Aston Martin Is a Binge Too Far for China’s Geely

The Geely Group has held preliminary talks about a possible investment in Aston Martin Lagonda Global Holdings Plc.

(Bloomberg Opinion) -- Timing is everything in investing, a refrain the ambitious Li Shufu might want to heed.

The Geely Group has held preliminary talks about a possible investment in Aston Martin Lagonda Global Holdings Plc, the high-end but encumbered British carmaker of James Bond fame. Billionaire Lawrence Stroll, owner of the Racing Point Formula One team, is also among the investors looking to pump in fresh capital.

At first blush, this isn’t surprising. Struggling to dent the world market with Geely Automobile Holdings Ltd.’s own vehicles, the Chinese auto executive has developed a modus operandi of appearing to ascend the value chain by picking up marquee brands, financially precarious though they may be. Through his holding company Zhejiang Geely Holding Group, Li splashed out $9 billion to build a 9.7% stake in Mercedes Benz-maker Daimler AG in 2018. Zhejiang Geely owns or has stakes in Volvo AB, Lotus Cars, Malaysia’s Proton Holdings Bhd and even a flying car company, Terrafugia Inc., either directly or through its subsidiaries.

Li is trying to stay ahead of the expensive technology curve. Earlier this month, Geely set up a joint venture with Daimler to make the electric version of Smart cars in China. The company has an electric vehicle battery joint venture with South Korea’s LG Chem Ltd. Geely has also used Volvo Car Group in a joint venture to subsidize Lynk & Co., a more upmarket version of Geely’s homegrown brands that’s so far sold primarily in China.

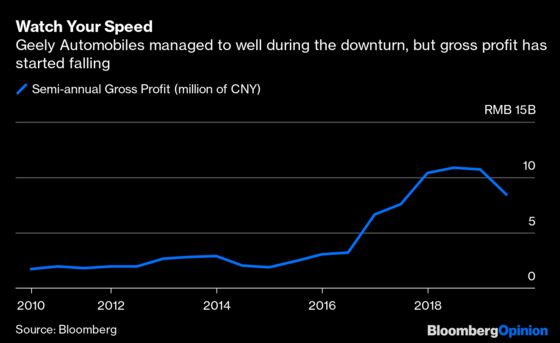

So, Aston Martin seems to fits in. But this time, Li has more to consider: business at home. Geely Auto sold 1.36 million cars last year, posting $2.8 billion in profit for the 12 months to June 30, but the Chinese market is struggling to find a footing. Retail car sales tumbled more than 7% in 2019, with production down 9.5%. All told, sales in the world’s largest car market are shrinking and the competition to survive is getting stiffer.

The outlook is grim. While new car buyers accounted for two-thirds of sales over the last five years, the next five will likely be driven by replacement demand, Goldman Sachs Group Inc. forecasts. To keep up with upgrading consumers, most automakers, including Geely, are rolling out new models of multi-purpose vehicles (the category that lies between SUVs and family vans). Sure, Geely is investing in a future of electric cars, but the costs for mass adoption remain high.

Geely has done better through the downturn by maintaining a fine balance between production, sales and inventory. But it has had to slash sales targets, moving further away from its goal of selling 2 million vehicles by 2020. While Lynk sales volumes rose, net profit fell. Research and development costs continue to climb. Geely remains exposed to lower-tier cities, where demand has cratered.

Vanity buying is best saved for more upbeat times. Investing in Aston Martin will be a cash sink, premium brand or not. Low as the price may be, a stake won’t add value to Li’s auto portfolio any time soon given its debt burden and a struggling core business. The Geely group should have other priorities, especially its finances.

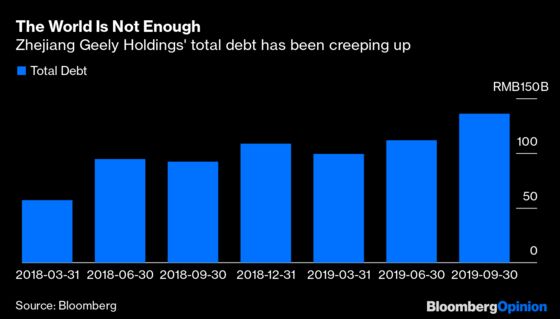

Debt at Zhejiang Geely totaled 136 billion yuan ($19 billion) at the end of September 2019, up from 92 billion yuan a year earlier. Previous stake purchases have come with leverage. To buy Daimler, for instance, Geely took to using complex derivatives. Its ratio of net debt to earnings before interest, tax, depreciation and amortization rose to 1.4 times in 2018 from 0.6 times in 2017, according to S&P Global Intelligence, because it took on a fair amount of debt to fund the acquisition of its 8% stake in Volvo AB. The credit rater estimated that the leverage ratio could rise further on lower sales and shrinking margins. Meanwhile, the parent actively supports various operations at subsidiaries.

Geely may find the slow lane is best for now.

44.1% owned by Zhejiang Geely Holding Co.

To contact the editor responsible for this story: Patrick McDowell at pmcdowell10@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2020 Bloomberg L.P.