The City of London Fails to Take Back Control After Brexit

(Bloomberg Opinion) -- The City of London’s chief coping mechanism for dealing with Brexit’s threat to the financial services business is to dismiss the loss of jobs and investment as a trickle rather than a flood.

Yes, cheerleaders argue, some 7,500 jobs have been moved to the European Union, but that’s a fraction of the hundreds of thousands predicted by the doomsayers. Sure, job openings in London’s finance industry almost halved in 2020, but that had a lot to do with Covid-19. Of course EU share trading has flowed to the continent, but it’s a low-margin business that’s symbolic at best.

This analysis has two problems.

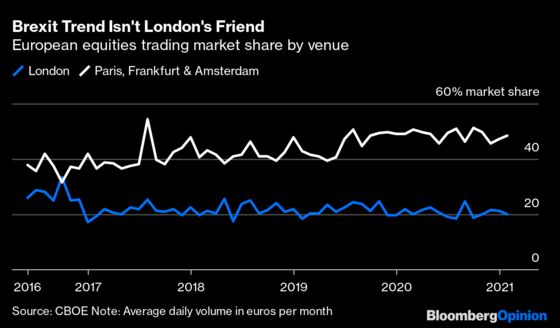

The first is that even a trickle can do damage if left unchecked. European equities trading may be small beer in the grand scheme of things, but it’s notable that London’s market-share loss hasn’t recovered. Amsterdam even surpassed the City as Europe’s largest share trading center last month by average daily volume, according to the FT.

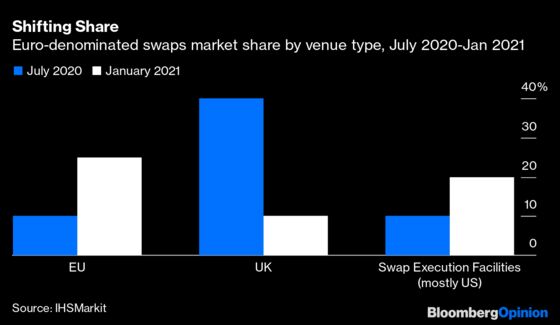

And even if stock trading is a “sideshow” next to derivatives, as former London Stock Exchange Group Plc boss Xavier Rolet put it, the picture there doesn’t look great either. U.K. venues’ share of euro-swap trading fell to 10% last month from nearly 40% in July, according to IHSMarkit. While the U.S. won some of this business, the EU’s portion also rose.

The second problem for London’s cheerleaders is that these shifts are emboldening officials in Paris, Frankfurt and Brussels to stick to a tough regulatory stance. Brits were hoping the Europeans would regret treating London as a new rival on their doorstep. The opposite has happened. Brussels still hasn’t granted the U.K. full “equivalent” status that would allow for preferential, if not frictionless, cross-border trade in financial services. With fears of a costly fragmentation of markets so far unfounded, there’s been no clamor from European market participants to go easy on London either.

Unlike the post-Brexit customs checks that have disrupted trade in goods, often described as “teething problems” that will be smoothed out, friction in financial services is increasingly seen as the beginning of a new normal. The obligation to trade EU stocks on EU soil is seen as a beachhead — a mere “skirmish,” as Aquis Exchange Chief Executive Officer Alasdair Haynes puts it. The real war will be over the clearing infrastructure that underpins London’s dominance of derivatives trading.

The more things go the EU’s way in the early stages of this highly politicized financial tug of war, the more control they’ll seek. And the U.K.’s lack of clarity on its post-Brexit plans for financial regulation doesn’t help its position. The fear in Brussels that Brits’ urge to deregulate could drive a tank through single-market rules is very real. EU markets watchdog Esma recently warned of “ questionable practices” by financial firms trying to circumvent rules on selling services into the bloc.

So when Bank of England Governor Andrew Bailey says the U.K. wants to avoid “rule taking” from Brussels, while in the same breath promising there’s no plan for a “high-risk, anything-goes” financial system, it’s simply too easy for the EU to dangle equivalence as a quid pro quo in return for more concrete assurances. EU Brexit negotiator Michel Barnier said the bloc wouldn’t be hurried into making such decisions.

Instead of “taking back control” as a result of Brexit, the City sounds more like it’s spinning its wheels. Covid-19 may have slowed the pace of physical job relocations to the EU, but it’s also shown how mobile capital can be. There’s no sign yet the Europeans have bitten off more than they can chew. Hopes for an imminent thawing of relations look very optimistic.

None of this means London will suddenly stop being Europe’s top financial center. The City is a global hub in a useful time zone, its legal system is trusted the world over, and its language is as influential as Greek was in ancient times. New ideas such as the listings review chaired by Jonathan Hill, a former EU commissioner, may bear fruit.

But there’s a big difference between a London that holds a near-total monopoly on European financial jobs and trading — as it did before Brexit — and one that has two-thirds of the pie, or maybe even just half of it. If the U.K. doesn’t play its cards right, we may be heading for the latter — drip by drip.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering the European Union and France. He worked previously at Reuters and Forbes.

©2021 Bloomberg L.P.