(Bloomberg Opinion) -- It looked like buyout firm Advent International and Singapore sovereign wealth GIC had left nothing to chance when they agreed to buy Swedish Orphan Biovitrum AB (Sobi) for $8 billion in September. The billionaire Wallenbergs, with 36% of the biotech company, immediately pledged to accept the offer, as did a Swedish state pension fund with 7%.

Not AstraZeneca Plc. The U.K. drugmaker, with an 8% holding (according to its 2020 annual report), hasn’t declared its intentions. The silence is becoming deafening.

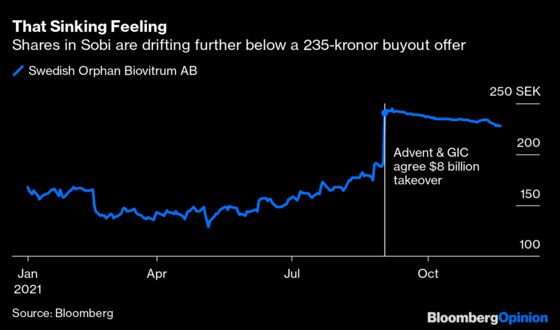

The bidders have acceptances covering some 85% of the shares, but they have made the offer conditional on getting to 90%. At that level, Swedish law allows them to squeeze out the last minority shareholders. And having full control is usually key to getting the best financing terms. On Tuesday, the group pushed back the deadline for acceptances from Nov. 26 to Dec. 1. It also said it wouldn’t lower the acceptance hurdle. The message to the stragglers here is stark: Hurry up and tender your shares, and you’ll have the money in your account in December.

If the latest count excludes AstraZeneca’s stake, the firm’s assent would get the transaction over the bar. If it has accepted (or plans to accept) the offer, then it’s strange and unhelpful that it hasn’t said so. A weakening Sobi share price, currently 6% below the bid, suggests some market doubts about the deal succeeding.

It’s not clear why the U.K. drugmaker is being coy. Could it want a sweetener? Assuming it hasn’t tendered, haggling for a 5-10% bump on a stake worth about $630 million at the bid price hardly seems worth it. After all, AstraZeneca has a market value of $175 billion.

The alternative explanations would be more strategic. AstraZeneca has its eye on some of Sobi’s drugs, according to Dagens industri. Conversely, maybe it has an interest in preserving the status quo or preventing a rival getting hold of Sobi.

Sobi issued the U.K. firm 24 million shares in 2019 as part payment for the U.S. rights to Synagis, a drug to combat a rare respiratory disease, plus rights to half the U.S. earnings of a related medicine in development. If Sobi goes to Advent and GIC, that would create an element of uncertainty about who ends up owning the rights when the duo seeks to exit. The buyout could be a step to Sobi becoming part of another pharmaceuticals giant.

Of course, were a competing pharma company trying to buy Sobi today, the acceptance requirement would likely be lower than what the buyout consortium is demanding: A corporate bidder could probably finance an acquisition of this size from its own resources. AstraZeneca would be powerless to stop it. But given that, why didn’t AstraZeneca negotiate change-of-control provisions in the original partnership deal?

What didn’t matter then may matter now. AstraZeneca’s strategy has changed since 2019. Its July acquisition of Alexion Pharmaceuticals Inc. has added rare diseases as a new pillar of the strategy.

When the Sobi takeover was agreed upon over two months ago, the strength of the share price reaction suggested the main threat to completion was a gatecrasher. Advent and GIC can be glad that didn’t materialize. But the nailbiting finish is a reminder to buyout bidders that they need the support of pretty much all shareholders — not just the ones with the biggest holdings.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2021 Bloomberg L.P.