Aston Martin and Funding Circle Left Painful Scars

(Bloomberg Opinion) -- It’s easy to announce an initial public offering in Europe, but far harder to complete it. Don’t be distracted by the handful of decent-sized share issues launched in January. The recent evidence suggests that the target audience for European IPOs is smaller, fussier and harder to reach than it used to be.

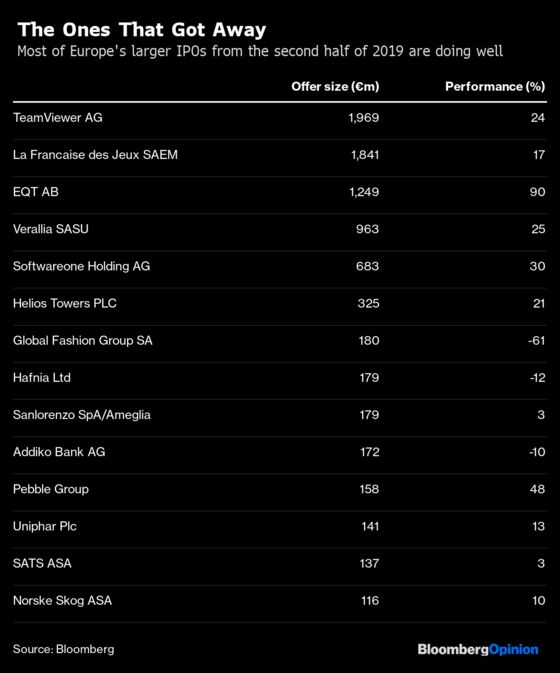

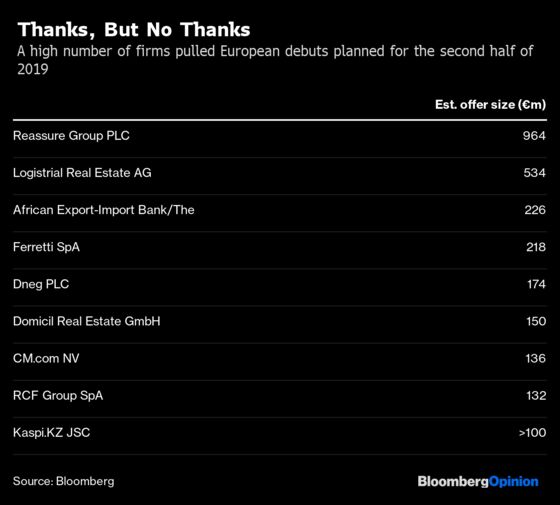

Some 17 offerings totaling 1.4 billion euros ($1.6 billion) were unveiled in January on European bourses. Look at how deals fared in the second half of last year and it’s hard to be confident that they will all reach the finishing line. Fourteen IPOs worth more than 100 million euros debuted in the last six months of 2019 (ignoring investment companies), Bloomberg data show. But nine got pulled. That’s an uncomfortably close ratio between offerings that got away and those that failed. Glance at the U.S. in the same period, or Europe in the preceding six months, and deal failures such as WeWork were vastly outnumbered by successes like Nexi SpA.

Clearly, the acute uncertainty around Brexit late last year was a dampener, making U.S. investors even more reluctant to leave their domestic market.

But Brexit probably just exacerbated existing problems. The drift to passive investment strategies is gradually reducing the number of active fund managers on whose support the IPO market relies. Those active managers that remain have to run more concentrated portfolios to beat their benchmark. Gone are the days when they would automatically buy most new stock offerings put before them.

The private-equity cycle hasn’t helped. Buyouts looking to go public nowadays are likely to have been purchased several years into the recovery in asset prices after the financial crisis; their owners will probably have injected more debt to juice up returns, making the assets less attractive to stock-market investors.

Meanwhile, MiFID rules have led investment banks to cut back their equity sales and research staff. That, in turn, weakens relationships with the asset management community. Even before that happened, book-runner syndicates tended to be smaller in Europe than in the U.S.

The spectacular losses inflicted by a handful of London deals from 2018, notably Aston Martin Lagonda Global Holdings Plc, Funding Circle Holdings Plc and Amigo Holdings Plc linger in the memory. Even that year’s star performer, cyber-security group Avast Plc, has dipped in 2020.

Some of these impediments could ease. The S&P 500 index trades on 19 times expected earnings versus the Bloomberg European 500 Index’s 16 times. Maybe that discount could tempt international investors to look at European stocks and, with them, IPOs. January has seen successful share sales by companies that are already listed. But there’s still no clarity on Brexit’s final shape, and MiFID is here to stay.

It adds up to a headache for companies looking to go public. One option is to hold back until the business has grown big enough to justify a decent market capitalization. Active fund managers may then be interested, knowing the shares will be liquid and will get a boost from forced buying by index funds. But for those who can’t wait, finding supportive investors has gone from shaking the tree to panning for gold.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2020 Bloomberg L.P.