(Bloomberg Opinion) -- The Bank of England met on Thursday against the backdrop of a newly imposed lockdown that’s designed to curb the spread of the coronavirus, but will also crimp the U.K. economy. For lenders who were already nervous about borrowers being unable to pay their debts, the prospect of a second collapse in growth will prompt them to rein in their support even further.

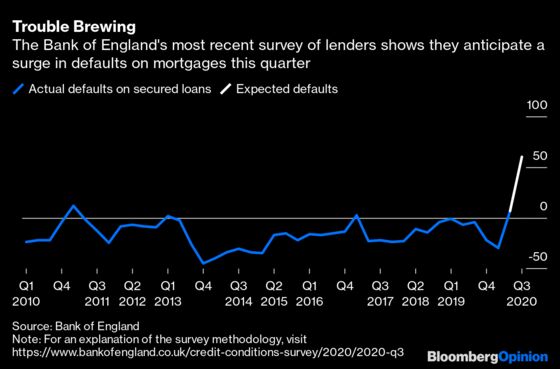

The central bank’s most recent survey of credit conditions, conducted Sept. 1-18 and published in mid-October, showed lenders anticipating a surge in mortgage defaults this quarter after years of stability.

With non-essential businesses closing from this week, economists are busy trimming their estimates for U.K. growth in the coming three months. That will lead to higher unemployment, making consumers more apprehensive about their financial futures and mortgage lenders even more wary about the health of their lending books.

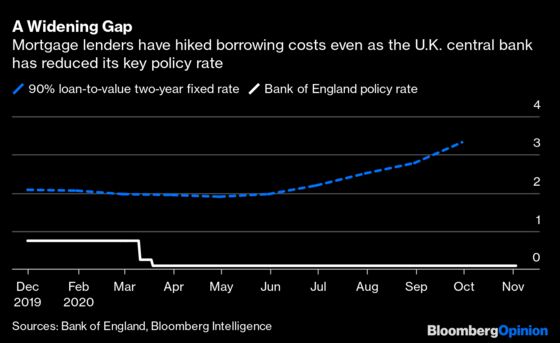

For the Bank of England, that’s a problem. It’s slashed official interest rates to a record low of 0.1% in an effort to stimulate lending and borrowing. But in the U.K. mortgage market, banks and building societies have steadily increased how much they charge on the most prevalent fixed-rate home loans.

For a household borrowing 90% of the value of its home, the cost of a two-year fixed mortgage has surged to 3.32%, its highest level in more than five years. So the central bank’s efforts have done nothing to ease the burden of the biggest debt carried by most consumers.

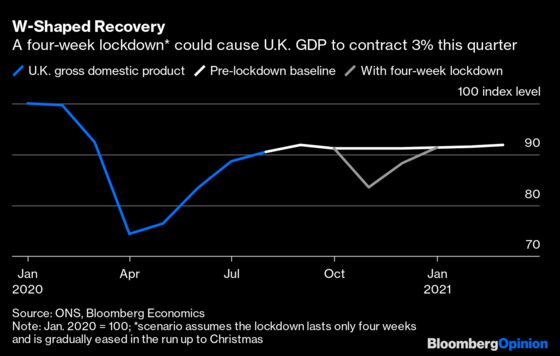

As for forecasting what will happen next to the economy, the advice for soothsayers is to rip it up and start again. The new lockdown makes growth forecasts for the fourth quarter even more of a guessing game than previously, not least because it’s far from certain that restrictions will be eased on Dec. 2 as the U.K. government currently anticipates. A partial lifting in the run up to Christmas would at least allow retailers and hospitality venues to make something out of the holiday season, as opposed to facing a total washout if it is extended.

Barring moving Christmas to the spring, there is going to be another dip in the final quarter of the year, with the summer rebound becoming a distant memory. This second national shuttering is unlikely to be quite as savage as the first, which saw gross domestic product plunge 20% between April and June. But Dan Hanson at Bloomberg Economics has already revised down his fourth-quarter estimate to -3% from +1% — a scenario he says will only get worse if the restrictions are extended deeper into December.

The monetary policy committee won’t put much reliance on the quarterly economic assessment because not even real-time data can shed much light on how the next few months will pan out, let alone any Brexit conclusion. The central bank added a larger-than-expected 150 billion pounds ($195 billion) to its bond-buying program on Thursday, ensuring U.K. gilt yields stay firmly anchored, which will help the government fund its ballooning fiscal support.

Gilt issuance in this financial year will now exceed the current expectations of 500 billion pounds, as the government’s borrowing requirements have shot up again with the extension of the employment furlough scheme and a doubling of aid for self-employed workers.

So until the economic fog clears, the best thing the monetary policy committee can do is to follow the playbook it’s used from the onset of the pandemic, which Governor Andrew Bailey has described as going “big and fast.” Thursday’s action certainly qualifies as both those things, and there’s a clear willingness to do more. But for homeowners who need to either roll over existing mortgages or take out new loans, the economic pain will only get worse.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.