(Bloomberg Opinion) -- It takes something special to really stand out in debt capital markets in 2020 when issuance has hit a new record, but Austria’s Erste Group Bank AG certainly caught the eye this week with a perpetual deal at an incredibly low yield of 3.375%.

It was the second lowest coupon on record for a so-called additional tier 1 regulatory capital bond, also known as a CoCo, which is an especially risky type of debt because the investor bears the losses if the bank fails. Even so, and despite the small yield, the 500 million-euro ($554 million) issue was more than 10 times subscribed.

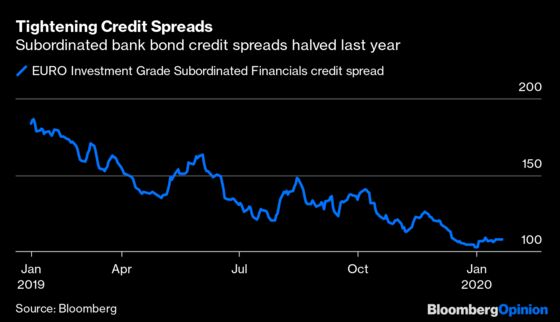

Investor demand for the riskiest type of European bank debt has never been stronger. This AT1 class of regulatory capital was created after the banking crisis to bolster lenders’ financial reserves — and to offer a generous rate of interest to reflect their riskiness.

Although it’s a perpetual bond, making it similar to equity, the market practice is almost always for this kind of note to be redeemed at the first issuer call date — a convention that Spain’s Banco Santander SA flouted shamelessly last year. While the coupon can look optically attractive, it’s not for the faint-hearted.

Erste is the first AT1 deal this year with an investment grade rating, opening it up to a wider pool of demand. The bank could easily have issued more but it chose to stick to its announced size. Instead it drove the yield on offer down by 62.5 basis points from the initial price talk of a 4% coupon, a bigger than 15% reduction.

That’s an extraordinary cut for a fixed-income deal, though it’s not unique in this market — where investors will take almost any yield they can get. A similar AT1 deal from the lower-rated Italian lender Banco BPM SpA was tightened by 75 basis points just last week. This looks suspiciously like bait and switch, where investors are lured with a high coupon only to let the issuer build a huge book of demand and then slash the return on offer.

Erste has been on quite a journey since having to write off billions of euros in 2014 from ill-fated ventures in Hungary and Romania. It returned to the AT1 market in 2016, but had to pay an 8.875% coupon, more than 2.5 times what it’s paying on the new issue.

The Austrian lender placed a similar bond at 5.125% as recently as March, illustrating the strength of investor demand for top-rated bank debt at a time when European government bond yields are incredibly low or negative. The European Central Bank has restarted bond-buying, so it’s it is hard to see this investor hunt for yield stopping soon. Still, debt-pricing techniques might be a little less shameless.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2020 Bloomberg L.P.