks Are Crashing Down to Earth

(Bloomberg Opinion) -- For decades now, Australian banks have been a class apart.

Thanks to a ceaselessly growing economy, an oligopolistic structure that prevents mergers between the big four lenders, and the loyalty of self-funded retirees who play a large part in the local stock market, they’ve been valued as if they’re in a fundamentally different business from counterparts in other countries.

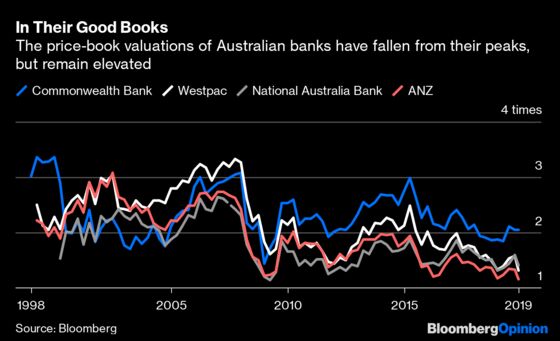

At their peaks, Commonwealth Bank of Australia, Westpac Banking Corp. and Australia & New Zealand Banking Group Ltd. were all priced at more than three times book value. That’s extraordinary in an industry where the share price should tend to cleave fairly close to the value of net assets, and where the median valuation among large banks in developed markets is 0.77 times book.

Tuesday’s announcement that Westpac Chief Executive Officer Brian Hartzer has resigned after the company was accused of 23 million separate breaches of money-laundering regulations should be a wake-up call. While valuations have slipped in recent years thanks to a teetering housing market and a government inquiry into the sector, Australia’s banks still have further to fall.

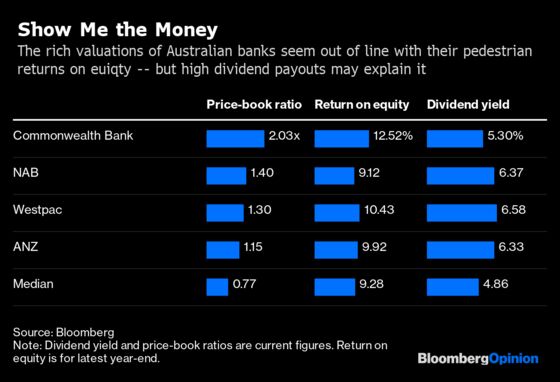

If you look at them in terms of return on equity, the big four are distinctly middle-of-the-road. All are around the median deciles relative to their peers in other countries except for Commonwealth Bank, with National Australia Bank Ltd. somewhat below the midpoint.

Switch to price-book measures, though, and they’re close to the top of the pack, with the Commonwealth at number three in the world.

The best explanation for this is probably their reputation as excellent dividend payers. Given the vast uncertainties around bank earnings due to regulatory requirements and the fuzziness of working capital and capital expenditures, dividends are often regarded as the most solid basis for a real understanding of a bank’s future cashflows. Given that shareholders are ultimately paying for a right to a slice of those cashflows, it’s natural that banks with above-average dividend yields should have above-average valuations, too.

Australia is relatively exceptional on that front. All of the big four barring the Commonwealth are in the second-highest decile among their peers in terms of analysts’ estimates for blended-forward 12-month dividend yields. Combined with the fact that Australia’s army of affluent retirees show an unusual loyalty to household-name blue-chip companies that pay a reliable income stream of shareholder returns, it’s little wonder the sector is outperforming.

There’s a problem on the horizon, though. As Bloomberg News’s Emily Cadman has written, the dividend party could be coming to a close. Payouts have already been reduced at Westpac and National Australia Bank, and ANZ has cut the amount eligible for tax refunds, as the big banks have been forced to set aside more capital by the regulator.

Such balance sheet reinforcement should at least be a temporary measure, but even once they’re paid there are further risks to cashflows. Australia’s economy is slowing, as my colleague Daniel Moss has written.

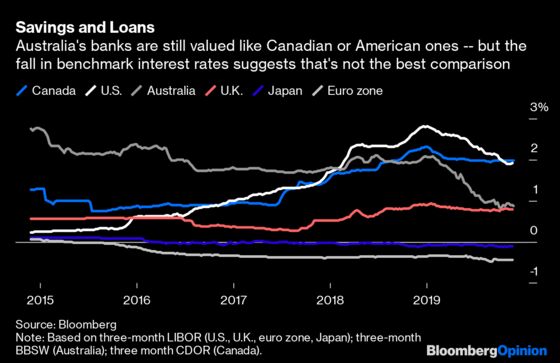

Interest rates, as measured by three-month interbank benchmarks, look closer to those in the U.K. than the country’s bank valuation peers in the U.S. and Canada. That’s likely to have a rough knock-on effect on earnings, given the tight relationship between borrowing costs and net interest margins, a key determinant of bank profits.

Even if the current rebound in the housing market translates into a more sustained upswing, there are challenges. Any banks wanting to take advantage of that by lending more aggressively are going to need to find a way to attract more deposits, which will put further pressure on interest margins given the low rate environment.

All of that should serve to reduce the reliability of those dividend payouts — and without that, Australia’s retirees may find there are other blue-chip businesses worthy of investment.

Westpac shares have reacted positively to the news of the clean-out at the top of the bank, but don’t expect the big four to find recovery from their malaise easy. Australia’s banks have been cash machines while the economy prospered. As it struggles to relight the fire that powered it for the past three decades, that money could be drying up, too.

We've confined our universe to banks with more than $100 billion in assets in North America, Western Europe and developed Asia-Pacific markets.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.