(Bloomberg Opinion) -- If AT&T Inc. starts to look like it’s standing a bit taller, that’s the result of it no longer stuck carrying around the weight of a mangled satellite business.

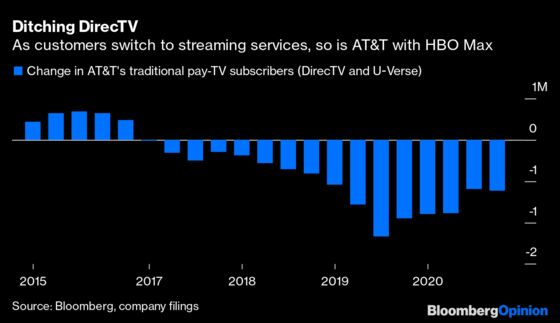

The wireless carrier announced late Thursday that it’s separating DirecTV and its other U.S. pay-TV products — AT&T TV and U-Verse — into a separately run company that will be 70% owned by AT&T and 30% owned by private equity firm TPG Capital. The transaction values the business being carved out at $16.25 billion including debt, a fraction of the $67 billion that AT&T paid for DirecTV in 2015. Needless to say, it did not earn a particularly high return on the DirecTV investment, but at this point, the value of not owning this antique collection is the true prize.

The deal allows CEO John Stankey and the rest of AT&T to devote their focus to products of the future rather than the past: that is, the company’s 5G wireless network and HBO Max streaming-video service. AT&T will also reap $7.6 billion in cash from the separation and hand off $200 million of existing DirecTV debt. One of the biggest benefits, though, is that its earnings reports will no longer need to call attention to DirecTV, nor will executives have to continue struggling to defend owning the business. The magic words of Thursday’s press release: “Following close of the transaction, AT&T expects to deconsolidate the U.S. video operations from its consolidated results.”

Why retain a stake at all? The likeliest reason is that AT&T, after a long and thorough search, couldn’t find a buyer willing to buy the whole thing at a palatable enough price. In the end, it did the deal it could do. The biggest downside, though, may be absorbed by customers, which in this case includes subscribers in rural markets without many video-entertainment alternatives. As a recent DirecTV user, it was evident that the service wasn’t high on AT&T’s list of priorities. It’s not unreasonable to worry that in private equity’s hands, product enhancements could fall further by the wayside. In deals such as these, the euphemism is that the owners “run the business for cash,” milking what they can for as long as they can.

AT&T, the most indebted non-bank corporation in America, could certainly use the cash. Even as it tries to reduce debt via various asset sales, AT&T needs to make important investments in its wireless network. It recently bid $23 billion in a Federal Communications Commission auction of U.S. airwaves ideal for 5G connections, and the FCC’s acting chair is eyeing yet another auction for more so-called mid-band spectrum later this year. AT&T recently signed a bank loan for $14.7 billion to use on such purchases, and it includes a covenant requiring the company’s net-debt-to-Ebitda ratio to go no higher than 3.5; AT&T reported an adjusted ratio of 2.7 as of the end of 2020.

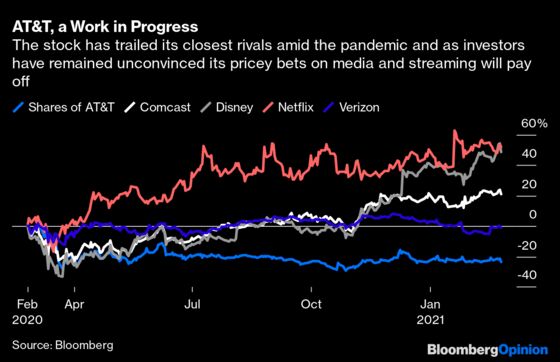

AT&T needs to step up its efforts in both 5G and streaming. In 5G, T-Mobile US Inc.’s takeover of Sprint Corp. last year effectively gave a major rival a boatload of advantageous spectrum. As for streaming, HBO Max is still playing catchup after the pandemic shut down Hollywood studios. In turn, it made the costly but wise decision to put all 2021 Warner Bros. films on the app the same day they hit theaters to juice subscriber gains. Meanwhile, Netflix Inc. recently announced that it no longer needs to borrow money to finance its day-to-day operations, a sign of its increasing strength vis a vis the competition. Walt Disney Co. reorganized its operations around streaming and is planning to come out swinging with lots of new “Star Wars” and Marvel programs. And a new entrant was unveiled Wednesday night that might just give HBO Max a run for its money: Paramount+.

On the road to the streaming future, it pays for AT&T to travel light.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering the business of entertainment and telecommunications, as well as broader deals. She previously wrote an M&A column for Bloomberg News.

©2021 Bloomberg L.P.