(Bloomberg Opinion) -- In 2008, Schaeffler AG, a family-owned German auto parts supplier, made an offer to buy the shares of its listed rival Continental AG. It almost collapsed under the debt it amassed to fund the deal, which was unveiled shortly before the Lehman Brothers bankruptcy.

A decade later, another privately held German car parts company, ZF Friedrichshafen AG, has made a similarly ill-timed, debt-funded takeover: the $7 billion acquisition of truck-braking specialist Wabco Holdings Inc. ZF is now cutting thousands of jobs to keep its creditors at bay.

It’s possible you haven’t heard of ZF, because it doesn’t sell directly to consumers and isn’t listed on the stock market. But you will have heard of Ferdinand von Zeppelin, the man who set up ZF a century ago to start building gears for his airships. This mode of travel captured the world’s imagination until the 1937 Hindenburg fire ended the era of luxurious passenger-carrying dirigibles.

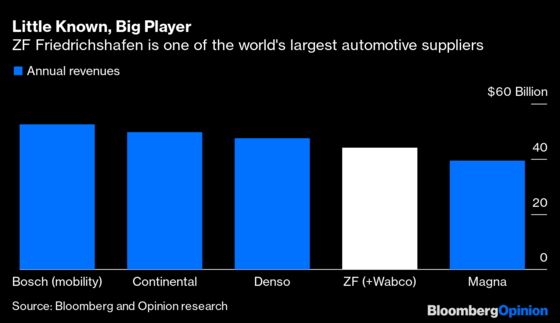

Today ZF is one of the largest auto parts suppliers, with almost 40 billion euros ($45 billion) of yearly sales. Its 160,000 employees make everything from vehicle transmissions to braking and automated-driving technology.

Instead of airships, ZF has used aggressive dealmaking to cross the Atlantic. It swallowed U.S. rival TRW Automotive for $12.9 billion in 2014, and after years eyeing Wabco it finally made a move last year. (Wabco is based in Bern, Switzerland, but was listed in the U.S.) These deals have helped reduce the company’s dependence on combustion-engine technologies, which now comprise less than 30% of ZF’s revenues.

But future-proofing has forced the once cautious German group to embrace some pretty racy, Anglo-Saxon ways. The Wabco deal was priced at an eye-watering 20 times the target’s average earnings over the past three years. ZF has amassed 9.6 billion euros of debt and it has another 5 billion euros of pension liabilities, according to Bloomberg data. Wabco’s boss, Jacques Esculier, is in line to receive a $24 million golden parachute payment for selling to ZF, but that’s nothing compared with the $88 million that TRW boss John Plant received after ZF’s takeover.

Some companies have tried to amend or back out of deals agreed before the coronavirus pandemic but the Wabco deal closed as planned last month. ZF’s management wrote immediately to employees, revealing up to 15,000 job cuts (about 10% of its workforce). If debt covenants aren’t met, “external creditors could demand influence over our business decisions,” the email warned. Lacking a stock market listing, ZF can’t easily raise capital from equity investors.

When car sales were still growing steadily, automotive companies and their suppliers could afford to carry some excess weight. ZF’s operating profit margins were about 4% on average over the past five years, providing only a thin cushion. Now it’s having to confront three shocks all at once: coronavirus production shutdowns, a global recession and the structural shift to electric vehicles.

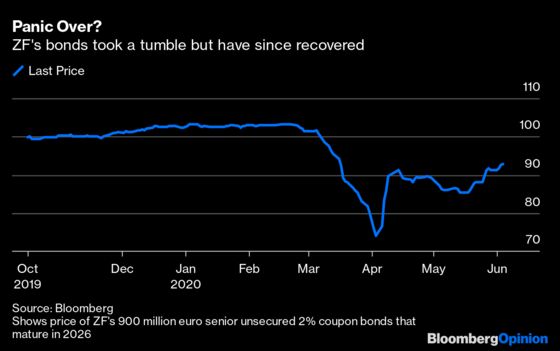

About 80% of ZF’s 50,000 German employees have had their working hours cut because of the pandemic. The company warned it will make large losses and credit-rating agencies have downgraded its debt to junk. ZF has joined the ranks of so-called “fallen angels,” which have lost their investment-grade status. Its bonds lost more than a quarter of their value at one point, but have rebounded following aggressive market interventions by central banks.

So is this just another tale of a debt-enamored company getting a coronavirus comeuppance? Maybe not. In at least a couple of respects ZF is pretty unique.

About 94% of the company’s shares are controlled by the Zeppelin Foundation, a legacy of the airship inventor that’s overseen today by the German city of Friedrichshafen — population 60,000. The cost cuts are a blow to the town, situated on the shores of the idyllic Lake Constance. Dividends from ZF helped pay for its hospital, university and preschools. The town’s mayor, Andreas Brand, sits on the company’s supervisory board and is pretty influential. Stefan Sommer, the architect of ZF’s debt-funded expansion, stood down as chief executive officer in 2017 after clashing with the more cautious Brand.

ZF’s borrowings are pretty esoteric too. It has regular bonds but it’s also a prolific user of Schuldschein finance, a form of debt — not quite a loan and not quite a bond — that’s popular with Germany’s “Mittelstand” of small and medium-sized companies. Lately this financing model has spread beyond German-speaking countries, with borrowers attracted by the limited disclosure requirements. Schuldschein debt can cause complications, though, if a company gets into difficulty. The permission of each borrower (rather than a simple majority) is required to restructure the debt.

No wonder ZF is so keen to keep its creditors at arm’s length. Last month it amended a key lending agreement, which will allow its net borrowings to widen to as much as 5.5 times Ebitda (a measure of cash earnings) in the next 12 months. The company is not in any immediate danger because it has about 10 billion euros of cash, cash equivalents and credit facilities, and there are no major borrowings that need refinancing soon. Still, its leverage is heading higher than its owners and lenders would like.

JPMorgan Chase & Co. advised ZF on its Wabco takeover and helped furnish it with a larger overdraft facility. A decade ago JPMorgan advised Continental on how to defend itself against Schaeffler’s approach. It knows all about the pitfalls of doing a big deal at the top of the market.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2020 Bloomberg L.P.