(Bloomberg Opinion) -- Marks and Spencer Group Plc isn’t just reviving its notorious food porn ads. Chairman Archie Norman seems set on turning the food-to-furnishings retailer into a grocer.

It’s not surprising that the executive who in the 1990s turned around Asda, now Walmart Inc.’s British operation, wants to focus on food. But it’s a brave move, nonetheless. Britain’s grocery market is brutally competitive and its margins are skinnier than what M&S is used to.

On Wednesday, M&S announced a rights offering to fund its joint venture with Ocado Plc, a move that will double the size of its grocery business over the next five years or so. The division generated sales of almost 6 billion pounds in the year to March 30 2019.

Excluding the impact of this year’s late Easter holiday, the division appears to be growing. The same can’t be said about M&S’s clothing operation.

So M&S’s decision to pare the amount of floorspace it dedicates to clothing by 25% to make way for more food aisles makes sense.

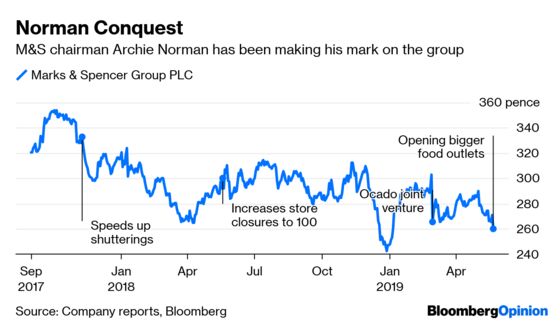

But the retailer appears to be going further than stacking its shelves differently. On Wednesday, the company said it will close 25 smaller food stores but will open more bigger outlets, with car parking and a broader range of products. That sounds more like a traditional supermarket than somewhere to pick up a ready meal for dinner.

That pivot from fashion to food should trouble investors. Although grocery accounted for 63% of M&S’s U.K. revenue in the last fiscal year, it is less lucrative than clothing.

M&S doesn’t break out the earnings of each division. But assume that food has an operating margin of about 3% – reasonable given the figure for Britain’s publicly traded supermarkets is about 2.5% to 3% – and that the measure for clothing is about 10%. In that case, M&S would have to generate roughly three times more in food sales to make the same profit it achieves from clothing. So even if the retailer manages to turbocharge its grocery revenue, the move wouldn’t necessarily be accompanied by a jump in profit.

Its margins could still be vulnerable. While there will be synergies from the Ocado deal, delivering groceries to customers’ homes is typically more expensive. And Waitrose, Ocado’s current delivery partner, is likely to mount a fight-back.

M&S shares are down 15 percent since the company announced the deal with Ocado in February. Some of that reflects the rights offering and a dividend cut – but it also shows some skepticism about Norman’s food strategy. Given his track record, it would be foolish to bet against him. He has time to make a go of things, having carefully managed expectations. But shareholders will want to see that all this action – not to mention 1 billion pounds of one-time charges over the past two years – adds up to more than just a catchy marketing slogan.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.