(Bloomberg Opinion) -- The financial-market intelligentsia has been obsessed with “real yields” for a while now. With U.S. Treasuries trading in a range, stocks roaring back to record highs and gold suddenly regaining its luster, the fact that inflation-adjusted interest rates were deeply negative seemed like an obvious way to link the moves across markets.

I’m here to tell you that the sharp decline in real yields is something of a fake-out.

My first clue was from my discussion with Lacy Hunt, chief economist at Hoisington Investment Management. It didn’t make it into the published Q&A, but I asked him whether the V-shaped increase in U.S. breakeven inflation rates — and, by extension, the plunging yields on Treasury Inflation Protected Securities — made him question his view that deflation was the big economic risk. He brushed it off with a simple response: “The TIPS market is too small to get a good reading.”

Then I read this Twitter thread from Roberto Perli, head of global policy research at Cornerstone Macro LLC, and it all started to click into place:

Perli, a former associate director in the Federal Reserve’s Division of Monetary Affairs, is using a model from researchers at the central bank, which is updated through the end of July. The top-line result might be shocking to some: Market-based inflation expectations have barely budged during the coronavirus crisis. If anything, they’ve moved slightly lower.

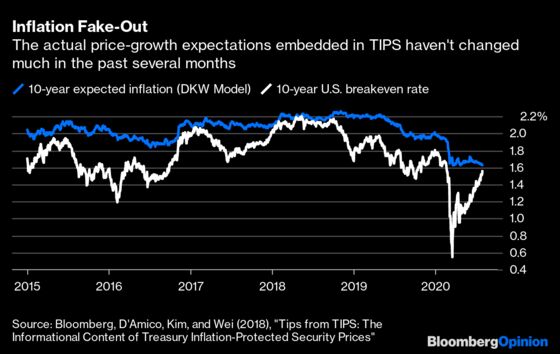

That is far from the pervasive narrative that has echoed across financial markets recently. Just to hammer it home, here’s a chart of 10-year inflation expectations based on the DKW model, along with the U.S. 10-year breakeven rate.

Put together, the two measures of expected inflation over the next decade tell startlingly different stories. But it becomes much easier to reconcile the two when recalling that Hunt deemed the TIPS market too small to be entirely accurate.

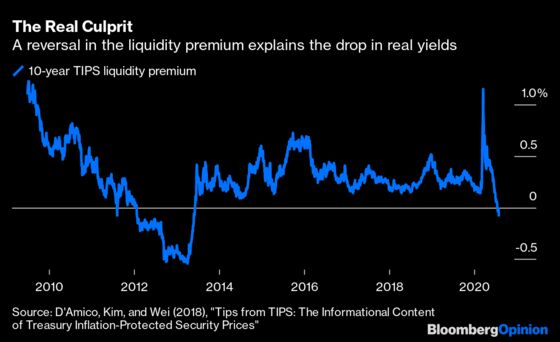

Put plainly, the swing in TIPS liquidity since March — from none to plentiful — has accounted for the vast majority of the move in breakeven rates and real yields. It comes down to basic math: If inflation expectations haven’t changed, and neither has the outlook for the average fed funds rate or the real term premium or the inflation risk premium, then the only other component left is the “liquidity premium.”

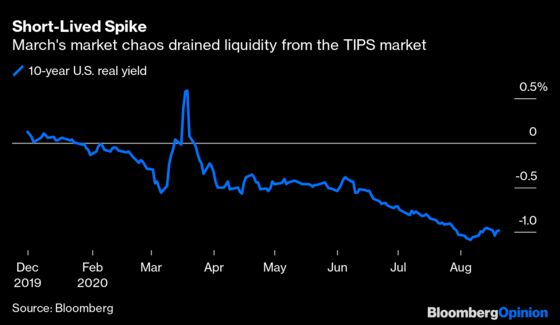

In hindsight, this dynamic should have been obvious to spot. During the worst of the Treasury market’s turbulence, I wrote about a seemingly inexplicable spike in U.S. real yields. The 10-year TIPS rate surged more than 40 basis points, from just less than 0% to 0.39%, in the largest one-day move in Bloomberg data going back to 1997. “Given the lack of liquidity plaguing the Treasury market, it’s hard to know for sure whether this huge move in real yields is, well, real,” I quipped.

The Fed’s model reveals it was precisely a liquidity squeeze that jolted real yields. On March 18, when I flagged the record surge in real yields, the “liquidity premium” was 1.12%, a sixfold increase from two weeks earlier. Only in late June did liquidity revert back to its early-March levels. It shouldn’t come as much surprise that around that same time, real yields touched the lowest level since 2013.

The drop in the liquidity premium didn’t stop at around 0.2%, however. Rather, it has continued to slide, so much so that it turned negative at the end of July, meaning it’s now pushing down real yields and pushing up inflation breakeven rates. In other words, it’s working to exacerbate the recent trends.

“We need to understand that being long breakeven rates today doesn’t mean necessarily being long inflation,” Perli said on Twitter. “More than anything it means being long TIPS liquidity. The trade probably continues to work, but be careful because TIPS liquidity can be fickle.”

My Bloomberg Opinion colleague Tim Duy raised a good question about the ability to distinguish between liquidity and inflation expectations. After all, if traders saw a greater risk of accelerating price growth, they’d naturally turn to TIPS, therefore improving liquidity. There’s not an obvious answer, but the fact that the liquidity premium turned negative for the first time since 2013 suggests it’s not the equilibrium state of the market; a further increase in U.S. breakeven rates — and decline in real yields — will probably have to come from a move higher in expected inflation.

Now, that’s hardly a far-fetched scenario. The U.S. core consumer price index increased 0.6% in July from a month earlier, its biggest jump since 1991. Meanwhile, University of Michigan survey data show Americans expect a 2.7% inflation rate over the next five to 10 years, matching the highest level since 2016 and up from 2.2% at the end of last year. Combine that data with the Fed’s framework review, which is expected to signal greater tolerance for price growth to exceed the central bank’s 2% target, and there’s hardly a shortage of reasons to justify inflation protection.

Citigroup Inc., for one, has suggested going long 30-year breakevens. “The argument for buying long end BEs is primarily based on expectations of rising inflation risk premium,” strategists led by Jabaz Mathai wrote on Aug. 20. On that same day, a Treasury auction of 30-year TIPS had a yield that was more than five basis points higher than indicated before the sale, signaling weak demand for inflation-linked securities at the prevailing price.

Across the curve, history suggests the climb in inflation breakeven rates will get much harder from here. Most maturities are now roughly in line with their five-year averages, bolstered by the now-negative liquidity premium. There’s nothing stopping the liquidity component from remaining negative for months or even years, of course. But if Fed officials are correct and disinflationary pressure grips the U.S. economy, it could spark a selloff in TIPS. Even just a loss of momentum in inflation-linked securities after their best performance relative to nominal peers in at least 22 years could push real yields higher as investors take profits from the crowded trade. That, in turn, might prompt some soul-searching among recent gold converts, or those who have left bank stocks for dead.

Framing financial market moves in the context of real yields sounds sophisticated, but it’s crucial to know the variables influencing TIPS rates rather than take them entirely at face value. “We are talking about models so we need to be open to the possibility that they might be off,” Perli told me. “But there is backup information that supports the conclusions.”

The signal from the TIPS market, then, isn’t so much that inflation is making a comeback, but that expectations hardly budged during the Covid-19 pandemic. That will be a humbling realization for investors who have been trading based on the premise of ever-lower real yields.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2020 Bloomberg L.P.