(Bloomberg Opinion) -- The company behind Aston Martin should take the plunge and raise some equity while it can. Aston Martin Lagonda Global Holdings Plc doesn’t need the money immediately. But the historic sportscar maker may in the future, and it would be better to secure the cushion now before its window of opportunity shuts entirely. Thursday’s brief 21% share price fall should focus minds.

When Aston went public in October, it had a goal to produce about 7,200 cars this year, doubling to 14,000 in the “medium term” (understood as 2022). Last month it revised that first target down to 6,400 vehicles. Analysts are less optimistic about the future, with some now expecting Aston to deliver only 11,000-12,000 three years out.

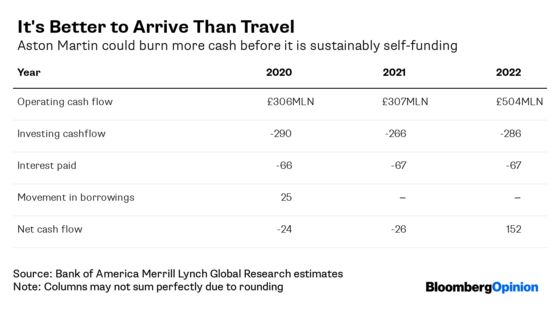

The shortfall matters. Aston’s business model is to use cash from car sales to fund development of its next models. Its yearly capital spending budget is roughly 300 million pounds ($362 million). Ongoing cash interest charges are estimated at about 65 million pounds. Operating cash flow is expected to be only 234 million pounds this year, according to Bank of America Merrill Lynch analysts. So Aston will have to dip into its 127 million pounds of cash reserves.

Can the company pay its own way from 2020? Opinions diverge. The group is due to launch its DBX sports utility vehicle in the second quarter, aiding cash generation. Some analysts expect operating cash flow to pick up and capex to fall, facilitating a reduction in net debt. Others sees the cash equation remaining slightly out of balance, and net debt rising next year and in 2021 but falling sharply thereafter. Aston can fund itself without recourse to new money in both scenarios.

But what if sales and cash generation fall sharply? There are three predictable risks: A badly managed Brexit could disrupt Aston’s supply chain more than it’s prepared for; the DBX might flop because of production snags or poor demand; a global economic slowdown would see Aston’s Asian and U.S. markets suffer from the same weakness that’s held Europe back this year.

In any of these scenarios, Aston’s cash could run dry unless the group slammed the brakes on the business and slashed capex. That might be a solution if Aston didn’t also face a looming refinancing in 2022. In reality, it will not want to go into that leaking cash and with the business on hold.

True, the carmaker could raise some new long-term debt now. This seems to be management’s preferred option. But it’s strange to be borrowing more when Aston is stretching to service its current debts. A 250-500 million pound rights offer would alleviate the strain, as BAML notes. With Aston’s market value now just 1 billion pounds, the chance to grab the top of that range may already have passed.

The weak share price, having already fallen so far, may make underwriters more willing to support a capital raise. James Bond is careful to drive a bulletproof Aston. This balance sheet needs the same armor.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.