This Alpine Lighting Deal Brings an Avalanche of Risk

(Bloomberg Opinion) -- A 12,000-foot-high Alpine mountain range and 250 miles separate AMS AG’s base in the Austrian town of Premstaetten and Osram Licht AG’s Munich headquarters. The Austrian firm must overcome much bigger obstacles in its attempted takeover of the German lighting-maker.

After months of toing and froing, AMS finally tabled a 3.7 billion-euro ($4.1 billion) approach for Osram late on Sunday. The deal would trump a 3.4 billion-euro bid from Bain Capital and Carlyle Group LP that Osram has already accepted. From that perspective, it looks very attractive to the German company’s investors. The approach offers a glimmer of hope: the Bain-Carlyle bid appears dead in the water after being rejected by Allianz Global Investors, Osram’s biggest shareholder, last week.

The difficulty is on the AMS side. Chief Executive Officer Alexander Everke hasn’t yet done enough to warrant lifting the company’s debt ratios to levels well above most peers in exchange for returns in the near term that are likely to be below capital costs, based on planned synergies and analyst earnings forecasts. The company is confident returns will exceed costs in the second year after the deal completes. That will be contingent on hitting some ambitious savings targets.

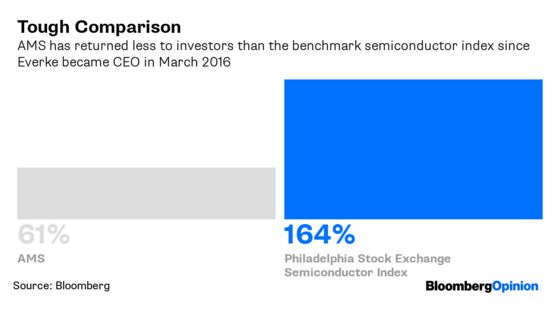

In Everke’s three years at the helm, AMS has generated significantly lower returns for shareholders than the Philadelphia Stock Exchange Semiconductor Index, despite major outlays on acquisitions and manufacturing capacity. Sure, AMS has improved its sensor offering and, after a bumpy few years, might finally be starting to demonstrate returns on that spending.

But integrating Osram, with its 24,300 employees globally, is a significantly greater challenge than AMS’s biggest acquisition to date: The 2016 deal to buy Heptagon, with just 830 employees, for $570 million.

To fund the takeover, AMS plans a 1.5 billion-euro equity increase, underwritten by UBS Group AG and HSBC Holdings Plc, which 50% of shareholders will need to approve at an extraordinary general meeting in the fourth quarter. In return, it will get a company whose core automotive market is shrinking.

The offer is a gamble on carmakers adopting more and smarter sensor technology for the vehicles they are still able to sell. Osram’s strongest business has traditionally been car headlamps, but in recent years it has expanded into different parts of the optical spectrum, such as infra-red. AMS is optimistic that it can package those products with its sensors to work in autonomous cars (which might need laser-based environmental sensors) and for in-cabin sensing (to tell, for example, if the driver has fallen asleep).

It seems a hell of a lot of upfront risk given that it’s unclear what kind of sensors autonomous cars will need when they hit the roads on a significant scale in perhaps a decade’s time. AMS was unwise to invest so heavily in smartphone sensors when it did. But the automotive sensor market is not the best way to diversify.

--With assistance from Chris Hughes.

To contact the editor responsible for this story: Stephanie Baker at stebaker@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.