Aston Martin Buys a Very Pricey Insurance Policy for Its New SUV

(Bloomberg Opinion) -- The maker of Aston Martin sports cars is buying what it calls an insurance policy against the risk it runs out of cash before the most critical product launch in its 106-year history. The terms of a new $250 million debt package unveiled Wednesday show just how limited the U.K. company’s options for securing funds are as it seeks to challenge Bentley and Lamborghini in the market for luxury sport utility vehicles.

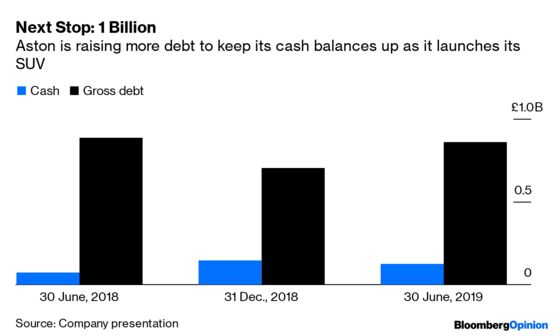

It’s an about-face from July, when Aston Martin Lagonda Global Holdings Plc said it didn’t think it needed more cash to make it to the first production run of its long-awaited DBX SUV next year. It’s still possible the actual need won’t arise. Cash generation in the first half of 2019 was poor due to weak sales. But it’s not clear yet whether Aston can sell enough cars in the second half to cover capital spending and cash interest costs without tapping into an existing 127 million pounds ($157 million) of cash reserves.

The snag is that Aston’s cash needs will only intensify in the months running up to the first DBX rolling off the production line in April at a brand-new, state-of-the-art factory in Wales. Especially as the threats to sales of its existing range are mounting: Brexit, the trade war, unrest in Hong Kong — the list goes on. The company had some 860 million pounds of gross debt at the half-year stage. With its latest debt issue, borrowing capacity is now completely exhausted.

Given Aston’s already high leverage, the financing charges of the new package are out of the orbit — 12% on a $150 million secured note ranking equal with its existing secured bonds. Another $100 million is available on the same terms if DBX orders hit a threshold. Otherwise, Aston can raise the cash on an unsecured basis — but paying 15%.

True, the cash interest is only 6% on each tranche, with the remainder rolled up and added to the principal borrowed. That mitigates the additional cash burn but adds to the refinancing burden when all the debts come due in 2022.

Shareholders remain worried. No wonder. The pile of borrowings is just so big, it’s hard to see how Aston can avoid issuing new shares at some point in order to bring it down.

These latest debt securities were likely sold in large part to Aston’s existing bondholders. After all, they have an interest in securing the launch of the DBX, which the company reckons fills a gap for a car that is both an SUV and beautiful. Likewise, Aston will be tapping familiar customers for DBX sales: Many Aston Martin fans also have an SUV and may like the idea of trading that up to a second Aston.

Everything hinges on the DBX’s success. Aston will need this car to be a worldwide hit if it is to comfortably refinance its debt. An equity offering surely looms at some point. Aston can but hope that its shares, 70% off their price in last October’s IPO, will be higher when that day comes.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.